15/3 Credit Card Payment Hack: What is It and Do You Need It?

EG

Summary:

The 15/3 credit card hack can help you lower your credit card utilization and boost your credit score. The hack involves making one credit card payment 15 days before the due date and a second payment three days before the due date. You then pay any remaining balance the day before or day of the due date.

When you’re struggling to boost your credit score, it can sometimes feel like nothing works. Even when you make your monthly payments on time, it can feel like your credit score just won’t budge.

If you’re having a hard time boosting your credit score, you aren’t alone. The good news is there are ways to improve your credit score. The 15/3 credit card hack is one of them. Here is how it works.

Compare Credit Cards

Compare the rates, fees, and rewards of leading credit cards.

What is the 15/3 credit card hack?

The 15/3 credit card payment hack is a method of paying down your credit card balance in a way that boosts your credit score. The basic premise is that you make two monthly payments on your credit card: one payment 15 days before your due date and the other three days before your due date. If you have any remaining balance, pay that on or before your due date.

Pro Tip

Your statement date is the day your monthly billing statement closes and your statement is generated. You can find it on your latest credit card statement.

How the 15/3 credit card hack improves your credit

There’s a bit of confusion as to how the 15/3 hack improves your credit. Some financial experts advise that when you follow this strategy, you’ll have two monthly payments appear on your credit history each month. This claim simply isn’t true. No matter how many payments you make each month, your credit history will look the same, since your credit card issuer reports your outstanding balance once per month.

However, that doesn’t mean the 15/3 hack can’t still benefit your credit. The other reason personal finance gurus recommend this method is that it can lower your credit utilization ratio.

Lowering your credit utilization ratio

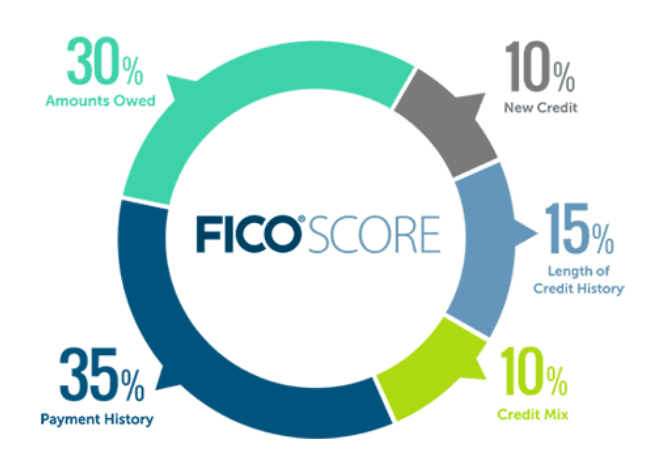

Your credit utilization is the percentage of your available revolving credit that you’re using. So, if you have a credit card with a $1,000 limit and have a balance of $200, your utilization is 20%. Credit bureaus and lenders generally like to see a credit utilization below 30% of your total credit limit.

Your credit utilization ratio is one of the most important factors that impact your credit score, and it accounts for about 30% of the calculation. The higher your utilization, the lower your credit score is likely to be, and vice versa.

Your utilization is based on your credit card balances as they’re reported to the credit bureaus. The goal of the 15/3 credit card payment hack is to keep your revolving credit balances low so that when they’re reported to the credit bureaus, you have utilization below the desired percentage.

15/3 credit card hack example

Let’s say you spend $1,000 per month on your credit card for day-to-day expenses. If you just pay your credit card bill on the payment date, then your credit card company would report a $1,000 statement balance to the credit bureaus.

If you had a credit limit of $2,000, then you would have a credit utilization rate of 50%, which is higher than credit bureaus like to see. Even though you pay off your credit card in full each month, you could still see a negative impact on your credit score.

Using the 15/3 hack, you would make a payment of $500 15 days before your credit card due date. Then, you’d make another $500 payment just three days before your due date. Finally, if you made any additional purchases before the due date, you would pay off the remaining balance.

When the credit card company reports your monthly activity to the credit bureaus, you would have just a small balance — just enough to show the credit bureaus that you’re using your card, but not high enough to hurt your credit score.

Pro Tip

Most credit card issuers won’t allow you to set up automatic payments to implement the 15/3 hack. Instead, set a reminder on your calendar to make the necessary payments on the correct dates.

Does the 15/3 credit card hack work?

When it comes to whether the 15/3 credit card payment hack actually works, the short answer is: sort of.

Your credit card company may report your monthly balance to the three credit bureaus on or around your statement date. And it’s absolutely true that making payments on your credit card throughout the month — especially before the due date — can reduce your credit utilization, and therefore help you improve your credit score.

However, the specific numbers of 15 and three days before your due date are somewhat arbitrary. There’s no real basis to choosing those dates. You could use practically any combination of dates and the impact would be the same. In fact, paying your balance half way through the month and in full before the payment is due is probably a simpler and more effective method to lower your credit utilization rate.

As we mentioned previously, the 15/3 hack also doesn’t work entirely as some personal finance educators claim it does. Even if you make multiple payments on your credit card each month, you’ll still have just one addition to your payment history on your credit report.

Rather than worrying about credit multiple payments, you could also just make a single payment before your due date to ensure your balance is low when it’s reported to the credit bureaus.

Paying before statement date vs. due date

Since we’ve talked a lot about paying before your statement date and due date, it’s important that you know the difference between paying before these dates. Paying your credit card balance before the due date can improve your payment history, which then gradually improves your credit score.

Paying before your statement date lowers your credit utilization. Though your statement date isn’t always the same date credit card companies report to credit bureaus, making a payment before your statement date generally reduces the amount of credit the bureaus think you’re using.

One of the best ways to improve your credit score is through secured credit cards. A secured credit card requires a cash deposit with the issuer before you can open an account, making it available to those with fair or poor credit.

Should you use the 15/3 credit card hack?

If you’re struggling to boost your credit score, you might be wondering whether the 15/3 hack is the thing to help you do it. And depending on your situation, it may be worth a shot.

Great for you if…

First, the 15/3 credit card hack might be a good idea if you’re working to boost your credit score and you have a low credit limit. Because you have a low limit, every little bit makes a difference in your balance, and using more than 30% of your available credit can harm your credit score.

The 15/3 hack is also worth considering for people who use their credit cards for everything. Even if you’re a responsible credit card user who pays off your full balance each month, charging everything to your card throughout the month can rack up a large balance.

But when that balance is reported to the credit bureaus, they don’t necessarily know you’ll be able to pay it off. They can only make assumptions based on the information reported to them — and at that time, you’re carrying credit card debt. Making a payment before the statement date can reduce the impact on your credit score.

Not right for you if…

As we mentioned previously, you don’t necessarily have to abide by the 15/3 rule. You’ll get the same benefit by paying off your balance on any date leading up to your statement date.

It’s also important to remember that paying your balance before your due date isn’t the only strategy to implement when boosting credit scores. Other tips you can use in conjunction with this one include:

- Make every monthly payment on time, whether it’s on your credit card or your utility bill

- Paying off any credit card debt you’ve been carrying (pay more than the minimum payment to help you get ahead)

- Keep your credit card account open even after you’ve paid off your balance

- Avoid too many new inquiries on your credit report

FAQs

Is the 15/3 credit card hack real?

Yes, the 15/3 credit card can be a legitimate way to improve your credit score by reducing your credit utilization. However, there are some misconceptions about it. It won’t result in additional reports on your credit history, nor do the payments necessarily have to happen 15 and three days before your due date.

How do you “trick” your credit score?

There aren’t really ways to legally trick your credit score. The best way to improve your credit score is simply to use your credit cards and other debt responsibly, including reducing your credit utilization.

Is it good to pay a credit card early?

Yes, paying on your credit card early can help your credit score by reducing the balance that’s reported to the credit bureaus.

Does making two payments a month help credit?

There’s little difference in your credit score between making one or two payments on your credit card. The real benefit comes from paying down your balance before it’s reported to the credit bureaus, whether it’s with multiple payments or just one.

Key Takeaways

- The 15/3 credit card hack requires that you pay half your credit card balance 15 days before your due date and the other half three days before your due date.

- The 15/3 hack has the benefit of reducing your credit utilization, which can help to boost your credit score.

- There are some misconceptions about the 15/3 hack, including the fact that just one payment before your due date will accomplish the same goal.

- The 15/3 hack or another similar method might be right for you if you have a low credit limit or use a large percentage of your credit limit each month.

EG

Erin Gobler is a Wisconsin-based personal finance writer with experience writing about mortgages, investing, taxes, personal loans, and insurance. Her work has been published in major outlets, such as SuperMoney, Fox Business, and Time.com.

Share this post: