The Ultimate Personal Finance Guide for Fresh out of College Grads

AH

Last updated 03/19/2024 by

Audrey HendersonAs a freshly minted college grad, you may feel as though you can take on the world.And why not? With your hard-earned degree and a shiny new job offer in hand, you should feel proud of your accomplishments.

But what if you’re not that confident new grad everyone expects you to be? You may be anxious about how to approach the next phase of your life, especially if you’re living with Mom and Dad because you can’t find a job that pays enough money to live on your own.

In either case, you have the advantage of making a fresh start. Along with mapping out your career and perhaps searching for a life partner, getting your financial house in order is an essential element of getting off on the right foot, giving you a better chance to create a productive, positive future.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Face Up to Student Loans

If you were able to complete your education without taking on massive student loans, lucky you. You are definitely the exception. In 2012, the average debt loan for students was a hefty $29,400, according to the Institute for College Access and Success. Paying off that type of loan debt can take years, if not decades.

Related article: Grieving? You May Have to Pay off Your Private Student Loan

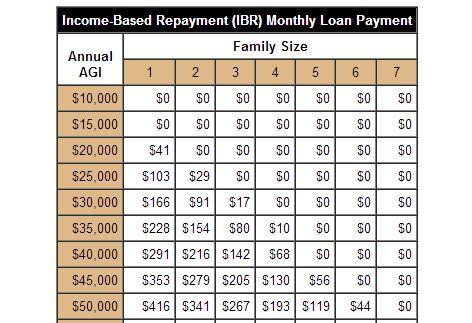

It’s likely that when first taking on the federal student loan you chose the Standard Repayment Plan, which would need to be repaid in 10 years time. The hundreds-per-month bill that’ll be coming up in a few months has likely frightened you into hiding the reminders and pretending they don’t exist. That’s where plans like Income-Based Repayment (IBR) come in.

Most federal student loans are eligible for at least one income-driven repayment plan. – Federal Student Aid

New college grads can often negotiate lower monthly payments that are in line with entry-level salaries. Through these plans, and if you qualify, you’ll only pay 10-15% of your discretionary income. The chart below shows the monthly payment for IBR in 2012, at a 15% rate up to an income of $50,000.

Nonetheless, if you are feeling overwhelmed by repaying your government-issued student loans, look into deferment, forbearance or re-consolidation options. Privately issued student loans may be more difficult to negotiate, but if you’re struggling, it doesn’t hurt to make the effort. Whatever you do, don’t ignore the problem.

MoneyUnder30 has an excellent post on what happens if you don’t pay your student loans. (It isn’t pretty)

Take Advantage of Tax Breaks and Accelerated Savings

While it is true that you cannot deduct job hunting expenses for your first job, you can claim tax breaks for moving expenses if your new job is located far from your present location. The interest from your student loan payments may also be tax deductible.

If you join a company with a 401(k) plan, contribute as much as you can afford, especially if your new company matches your contributions. Because traditional 401(k) plans are funded with pre-tax dollars, each $1,000 that you contribute only takes a $750 bite out of your income if you are in the 25 percent tax bracket.

Start saving now, even if it’s only a few dollars every week. You’ll develop strong financial discipline that can help you navigate rough financial seas in the future. Plus, saving money in your 20s almost like growing a money tree. According to calculations by TD Ameritrade reported in U.S. News and World Reports, an individual saving a modest $100 per month will have accumulated $471,358 by age 67, assuming an 8 percent annual return on investment. If that same person were to wait until age 41 to begin saving, at age 67 he or she would only have accumulated $59,295.

Protect Yourself (and your Stuff) With Insurance

Look in the mirror and say out loud: “I am not indestructible.” Because you’re not. Do you have the cash to replace your computer, cell phone, wardrobe, car, furniture and Doctor Who memorabilia in case of natural disaster? Unless you are a Hollywood megastar, a Silicon Valley mogul or an elite professional athlete, you really don’t. Besides, do you really want to deal with the consequences of a car wreck without insurance?

Don’t think of insurance coverage as a downer. Consider it as a means of protecting your future, because that’s precisely what it is. The good news is that – except for maybe car insurance – you probably qualify for really low premiums because you’re young and your stuff is probably worth maybe a few thousand dollars, not millions.

Develop a Real, Grown-Up Budget

Especially if you lived on a Spartan budget in school, it’s tempting to blow nearly all you earn from your first full-time paychecks once you begin working. Try to resist the urge. Instead, assess your expenses and your assets and develop a grown-up style budget. Include student loan debt, savings, utilities and other monthly expenses such as your car note and, oh yes, rent. You should also leave room in your budget for entertainment and socializing, even if you are otherwise on a strict budget.

If you’ve always depended on Mom or your dormitory cafeteria for meals, you’ll need to learn how to shop for food. And yes, teach yourself how to prepare at least a few basic dishes for survival. Eating at home is much less expensive, often healthier and even tastier than always eating out. While you’re at it, learn how to sort and launder your clothes and keep your surroundings clean. If you’re boarding with your parents, lending a hand with the chores is one way to avoid being a freeloader while you’re living rent-free.

Just Because You Can Spend Money, Doesn’t Mean You Have To

Just because you’ve finally got a paycheck coming in doesn’t mean you have to buy everything in sight because you can, or you think you deserve it. If you’ve gotten through college without a car and live close to your job, stick it out for a few more years. If you’re lucky enough to be able to live at home rent-free for a while, do it and pocket the savings. Don’t try to justify camping out overnight for the latest iPhone because Apple!

Be honest with yourself about whether you’re investing in something useful or simply indulging meaningless overspending. Here’s a hint: If you can no longer read the numbers on your credit cards because they’re so worn, put down the plastic and gently back away.

This is not to say that using credit cards is always bad. After sleeping on a twin mattress supported by milk crates for three or four years, you deserve a proper bed. You probably do need to beef up your wardrobe, especially if your first job calls for business casual. You may even need a car to get to and from work. If your cash flow is not up the task, then yeah, you’ll probably need to use credit. Take a look at SuperMoney’s top credit cards of 2014 article to choose the best credit card for your needs.

The occasional splurge is OK, especially if it’s your mom’s birthday or you’re serving as best man or maid of honor at your best friend’s wedding. Imposing inflexible financial discipline upon yourself with no room for fun is a tailor made recipe for a full-blown spending spree – often when you can least afford it. Just plan ahead for major expenses that you know about in advance.

Besides, a long history of on-time credit card payments will make it that much easier to qualify for a bigger loan or mortgage down the road. So go ahead and obtain one or two credit cards if you didn’t pick up any in college.

But don’t get into the habit of paying only the monthly minimum payment while piling on debt, no matter what Suze Orman says on the subject. Stay well under your credit limits and pay your balances off on time, every month.

Consider Short and Long Term Career Goals

Especially in a tough job market, you may feel grateful if you are able to find a job at all. But once a company has made the decision to hire you, you have leverage. You are the candidate they want, and they DON’T want to have to begin the entire search process again. Use this leverage to negotiate the best salary and benefits package possible. You’ll develop valuable skills that you can use to obtain more lucrative employment packages as you move up within the company or seek work elsewhere.

Great article from Forbes: Here’s How To Negotiate Your Salary

Consider long-term career goals as well. Unless you are a concert pianist who began playing at the age of four, it is unlikely that your present job represents your ultimate dream job. Even if you are convinced that you are in the right career field, it is almost inevitable that you will change jobs and even companies several times in your life.

If progressing in your career requires additional education, consider how you will finance graduate school or vocational training. Will your employer pick up at some of the tab? Do you even need another degree? Take an objective assessment of whether sinking thousands of dollars and years of your life into an advanced degree will yield a worthwhile return on investment. Perhaps you can obtain the training you need through online instruction, noncredit courses or studying and reading on your own.

Speaking of self-study, carve out time during the evening or on weekends to pursue a hobby that could blossom into a second career. Take credit or noncredit courses in new technology, especially advances related to your field. Unless your endeavors are in direct violation of company policy or adversely affect your performance on the job, you should not feel guilty. Think of it as protecting your professional future because if your “dream job” turns into a nightmare, you’ll have something you’ll love on the side.

It’s Not All About the Benjamins

Many older people carry deep regrets about not following their dreams when they were younger. Don’t be one of them. If you’ve always wanted to be an actor, move to New York or Hollywood. If you can’t afford to move, join your local theater guild and keep the dream alive. Or take that iconic coming-of-age trip around the world now while you’re relatively unencumbered.

None of this means walking away from the love of your life, never setting down roots or not getting married. But think twice about tying yourself down to a mortgage, and a life in your home town, especially if you may want to relocate in the future. Likewise, consider holding off on starting a family, at least until you are settled in a place where you’d like to live long term. The house with the white picket fence will still be there when you’re in your 30s, or even your 40s.

The key is to remember that time is on your side, and you’ve got the opportunity to live the life your elders wish they could. Time is a tool. A valuable tool; an essential tool – but a tool. Being smart with how you plan your life and use your money now means that you’ll likely to be able to do the things that matter most to you in life. Isn’t that really what it’s all about?

Image Credit: Steve Wilson

AH

Audrey Henderson is a Chicagoland-based writer and researcher. She holds advanced degrees in sociology and law from Northwestern University. Her writing specialties are sustainable development in the built environment, policy related to arts and popular culture, socially and ecologically responsible travel, civic tech and personal finance.

Share this post: