Believe It or Not, Real Estate Affordability Hasn’t Changed Much in 40 Years

AL

Last updated 04/08/2024 by

Andrew LathamThe average sales price of a home has increased by more than 2000% since 1963.

In 2020, the median sales price of a home was $391,300. That is 20 times the $19,300 average sales price in 1963! How can you say housing affordability hasn’t changed? Consider all the data before you jump to a conclusion.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

Inflation-adjusted house prices paint a more accurate picture

First, the graph above shows the average sales price, not the median. The average price of homes can be distorted by houses that sell for very high or low prices. Median prices are usually a more reliable measure of the typical home price.

Second, you need to take into account inflation to understand how prices have really changed. Sure. Maybe the average price of a house in 1963 was $19,300. But the average wage was also $4,500. A gallon of gas cost 30 cents. And you could buy a dozen eggs for 55 cents.

The graph above shows the median inflation-adjusted house prices from 1975 to 2020. Although the price hike is not as dramatic, you can still see that house prices are much higher than historical averages. This could indicate we are are in another housing bubble similar to the one in 2005/2006. But there is another factor to consider.

Case-Shiller indices

Another way to compare the cost of housing over time is to use repeat-sales indices, such as the Standard & Poor’s CoreLogic Case–Shiller Home Price Indices. There are several Case-Shiller indices which are based on original work by economists Karl Case and Robert Shiller, who studied home pricing trends by comparing repeat sales of the same homes. The graph below shows the inflation-adjusted Case-Shiller and Real Building Cost indices for the United States from 1898 to 2019.

Although the Case-Shiller index is still not at a record high, we are not for off from the 2007 peak. By the end of 2019, the Case-Shiller index was similar to that of 2005, which was when Robert Shiller published the second edition of Irrational Exuberance and expressed concern about the sustainability of home prices because incomes were not keeping up with the rise in housing costs.

Wages have not kept up with housing prices

Now compare the rise in the median price of a home to the median income of Americans.

If you adjust for inflation, the median income of Americans has only increased by 33%. The median housing prices, however, have increased by 60%. It’s even worse when you look at the income of younger adults. For instance, the median income of people between 25 and 34 only increased by $30 in 44 years (1974 to 2017). It’s no wonder homeownership rates among Millennials are lower than for previous generations.

New houses and GDP

Are we really spending more on new houses than in the past? It certainly feels like housing is more expensive than ever. However, we are spending less on new homes as a percentage of gross domestic product (GDP) than in 1963, and half what we were spending in 2005. Using GDP as a benchmark for consumer spending is not without problems. However, it does paint a picture of the residential construction industry and housing expenditure over time. The graph below shows changes in the index of money spent on new homes divided by GDP from 1963 to 2020.

We spend relatively less now, but we are getting back on track in a hurry. The graph also illustrates well the effect recessions have on house sales. Every recession from 1973 is preceded by a sharp drop in the index. This index also speaks to the volatility of the construction industry, which can fall 145 points in just 4 years (2005 to 2009).

New homes are 47% larger than 40 years ago

Inflation, stagnant incomes, and statistical outliers are not the only reasons many people cannot afford to buy a home. Our taste for larger homes is also a significant player. In 2018, the median-sized new home was 781 square feet larger than 1978. Yet, the size of homes is a factor that is often ignored.

When you also factor in inflation, the price per square foot has remained pretty stable. Look at the price per square foot (inflation-adjusted) for new homes in the graph below.

In 2017 the price per square foot of a new home was only 4% more (about $3) than in 1979. Which no longer sounds like much of a real estate bubble. Particularly when you think about the amenities that are now standard for new homes.

In 1978, only 8% of homes had three or more bathrooms and just 63% had air-conditioning. Now, 40% of new homes have three or more bathrooms and 94% come with air-conditioning.

In 2019, the price of new homes dropped, but the median size of homes dropped even more, which increased the median price per square foot to $137.50.

Of course, this only shows the overall price for the entire United States. It gets messier when you look at prices at the regional level.

The data for the Northeast and the West of the United States explains why so many feel the real estate market is about to implode. These regions have seen the greatest price increase: $63 and $19 in the last 40 years.

Although we are probably seeing a housing bubble in California and New York, the data shows a different story in the Midwest and the South.

However, the story is completely different in the Midwest where the price per square foot actually dropped by nearly $20. Buying a home in the Midwest is — when you correct for size and inflation — cheaper now than in 1978.

Let that sink in.

In the South, the price per square foot has hardly changed. It has the lowest housing prices in the country and has closely followed the trend of the United States as a whole.

If you adjust for inflation, you could buy a house for practically the same price as 40 years ago. The key is keeping the size of the house to what was “normal” 40 years ago.

Obviously, using median pricing has its drawbacks. When prices become less volatile it can give the appearance of a collective increase or decrease in price, but it all depends on how the numbers are distributed. Neither median or average prices can give an accurate prediction of market direction. To do that, you need to have a deep understanding of the local housing market. Factors like the sales price of comparable properties, the local job market, and the average age of the population are key on city and neighborhood level.

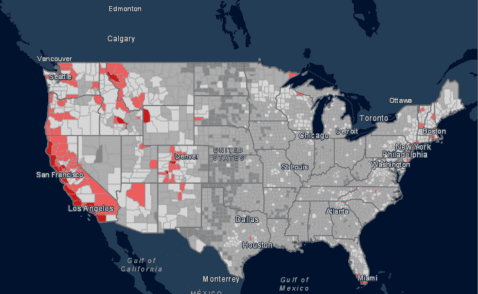

The Housing Affordability Index

A useful index to determine whether house prices are in line with what people can actually buy is the traditional housing affordability index. It shows what percentage of a population can afford to buy the median-priced home in a given region based on their income.

A low affordability index can be another sign of a housing bubble. As you can see from the map below, the majority of the United States counties provide reasonably affordable housing. It also shows hot spots where housing is less affordable in the United States. In some densely populated areas, residential properties are too expensive for the average household to purchase a home.

Large swaths of the West Coast and Northeast are unaffordable. In this map, California is a predominantly red state. Employment hubs like San Francisco, San Diego, and Los Angeles have particularly prohibitive housing costs. Compare the average housing affordability of the United States, 53 to California’s 26. This means that only 26% of Californians can afford a median-priced home in their state. The situation is similar in New York, particularly in metropolitan areas. So yes, California and New York are probably in a housing bubble. However, On the national level, 53% of Americans have the necessary income to qualify for a median-priced home in their state.

The bottom line

We are probably not looking at another housing bubble at the national level. Houses are much more expensive now, even when you adjust for inflation. Wages have not kept up with the increase of prices, which compounds the problem housing affordability. But the size of the median home has also increased. In fact, the US median cost of a square foot has remained relatively stable in the last 40 years.

Even though households are smaller, we crave for larger homes. This rises house prices dramatically. However, foot by foot the affordability of new homes has barely changed. If you adjust for inflation, you could buy a house for practically the same price as 40 years ago. The key is keeping the size of the house to what was “normal” 40 years ago. The good news is you can find some great deals in your area, if you are willing to buy a house the size of your grandparent’s home. The bad news is houses that size or hard to find.

The story changes drastically when you look at the West Coast and sections of the Northeast, particularly around big cities. In areas such as the Bay Area, we may very well be dealing with a housing bubble. Read our 2020 Mortgage Industry Study to see what has been causing this cycle of booms and busts in many large cities.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: