Is It Better To Get a 15-Year vs. a 30-Year Mortgage?

MG

Last updated 03/08/2024 by

Marcie GeffnerAlmost all home mortgages have a term of either 15 or 30 years.

The term is the length of time you have to pay off the loan through a pre-set schedule of monthly payments. As the name suggests, the 15-year loan allows 15 years. The 30-year loan allows 30 years.

So, which is better: a 15-year mortgage or a 30-year one? Let’s take a look.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

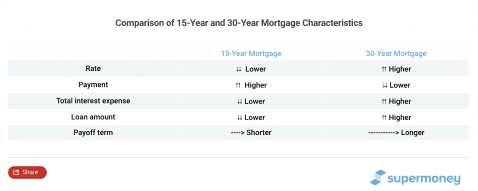

15-year vs. 30-year mortgage: which is better?

“This is a tough question, as every client is different,” says Adam P. Smith, president of Colorado Real Estate Finance Group, a real estate finance firm in Greenwood Village, Colo.

In other words, the right answer depends on your objectives.

A 15-year mortgage might make sense if you:

- Want to save money

- Want to force yourself to pay off your loan sooner

- Are confident you can afford a higher payment

A 30-year term might make sense if you:

- Want to qualify for a larger loan amount

- Want a lower payment

Discover how to buy a home with 10% down and no PMI with mortgage lender SoFi.

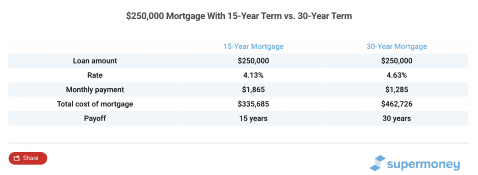

Before you choose between a 15-year mortgage and a 30-year mortgage, you should compare your options to get a clear picture of which works best for your personal situation.

Here’s an example:

Notice that the shorter term has a lower rate and higher payment. Also notice that the payment is a lot higher, $580 per month, but the total cost of the mortgage is lower.

Sold or refinanced

Most people don’t keep the same mortgage for 30 or even 15 years. More often, they sell their home or refinance before the term ends.

Some people get a 30-year mortgage when they buy a home and then later refinance into a 15-year when they’re earning more money, can afford the higher payment, and are closer to retirement when they want to be mortgage-free.

Refinancing into a 15-year loan can let you lock in a lower rate if market rates are lower or comparable when you refinance. If market rates are higher, this strategy might not work for you.

You can also get a 30-year loan and later refinance into another 30-year loan. That would give you more time to pay off your loan. Your rate and payment might be lower or higher.

Looking for a VA lender? Read our review of Veterans United Home Loans

You can make higher payments

If you want to pay off your loan sooner, but you’re not sure you’ll be able to afford the 15-year loan’s higher payment, you can get a 30-year loan but make the 15-year payment.

Your rate will be a bit higher, but if you experience a temporary job loss, illness, or disability, you won’t be locked into the higher payment.

You’ll also have more flexibility in your budget if your financial priorities change.

The downside is that making a higher payment every month when it’s not required takes “a certain amount of diligence” that many homeowners don’t have,” Smith says.

You can make extra payments

You can make extra payments on your mortgage of any amount at any time regardless of whether your term is 15 years or 30 years.

Some homeowners make one extra payment each year to pay off their mortgage sooner, but without the long-term commitment of the 15-year mortgage’s higher payment. Other people pay more whenever they can.

Either way, you’re not locked into the full term of your mortgage if you want to pay it off sooner.

Ready to get started?

Finding the right mortgage lender can make all the difference in the world. That’s why it’s important to do your research.

Review a list of top mortgage lenders to compare terms and find your best plan.

MG

Marcie Geffner is an award-winning freelance reporter, editor, writer and book critic. Her work has been featured online and in print by The Washington Post, Los Angeles Times, Chicago Sun-Times, Urban Land, Business Start-Ups and Fox Business Network Online, among many other newspapers, magazines, and websites. With a bachelor’s degree in English from UCLA and MBA from Pepperdine University in Malibu, Geffner has impressive credentials in both story-telling and business management. A second-generation native of Los Angeles, Geffner now lives in Ventura, California, a surf city northwest of her hometown.

Share this post: