How to Raise Your Credit Score by 100 Points

LJ

Last updated 03/19/2024 by

Lara JacobsSummary:

Are you going to be seeking a loan or new credit in the foreseeable future, or do you need to raise a mediocre credit score? This article explains how credit scores are calculated and gives 10 straightforward tips for boosting your credit score by 100 points. It also includes a convenient FAQ section about improving credit scores and how quickly this goal can be achieved.

If you’re trying to buy a house or car or seeking a new job, a higher credit score could mean the difference between success and disappointment, especially if you have a limited credit history. Even if you’re not in the market for a loan, working to improve your score is a good strategy in general. Whether your credit is poor, so-so, or even pretty good, chances are it could be even better.

On the other hand, if you’re seeking a silver bullet or magic wand, you are bound to be disappointed. While some of the strategies below can result in a dramatic rise in your credit score within a short period of time, there is no quick fix where improving your score is concerned. Nonetheless, following these tips will greatly improve your odds of achieving a higher credit score.

Compare Credit Repair Services

Compare multiple vetted providers. Discover your best option.

What factors are used to calculate a credit score?

Before jumping into the strategies to boost your credit score, you should know exactly how it’s calculated.

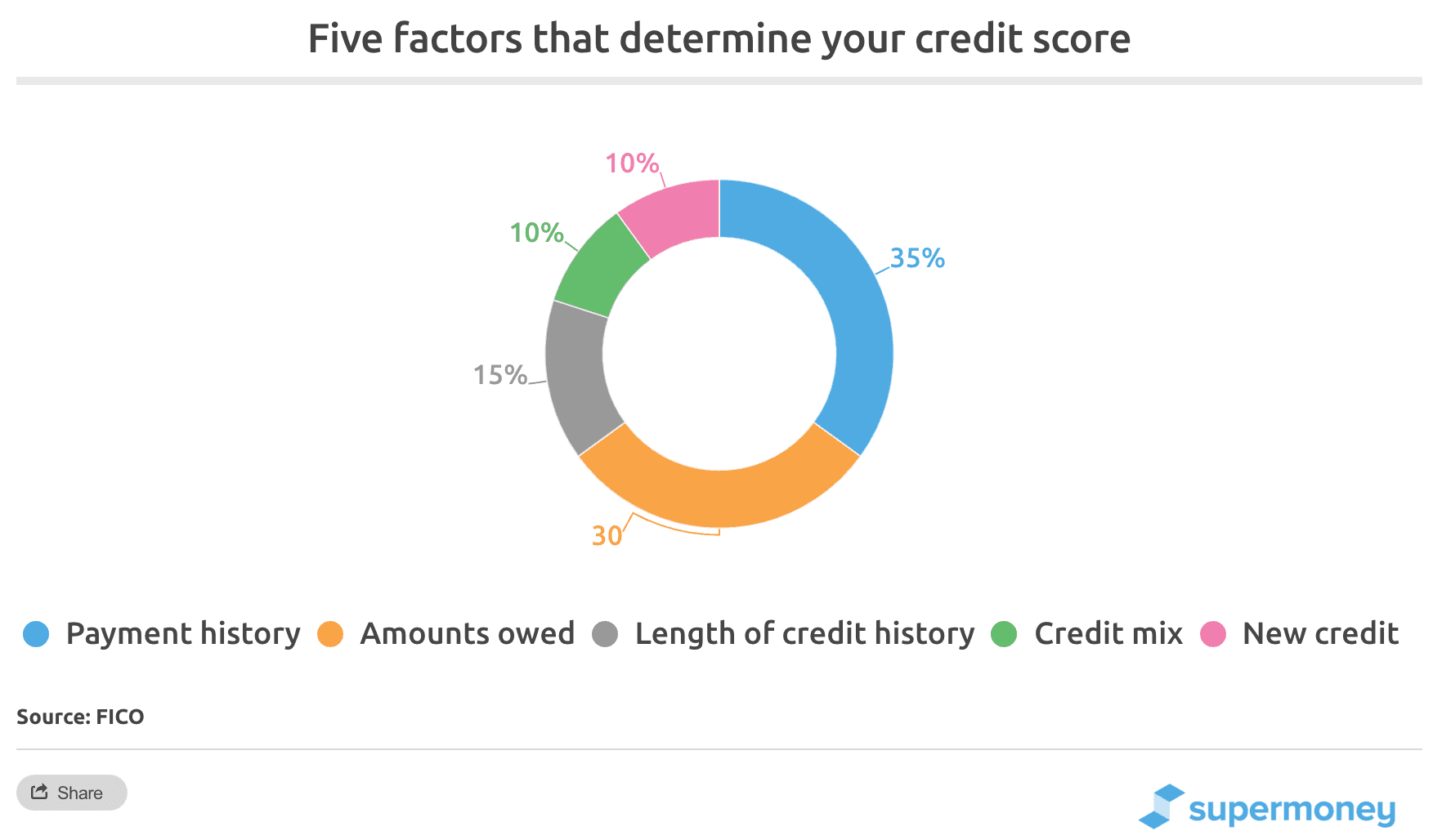

Your FICO score is based on the information in your credit reports from the three major credit reporting agencies: Equifax, Experian, and TransUnion. FICO scores are used by approximately 90% of lenders and creditors when determining whether or not to issue you credit and how much. The formula used to come up with the magic three-digit number breaks down as follows:

- Payment history (35%): If you miss a payment, a negative mark is added to your credit report once the account is 30 days or more past due, and the mark remains there for 7 years.

- Credit utilization (30%): This is the percentage of available credit that you use each month across all your revolving accounts (credit cards). It is best to keep this figure at 30% or lower.

- Length of credit history (15%): The longer your credit history, the more favorably creditors view you.

- Credit mix (10%): Ideally, you want to have a credit mix balance of both installment and revolving accounts.

- Credit inquiries (10%): Most lenders and service providers will report a hard inquiry on your credit history when you apply for credit. Fewer hard inquiries are best, as many inquiries generated in a short period of time could signal financial distress. Your score gets a small ping each time you apply for credit.

So, with this information in mind, how can you improve your credit score by 100 points

10 strategies to boost your credit score by 100

Improving your credit score is not an exact science. There are many steps you can take to improve it, but the exact result will depend on your credit profile.

For example, people with excellent credit will experience a higher score drop if they miss a payment than someone who already has poor credit. It will also take them longer to recover if get negative items on their report.

There are no quick fixes either (with the exception of strategy #6). Improving your credit score typically requires both effort and patience. On the other hand, the examples we include below illustrate how many of the strategies available to improve your score involve commonsense steps that you should be taking anyway.

That’s the good news. Nearly everyone can improve his or her score significantly. The table below summarizes the key actions that can influence your credit with estimates on the effect they can have on your scores based on data provided by FICO. I then break down these actions into simple strategies you can start implementing today.

| Credit Action | Estimated impact on credit score | Average time to recover |

|---|---|---|

| Miss a payment by 30 days | -35 to -90 | 9 to 18 months |

| Miss a payment by 90 days | -45 to -180 | 1 to 3 years |

| Lower credit card balance by 25% | +2 to +25 | n/a |

| Get a new $5K personal loan | -15 to -25 | n/a |

| Max out your credit cards | -35 to -140 | 3 months |

| Foreclosure | -35 to -125 | 3 to 7 years |

| External collections | -100 to -150 | 18 months |

| Charge-off | -45 to -130 | 18 months |

| Bankruptcy | -100 to -200+ | 6 years |

Note that most of the credit actions have a negative effect on your credit score. Not having these items on your credit report will gradually improve your credit score over time. The third column shows how long it takes (on average) to recover from a negative action. This gives you an idea of the relative importance of keeping those items off your credit report if your goal is to increase your score.

1. Pay bills on time

Your payment history is one of the two most important factors when it comes to your credit score. As stated above, it accounts for a whopping 35% of your overall score. Maintaining a current and pristine payment history is an excellent way to boost your score substantially. On the other hand, falling behind on your payments for even one account is almost guaranteed to sink your FICO score considerably. The other most important factor in your score is your credit utilization. Keeping a low credit utilization ratio, which is your account balances in relation to your available credit limits, is essential.

Key takeaway: Missing just one payment by 90 days could lower your credit score by as much as 180 points

2. Pay down your balance and keep it low

Another significant factor in your FICO score is your credit utilization ratio. For credit scoring purposes, 30% or lower is the sweet spot for credit utilization. Therefore, reducing your debt levels can improve your credit score quite a lot. Try to pay down your debt to that 30% level, or as close as possible.Alternatively, you could call your credit card company and request a credit limit increase to reduce this percentage without emptying your bank account. This only makes sense if you have the discipline to not use the credit card with its new higher credit line, of course. Also, if a credit card issuer performs a credit check to determine your eligibility, it could ping your score and lower it by a couple of points. Only take the chance if you’re reasonably confident you’ll be approved for the credit limit increase.

Key takeaway: Reducing your credit card balance by 25% could improve your credit score by up to 55 points.

3. Only apply for credit when you need it

When you are house-hunting, you will probably seek out the best possible interest rate for your mortgage. Likewise, you will probably shop around for the lowest interest rates for a car loan if you’re in the market for a new ride. Credit reporting agencies account for that by counting similar credit inquiries made within a limited period of time as one “hard” inquiry, which translates to a lesser hit to your credit rating. Try to concentrate your credit inquiries within short periods of time, and don’t apply for credit unless you need it.

Key takeaway: Getting a $5K loan could lower your credit score by up to 35 points, but it could also improve your score in the long run if you make regular and on-time payments.

4. Leave old accounts open

The age of your oldest active accounts also has a bearing on your credit score. Therefore it’s a good idea to leave old accounts open if they are in good standing. This is especially true for credit cards with high credit limits that you don’t use often — leaving those accounts open improves your credit utilization ratio, which also boosts your score.

Key takeaway: Closing credit accounts will usually lower the average length of your credit history and will reduce your debt to credit ratio (if you carry a balance), which are both bad for your credit score.

5. Reschedule payment due dates

Your credit card issuer may give you the option of scheduling your due date. Take advantage of this convenience and schedule your due dates for one or two days after your pay dates if you are a wage earner so that you are more likely to have cash on hand to pay. That’s another way to help maintain consistent on-time bill payments.

Key takeaway: This is a defensive move that will help you avoid missed payments.

6. Correct credit report errors

You are entitled to obtain one free copy of your credit report annually from each of the three major credit reporting agencies: Experian, Equifax, and TransUnion. If you space your credit reports every four months, you could monitor your credit year-round for free. To keep your credit file clean, ensure that all errors get corrected.When you file a dispute over erroneous information in your credit report, the credit bureaus have 30 days to investigate and determine whether or not the information is accurate. If the credit bureaus rule in your favor and adjust your score, you could see a jump of several points just by getting the wrong information removed; no additional steps are required. Monitoring your credit reports and correcting errors is a surefire way to improve your FICO score.

Key takeaway: This is possibly the fastest way to improve your credit score. If you have multiple incorrect negative items on your report, you could increase your score by hundreds of points.

7. Establish and maintain a mix of credit

Balance is the key to life. Maintaining a perfect on-time payment record for one credit card account is great. But maintaining a record of on-time payments on a credit card account, a mortgage, and an auto loan is even better. That’s because credit cards count as revolving credit, while mortgages and auto loans are categorized as installment loans. Having a balanced credit mix is important for credit health. When a credit bureau sees that you can handle both types of debt responsibly, it definitely benefits your credit report and FICO score.

Key takeaway: Your credit mix accounts for up to 10% of your credit score so having a healthy mix will help although it’s hard to say by how much.

8. Clean up overdue debts

This step can be a tricky one. If you are struggling financially and have an old debt that will drop off your credit report in a few months, you may decide it’s best to let it go unpaid. Note that delinquent accounts stay on your report for up to seven years. However, typically it is best to pay delinquent accounts since it can improve your credit score and your chances of qualifying for additional credit. Note that paying delinquent accounts will not remove them completely from your credit report. They will still appear as paid late, but it looks a whole lot better than just having a delinquent account. One option worth considering is to negotiate a pay for delete arrangement with your creditor. This arrangement requires the creditor to remove the negative item if you pay the debt. Creditors are in no obligation to accept “pay for delete” requests, but sometimes it works.

Key takeaway: Missed payments are lethal to your credit score. Just one missed payment by 30 days can lower your credit score by 80 points.

9. Don’t signal possible credit problems

Are you going through a nasty dispute with a partner or (soon to be ex) spouse? Avoid paying attorney’s fees with a credit card, taking a rash of cash advances, or using your credit card at a pawn shop. While these actions themselves don’t have a direct adverse impact on your credit report or your FICO score, such behaviors could indicate that you’re having money problems. Merchants and credit card companies might get spooked and reduce your credit limits or even close your accounts — which definitely would adversely affect your credit score.

Key takeaway: Maxing out your credit cards could lower your score by as much as 120 points.

10. Consolidate small balances

Let’s say you have a credit card debt of 200 dollars on one card, 450 dollars on another, and 135 dollars on a third credit card. If possible, pay off those small debts either with a personal loan or by consolidating them onto a single (hopefully low-interest) credit card. Your credit report will reflect one monthly payment instead of several, which can improve your credit rating. Just don’t take the opportunity to run up new debts on your paid-off credit cards, or you will defeat the purpose of consolidating your old debts.

Key takeaway: Getting a loan may ding your credit score when you apply but it more than compensates for the bump you will receive for erasing your credit card balances.

Bonus strategy: Monitor your credit regularly

Have you heard the quote: “If you can’t measure it, you can’t improve it?” It also applies to your credit score. Consider signing up for services like Credit Sesame and Mint, which provide free credit scores along with copies of your credit report. That way, you can monitor the progress of your efforts.

If you know you’ll be seeking new credit in the foreseeable future, begin taking action as soon as possible to improve your credit score. Allowing at least a year is ideal, but even beginning several months in advance is good.

Key personal loan statistics

- Always pay your bills on time! Keep credit accounts current.

- Keep your credit utilization low. Pay down credit card balances to 30% of your limit or less.

- Only apply for credit when you need it. Keep credit inquiries to a minimum.

- Keep old accounts open — the length of your credit history matters.

- Reschedule your payment due dates for right after you get paid.

- Monitor your credit report and get errors corrected.

- Maintain a credit mix of revolving accounts (credit cards) and installment loans.

- Pay off delinquent accounts.

- Don’t signal possible credit problems to creditors.

- Consolidate smaller balances into one monthly payment.

FAQ on improving credit scores

How can I raise my credit score by 100 points?

One of the best ways to earn a great credit score is to always pay your bills on time. Missing one bill can lower your credit score by as much as 100 points. To begin your credit card recovery journey, make sure you pay all of your late payments and don’t miss another bill payment.

Is it possible to raise my credit score by 100 points in 3 months?

There is no specific amount of time guaranteed to be long enough to raise your credit score by a certain number of points. Many factors are involved in determining a credit score, and they are unique to each person and their credit history. In general, improving your credit score takes time and patience. It is not easily done quickly, but the soonest you could start to see results is 30 to 60 days, depending on your unique situation. However, it may take 3 or 4 months or even a year or more to move a credit score that much. The sooner you start the process, however, the sooner you’ll get there.

How long does it take for my credit score to update?

Account activity is reported to credit bureaus by credit card issuers and lenders once a month. The specific date will vary by lender, but you can confirm it by reaching out to creditors directly.

Does Credit Karma lower your credit score?

Having a Credit Karma account will not directly lower your credit scores. They request your credit report information on your behalf from TransUnion and Equifax. This is known as a soft inquiry, which won’t impact your scores. On the other hand, hard inquiries can influence your credit scores.

What is Experian Boost, and can it help my credit score?

Experian Boost is a service you can sign up for to get credit for paying cell phone and utility bills and even for making streaming service payments that are normally not reflected in your credit score. It is a useful tool to help build your positive payment history. You also get access to your Experian credit report and FICO scores with Experian Boost, as well as credit monitoring and alerts. Experian Boost can instantly raise your FICO credit score. At the end of the sign-up process, you receive an updated credit score showing how your score was actually affected.

How do I get the most accurate credit score?

If you are in the market for a loan, the best place to find the score most likely to be used by lenders is directly from FICO. Another option is to check out Credit Karma and/or Credit Sesame.

Can paying off collections raise your credit score?

Unfortunately, simply paying a collection account without getting it removed from your report often won’t improve your score. With few exceptions, as long as a collection account is listed on your credit reports, it’ll negatively affect your credit scores.

Where can I get a free credit report?

The three major credit bureaus have set up a central website and a mailing address to order your free annual report. You may get your free reports simultaneously or one at a time — the law allows you to order one free copy of your report from each credit bureau every 12 months. To get your free reports, visit AnnualCreditReport.com.

LJ

Lara is a personal finance writer that enjoys helping people live a balanced life. She covers the essentials -- think budgeting and healthcare -- and the finer things in life, such as food, travel, and design. In her free time, she enjoys reading, climbing, and cooking up globe-spanning fare for her favorite people.

Share this post: