How Much Money Should You Save From Your Salary to Be a Millionaire?

JL

Last updated 03/20/2024 by

Jennifer LeonhardiSaving money for retirement is something that just about everyone knows they should be doing. The sad reality, however, is that very few of us are actually saving enough money to allow us to be able to enjoy a financially comfortable retirement. So, how much money should we be saving each month towards our retirement? That all depends on how much you hoped to have saved up by the time you retire. If you have a goal in mind that you want to be a millionaire by the time you retire, then you may have to work a bit harder than the average Joe. Plus, there are always several other factors that are different for every situation.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

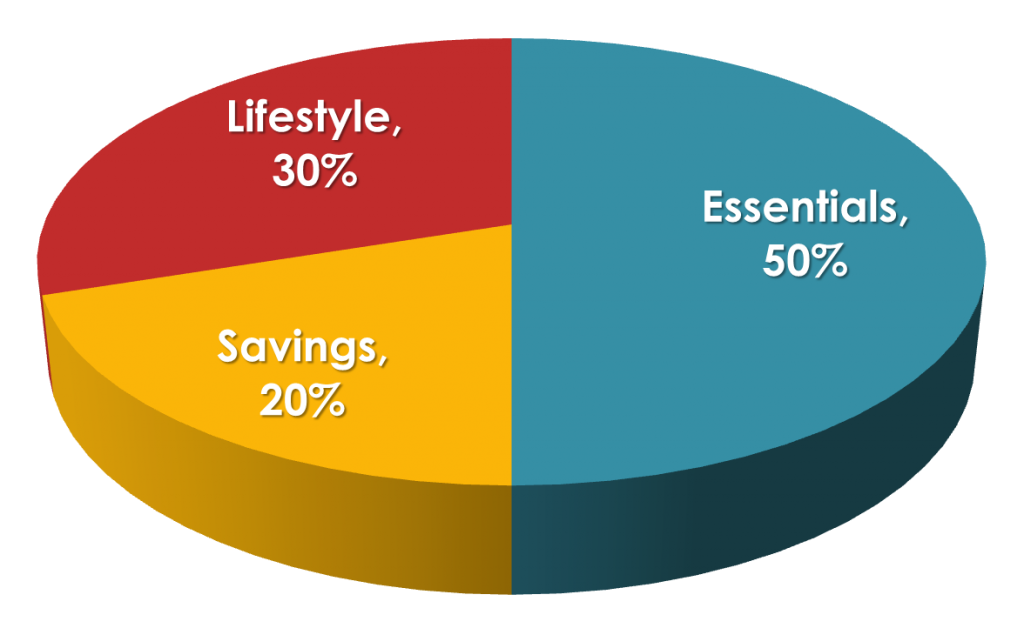

Using the 50-30-20 formula

This method of figuring out how you should be budgeting your monthly income is one of the most popular and easiest to use. Start by figuring out what your total net income is for the month, or your “take home” pay. Once you have this figure, you can break it down by the following:

- 50% should go to pay for all of your necessities. This includes things such as rent, utility bills, food, gas, etc. These are the things that you cannot live without.

- 30%should be allocated to discretionary items such as the cable bill, cell phone bill, entertainment, clothing, weekend fun, etc. These are the things that you enjoy doing but aren’t required for basic survival.

- 20%should be put aside for savings. At least half of this amount should go directly into a retirement account, but the remaining funds allocated here can be used for shorter-term savings goals. For example, buying a new car or taking a family vacation. A portion of this money should also be put aside for emergencies.

So, let’s say that John Smith earns a salary from his employer that yields $2,500.00 a month in take-home pay. With the rule above, his budget would break down something like this:

$1,250/month: Rent or mortgage payment, utilities, food, car payment, and gas for a vehicle. This category should include all of the expenses that he simply cannot live without. When you consider all the things that fall under this category, the amount Mr. Smith should be paying for his housing ideally should be less than 1/3rd of his total net income.

$750/month: Luxury items that Mr. Smith could probably live without, but doesn’t want to. This includes his cable tv, weekend golf trips with friends, and his habit of buying nice shoes.

$500/month: Savings put aside each month. At least $250-$300 of this should go to an IRA or 401(k) plan, but the rest can be put aside to save up for the new car he wants. If he hopes to be a millionaire by the time he retires, he will want to adjust this savings amount to be higher.

The age factor

The example listed above may seem simple enough, but the truth is that it simply will not work for everyone. Age is a huge factor when determining exactly how much someone should be saving each month toward their retirement. Not only their current age, but the age at which they wish to retire as well.

It is important to figure out how many good working years you have left in you before you want to enjoy your retirement. The more years you have left, the less you will have to save each year towards that goal. But if that date is quickly approaching and you don’t have anything saved up yet, you may need to make some significant changes to your monthly budget to be able to retire at all.

The other part of the age factor is to consider how long you plan on living once you’ve have retired. If you plan to retire at an earlier age, this hopefully means that you will have a longer retirement period to enjoy. And a longer one to fund as well.

On the contrary, if you plan on working later into those golden years, you will more likely have less time without work to have to worry about. To prepare for a financially secure retirement, it’s important to be realistic about how many years you might be able to enjoy the retirement period for.

The overall goal of figuring out how long you will live as a retired individual is to be able to “ballpark” how much money you will need to survive on. For example, if Mr. Smith plans to retire at age 65 and believes he needs to have enough in his retirement fund to survive for 20 years, he would need to have a minimum of $300,000 in a retirement fund to cover just his basic needs (based on his current living conditions: $1250/month for necessities x 12 months/year x 20 years in retirement = $300,000).

Obviously, the earlier you start saving for your retirement, the better off you will be. If Mr. Smith doesn’t start saving for his retirement until later in life, then his contributions to that retirement fund will need to be much more substantial.

Are you eligible for free money?

That’s right—free money! If you have the option of participating in an employer-sponsored 401(k) plan, then you most likely are eligible for some extra free cash to be put towards your retirement needs. Most employers who offer a 401(k) plan for their employees to participate in have an employer match that goes along with it. This is usually a percentage of whatever you contribute.

The amount the employer may contribute varies from company to company. Some employers will match the first 6% of the employee’s salary that they contribute dollar for dollar. Others will contribute a percentage (commonly 50%) of whatever the employee contributes from their pay. Another great point about 401(k) plans is that they are usually pre-tax.

So let’s go back to our example before where Mr. John Smith has a take-home pay of $2500/month. Let’s say his gross pay (before taxes) is $3000/month. If he contributed 6% to a company matched 401(k) plan, that would be $180/month he would be contributing. If the company matched his 6% dollar for dollar, that would be an extra $180/month that would be added to his retirement fund.

That would make a total of $360.00 extra dollars a month going toward Mr. Smith’s retirement fund. This is more than double what he would be putting aside if he used the 50-30-20 budget, and it is pre-tax dollars which lowers his overall tax liability.

How much debt you have

Another important factor to consider when trying to figure out how much you should contribute to your retirement is how much debt you have now. The more debt you currently have to pay off, the less money that is available to put aside for later in life.

This kind of debt includes credit cards, loans, and other amounts owed that take away from your monthly income. If you have a high amount of this sort of debt, depending on how much time you have before you want to retire, it may be a better idea to focus on paying this debt off quicker before dedicating too much of your income towards saving for later. The quicker you pay off this type of debt, the sooner you will really be able to start making some generous contributions to your retirement fund.

Other retirement resources

Some of us are fortunate enough to have other resources to rely on when it comes to planning for our retirement years. Some employees may have a pension fund that is funded based on their length of employment with an employer. These pension funds can often be substantial enough to sustain a retired employee well into their golden years.

Other sources of potential funding for retirement may include inheritance money, selling property that is not used or turning it into an income property (by renting or leasing it), or other long-term savings options like annuities, mutual funds or similar investments.

Retirement calculators

If all these calculations are too much for you to grasp, let me ease your mind by telling you that there is an easier way. Retirement calculators are relatively easy to use, available online, and allow you to play with some different numbers until you feel you have found a goal that can be realistically accomplished.

With a retirement calculator, you will be able to forecast your approximate retirement age, how much you will need to save each month/year, or how long you will be able to enjoy life without work. Simply input a few simple figures and it will do all the math for you.

The Social Security Administration also has a calculator that you can use online to determine what your approximate benefit amount will be from Social Security once you retire. This income is important to include in planning for your overall retirement needs.

Bottom Line: Save as much as you can

So how much should we put aside from our monthly pay to save for our retirement? The simple answer to that complex question is: as much as you can. It never hurts to put more money aside for your retirement today as opposed to the alternative of spending now and struggling later. If your goal is to be a millionaire when you retire, then you will have to focus even harder on building that savings and investing your funds wisely to get you to that point.

Since every individual’s financial situation and needs are unique, there is no magic number that everyone should be saving towards their retirement. Determining how much money you will need during retirement, contributing to an employer-sponsored 401(k) plan, or finding alternative methods to save for your future are all critical parts of making sure you have what you need for comfortable living during the later years of life. Using a retirement calculator tool can also help make these calculations easier to understand.

The earlier you start saving, the better off you will be. Also, the more you are able to put aside toward your retirement, the more financially stable and comfortable you will be during your later years. After all, enjoying the golden years of retirement is what we work so hard all of our lives for, isn’t it? Why not be fully prepared for whatever that time might bring.

JL

Jennifer Leonhardi was born and raised on Catalina Island, giving her a unique small town perspective and focus on community. With a degree in Sociology, she now primarily enjoys writing, largely based on her own experiences, on topics such as financial assistance programs, issues concerning the home and family, and socioeconomic trends.

Share this post: