The Ultimate Money Checklist For 2024: 10 Things You’ve Got To Do Now!

JB

Last updated 03/20/2024 by

Julie Bawden-DavisWith 2014 screeching to an end, it’s time to do a last minute assessment of your tax situation. Once the New Year arrives, opportunities to take advantage of tax breaks for this year disappear. Before you break out the bubbly and sing “Auld Lang Syne,” ensure you save as much as possible on this year’s taxes by tending to these financial tasks.

Compare Home Insurance Providers

Compare multiple vetted providers. Discover your best option.

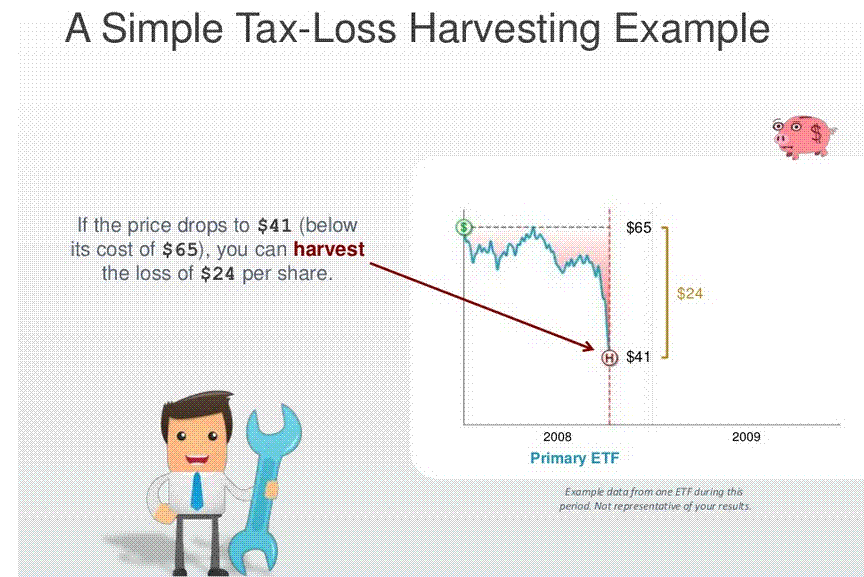

1. Consider Loss Harvesting

With the S&P 500 index rising almost 10 percent, it’s been a good year for stocks. Not every stock did well, though, which means you might have some losses. Offset your gains by selling losing investments before the end of the year. If you own mutual funds, bonds or stock trading below what you paid for them, you can sell them and use those losses to offset any taxable gains for the year. The gains can be offset with the losses dollar for dollar.

If your losses are more than your gains, you can also use up to $3,000 of that loss to offset other income. Even better, any remaining losses not offset can be carried over to the following year.

2. Defer Income

Since income is taxed in the year it’s received, it might be beneficial tax-wise to push upcoming payments into 2015. If possible, defer any year-end bonuses, or if you work for yourself, any payments, until the beginning of next year. You will want to defer income only if you think you’ll be in the same tax bracket or a lower one next year. If you think you’ll be making more money next year, you’ll want the income in 2014, or else you’ll end up paying more taxes in 2015.

Since income is taxed in the year it’s received, it might be beneficial tax-wise to push upcoming payments into 2015. If possible, defer any year-end bonuses, or if you work for yourself, any payments, until the beginning of next year. You will want to defer income only if you think you’ll be in the same tax bracket or a lower one next year. If you think you’ll be making more money next year, you’ll want the income in 2014, or else you’ll end up paying more taxes in 2015.3. Convert Your IRA To A Roth

If the idea of tax-free IRA withdrawals at retirement is appealing, consider converting your traditional IRA to a Roth. You’ll pay federal income taxes this year on the amount you’re converting, but from there on out you won’t pay any taxes on the money. Withdrawals of contributions from your Roth are tax and penalty-free once you’ve had the account open for five years, and you can take out investment earnings without paying tax on them once you are 59 ½.

If the idea of tax-free IRA withdrawals at retirement is appealing, consider converting your traditional IRA to a Roth. You’ll pay federal income taxes this year on the amount you’re converting, but from there on out you won’t pay any taxes on the money. Withdrawals of contributions from your Roth are tax and penalty-free once you’ve had the account open for five years, and you can take out investment earnings without paying tax on them once you are 59 ½.4. Contribute To Your 401(k)

If you haven’t maxed out your 401(k) for 2014 yet, you still have time to make a contribution. It’s possible to contribute up to $17,500 for the year or $23,000, if you’re 50 or older. Generally, the money you contribute to a 401(k) will lower your tax bill for the year, and you won’t be taxed until you withdraw the money at retirement.

If you haven’t maxed out your 401(k) for 2014 yet, you still have time to make a contribution. It’s possible to contribute up to $17,500 for the year or $23,000, if you’re 50 or older. Generally, the money you contribute to a 401(k) will lower your tax bill for the year, and you won’t be taxed until you withdraw the money at retirement.5. Check Your Flex Plan Balance

FSA plans offer a great way to save pre-tax money for medical expenses, but you can end up losing money if you don’t use the money in your account by year’s end. Your employer may allow you to carry over $500 to the following year until March 15, but your company may not be set up to allow such a grace period. Avoid losing the money in the account by using it on items like prescription medications, bandages, contact lenses, or go see your doctor, chiropractor or acupuncturist by December 31. For a full list of allowable expenses, consult IRS Form 502.

FSA plans offer a great way to save pre-tax money for medical expenses, but you can end up losing money if you don’t use the money in your account by year’s end. Your employer may allow you to carry over $500 to the following year until March 15, but your company may not be set up to allow such a grace period. Avoid losing the money in the account by using it on items like prescription medications, bandages, contact lenses, or go see your doctor, chiropractor or acupuncturist by December 31. For a full list of allowable expenses, consult IRS Form 502.6. Give To Charity

‘Tis the season to be generous and doing so can save you on your taxes. If you clean out your closets and give belongings to charity, in order for the gifts to be tax deductible, they must be itemized. If you make a cash contribution of more than $250 to a charity, in addition to your check stubs, you’ll need a letter of receipt from the organization. Also consider giving larger gifts to charity in order to get a bigger tax deduction. Such items can include vehicles and stocks or mutual funds.

‘Tis the season to be generous and doing so can save you on your taxes. If you clean out your closets and give belongings to charity, in order for the gifts to be tax deductible, they must be itemized. If you make a cash contribution of more than $250 to a charity, in addition to your check stubs, you’ll need a letter of receipt from the organization. Also consider giving larger gifts to charity in order to get a bigger tax deduction. Such items can include vehicles and stocks or mutual funds.7. Take Advantage Of Annual Gift Allowances

If you wish to give monetary gifts to beneficiaries and want to enjoy the tax benefits of doing so, now is the time to write those checks. For 2014, give up to $14,000 to each beneficiary or $28,000 combined with your spouse. You can give as many gifts as you want, and you don’t have to file a gift-tax return.

If you wish to give monetary gifts to beneficiaries and want to enjoy the tax benefits of doing so, now is the time to write those checks. For 2014, give up to $14,000 to each beneficiary or $28,000 combined with your spouse. You can give as many gifts as you want, and you don’t have to file a gift-tax return.8. Pay January’s Mortgage Early

Take advantage of this month’s mortgage payment interest by making January’s payment prior to December 31. Just make sure that the mortgage company records the payment as December and not January. In order to take advantage of the extra interest deduction, it must be on your 2014 1098 form.

Take advantage of this month’s mortgage payment interest by making January’s payment prior to December 31. Just make sure that the mortgage company records the payment as December and not January. In order to take advantage of the extra interest deduction, it must be on your 2014 1098 form.9. Plan To Write Off Your Home Office

If you work from a home office and you use it to meet with clients, or if the office is a separate structure from your home, you can write off the space on your taxes. It used to be that the home office deduction was controversial, but a new safe harbor deduction by the IRS allows you to deduct $5 per square foot of home office space, amounting to up to $1,500 each year.

If you work from a home office and you use it to meet with clients, or if the office is a separate structure from your home, you can write off the space on your taxes. It used to be that the home office deduction was controversial, but a new safe harbor deduction by the IRS allows you to deduct $5 per square foot of home office space, amounting to up to $1,500 each year.10. Pay Spring College Costs Now

Paying spring college tuition fees now may save you a substantial amount of money on this year’s taxes. You can claim the American Opportunity Tax Credit on your 2014 return. Eligible expenses for undergraduate studies under this tax credit include tuition, fees and books and other course materials for the first four years of study. The tax credit, which reduces your income tax, amounts to up to $2,500 for qualified expenses by an eligible student. Forty percent of the credit may be refundable, which means that you could even get a refund.

Paying spring college tuition fees now may save you a substantial amount of money on this year’s taxes. You can claim the American Opportunity Tax Credit on your 2014 return. Eligible expenses for undergraduate studies under this tax credit include tuition, fees and books and other course materials for the first four years of study. The tax credit, which reduces your income tax, amounts to up to $2,500 for qualified expenses by an eligible student. Forty percent of the credit may be refundable, which means that you could even get a refund.Of course, this time of year is hectic, but taking the time to make even a few of these financial adjustments now can mean a much brighter tax season come April.

JB

Julie Bawden-Davis is a widely published journalist specializing in personal finance and small business. She has written 10 books and more than 2,500 articles for a wide variety of national and international publications, including Parade.com, where she has a weekly column. In addition to contributing to SuperMoney, her work has appeared in publications such as American Express OPEN Forum, The Hartford and Forbes.

Share this post: