How to Stop an IRS Wage Garnishment

AL

Last updated 03/15/2023 by

Andrew LathamUnfortunately, getting a wage garnishment for tax debt is more common than you might think. In 2020, the IRS requested over 780,000 notices of levy on third parties, which includes garnishing wages from employers. The IRS has up to 10 years from the date taxes were assessed to collect them — even longer if there is evidence of fraud.

This guide will explain what a wage garnishment is, how it works, how to stop it, and what you should do if you receive a notice of garnishment from the IRS.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is Wage Garnishment?

Wage garnishment is a process of withholding earnings from an individual to repay a debt. In the case of wage garnishments, the debt in question is in unpaid taxes. In other words, the IRS files a wage garnishment to collect money from taxpayers who failed to pay owed taxes, and the IRS will send written notice to the taxpayer. They will require the taxpayer’s employer to withhold a portion of the taxpayer’s wages and send that withheld money directly to the IRS. They can even garnish other types of income, such as 1099 wages.

If you receive a notice of wage garnishment, the IRS may say something like, “Contact us to establish a payment plan to pay down your tax debt.” Otherwise, part of your paycheck will be withheld until:

- You make other payment arrangements to handle your tax debt.

- You pay your tax bill and all associated interest and penalties in full.

- The IRS releases the tax levy.

When does the IRS initiate wage garnishments?

Wage garnishment isn’t the IRS’s first step in pursuing the money they’re owed. Here is the standard process which may lead to garnishment:

- The IRS assesses your tax liability and demands payment for it.

- You ignore the notice demanding payment or refuse to make arrangements to pay your back taxes.

- The IRS sends you a federal tax bill entitled “Final Notice of Intent to Levy and Notice of Your Right to a Hearing.”

- 30 days pass without you taking any action to make arrangements to pay your debt.

Only after these steps can the IRS begin the levy process and compel your employer to withhold your pay.

How can I stop an IRS wage garnishment?

The IRS does not want to have to deal with wage garnishment any more than you do. As such, there are several ways to stop it even after the process starts.

Methods for stopping your Wages from Being Garnished

- Pay your tax debt in full.

- Enter into an installment agreement with the IRS to pay all taxes due.

- File for an offer in compromise.

- File for bankruptcy. This won’t release you from having to pay your tax debt in full, but it can stop the IRS from garnishing your wages for collection purposes.

- Quit your job. But this is a short-term solution. Even if you have no wages to collect, the IRS can still seize your property to collect the debt — and unemployment leaves you with no income to replenish the loss.

Responding to the IRS

If you receive notice of an IRS wage garnishment, it is important to take action right away to discuss your options. The IRS doesn’t want to garnish your wages. It is costly for the government, and it can create difficulties for the IRS, you, and your employer. So if you reach out and show a willingness to work together on a solution, you may be able to avoid garnishment entirely.

The IRS Fresh Start Program

The IRS Fresh Start program offers tax relief solutions to help you avoid wage garnishment. By setting up an installment agreement, you can pay your debt in affordable monthly payments. Or, if you qualify for an offer in compromise, you may be able to reduce your debt entirely. To learn more about the tax relief solutions available to you, read about the IRS Fresh Start program.

So be sure to contact the IRS right away when you receive a notice of delinquent taxes. If you’re proactive and cooperative, you can stave off wage garnishment. Increasing your withholding amount from each paycheck can help get you back to receiving tax returns every year.

How much can the IRS withhold from my paycheck?

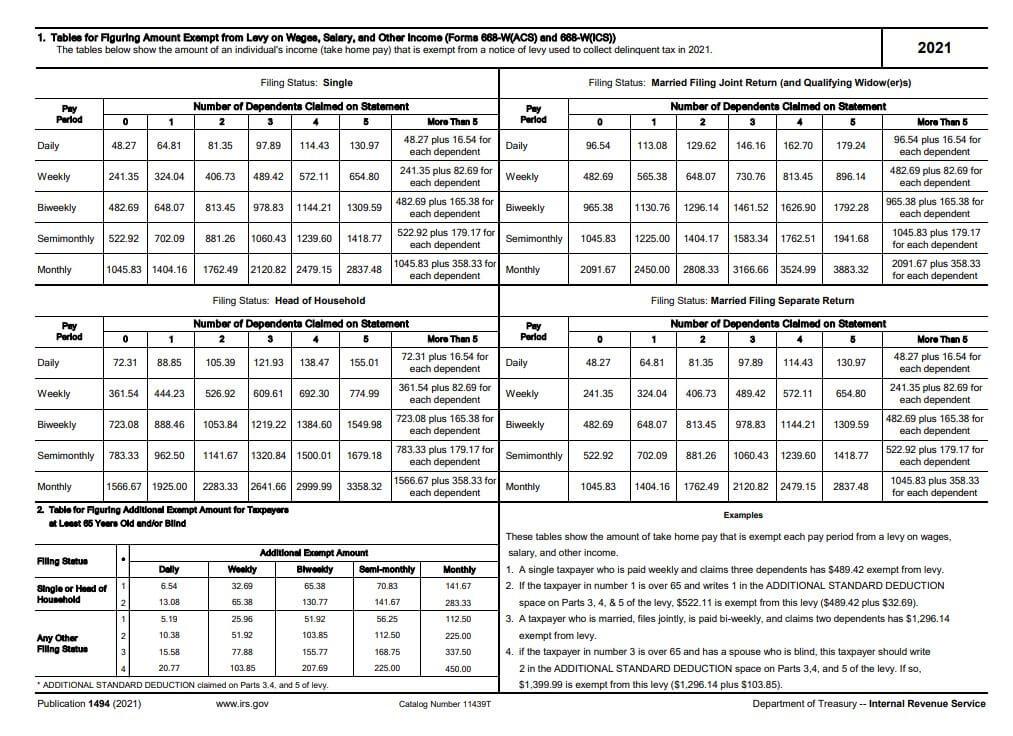

The percentage of your wages you’ll keep during an IRS garnishment is based on the standard deduction and the number of personal exemptions you can claim. The IRS uses the tables in Publication 1494 to calculate how much of a taxpayer’s income (take-home pay) is exempt from a wage garnishment (or a notice of levy) to collect delinquent tax in 2021.

The IRS bases its guidelines on what it deems will leave you enough money for regular living expenses. Typically, the IRS will garnish up to 15% of your wages. However, if you have other income sources, the IRS may allocate the exemptions to your other income sources and levy on 100% of your wages from a particular employer. The IRS can also levy any extraneous income supplements, such as bonuses or commissions.

That’s why it’s essential to contact the IRS to make other arrangements if possible. Garnishment can upend your lifestyle and shatter your budget — you should pursue alternatives if possible.

If you’re unsure how to set up an alternate payment plan, consider hiring a tax attorney to help you negotiate with the IRS.

The IRS may can levy up to 100% of your paycheck if you have other sources of income.

What should you do if you are experiencing financial hardship?

Wage garnishment is hard for everyone, but your financial situation must meet the IRS definition for financial hardship to appeal a garnishment.

According to the IRS, “An economic hardship occurs when we have determined the levy prevents you from meeting basic, reasonable living expenses. For the IRS to determine if a levy is causing hardship, the IRS will usually need you to provide financial information, so be prepared to provide it when you call.”

If the IRS determines that the wage garnishment is, indeed, creating financial hardship for you, they may release the levy. However, this does not mean that your tax debt is forgiven. You will still have to pay your tax debt even after the IRS releases the levy.

How can I avoid Tax Debt and Wage Garnishment?

The best way to avoid a tax levy or garnishment is to file and pay your taxes when due. If that is impossible, you can:

- File for an extension.

- Set up a payment plan and make monthly payments.

- Make a settlement or installment agreement with the IRS.

And remember, respond to all notices you receive from the IRS as soon as possible. If you receive a final notice, it could be your last chance to take action before the IRS takes legal action. Even if you cannot pay your tax debt, it is still imperative to take the time to contact the IRS to discuss all your options.

Who can help me with IRS wage garnishment?

If you are uncomfortable dealing directly with the IRS, you may find it helpful to hire a tax attorney. These professionals are well versed in handling all tax-related issues. Their experience with tax law lets them maximize results in negotiations with the IRS. They can also prevent you from sharing any sensitive information with the IRS that might trigger an audit.

If your wages are already being garnished, a tax attorney may be able to put a hold status on your garnishment while they negotiate a settlement. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee, offer a free consultation, and charge competitive rates. This means that you would still have access to your funds as long as the negotiation progresses.

Tax analysis can help prevent wage garnishment

By analyzing your financial, tax, and employment situation, a tax attorney can help you determine the best type of settlement for your situation and even stop IRS wage garnishment before it starts. After reaching a settlement, you can once again enjoy a good standing with the IRS.

Ready to get started? Compare and contrast top tax relief companies here. Or, if you’d rather negotiate on your own behalf, click here to educate yourself about the tax relief options available to you. Plus we have a list of debit prepaid cards that can help you avoid garnishment

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: