What Are The Most Popular Types of Credit?

JW

Last updated 03/19/2024 by

Jessica WalrackThe world of credit can be a confusing place as there are many types of credit. From credit scores to interest to various kinds of lenders, you may be wondering “Where do I start?” There are a lot of products to choose from and many times the terms and conditions are complicated, but once you find the right solution, developing good credit can help you achieve your goals.

Three of the most popular credit options available are credit cards, personal loans and home equity loans. Each is unique and they work very differently from each other. Depending on your situation, one probably will be best suited to your needs.

But, how do you know which one?

We will look at each option and explain how it works, the pros and cons, the recommended uses and three lenders we recommend. By the end, you will have the information you need to make an informed decision on the best financing option for your situation.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Credit cards

Let’s start by looking at one of the most common forms of credit available – the credit card.

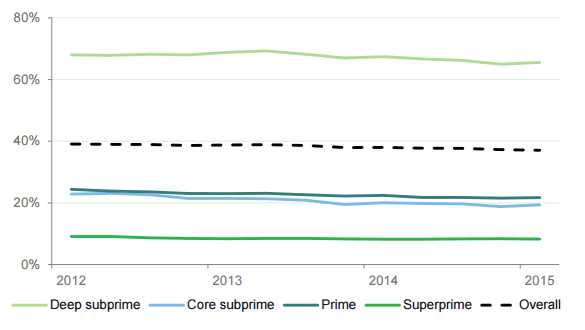

Credit cards extend you a line of credit that you can use to make purchases, pull out cash advances and transfer balances. The credit line you are granted will depend on your credit score. In the graph below from the Consumer Financial Protection Bureau’s Consumer Credit Card Market Report, see the average credit line given on new general purpose accounts.

If you pay the amount back in full by the due date on the balance, no interest is charged. However, if you only pay your minimum monthly payment, the balance will be carried over and interest will be applied to it.

The amount of interest you pay will depend on the annual percentage rate offered by the credit card lender, which typically ranges from 10% to 25%.

How do you get the best rate? Your credit history and credit score will play a role. The better your credit, the better rate you will get. Some credit cards will have an interest-free or reduced-interest introductory period that can be up to 24 months. In this case, no extra is charged as long as the credit amount is paid off within the allotted time. Aside from the interest, credit cards also carry extra costs, such as annual, late payment, balance transfer and cash advance fees.

Another aspect of credit cards that’s important to know about is the rewards perk. Select cards specialize in certain areas to give you incentives for spending on specific things. For example, travel cards let you earn airline miles as you spend, as well as other perks such as free access to private lounges in airports, rental car insurance and refunds if you cancel your trip. Another popular rewards card type is the cash-back card on which you earn back in cash a percentage of which you spend, typically 1% to 5%.

Credit cards also can help you build your credit. Your lenders report on the status of your accounts to the main credit bureaus every month. If you show responsible use of credit, such as making your payments on time and not maxing out your card, you will earn higher credit scores.

Recommended uses

Now that you know a little more about credit cards, when is the best time for you to use one? With credit lines ranging from $500 to $10,000, cards can be used to pay for things you don’t have the money for upfront, for example, a new refrigerator or dishwasher. Instead of getting another type of loan, you can use a credit card and pay for it over time.

Credit cards also are good for people looking to build their credit. As I mentioned, your account will be reported to the three credit bureaus monthly, so you can get a card just for the purpose of showing you can responsibly use it. Do this effectively by paying off your balance on time and in full each month. If you do carry a balance over, ensure it is under 30% of your entire credit limit.

Depending on your spending habits, credit cards with rewards can also be good to use for your regular spending so you can get more for your money. If you travel a lot, using a travel-focused credit card will provide you with benefits. If you spend regularly at grocery stores or gas stations, find a cash-back card that offers you rewards for those categories.

Top picks

Here are our top picks for credit cards:

Personal loans

With a personal loan, you are given a loan from a lender that is not secured against any asset you have. It is granted based on your creditworthiness. If approved, the amount will be given along with a set of terms for repayment. In most cases, personal loans will be for periods of five years and less, have an origination fee, have interest applied and require monthly payments.

Your credit score will help determine the interest rate applied to your loan. The better your credit and higher your score, the less risk you are to the lender, and so the interest rate will be lower. If your score is too low, the loan will not be approved.

Most personal loans have fixed interest rates, which means that for the duration of the loan, the rate will not change and your monthly payments will remain the same. Others may have variable rates, so when the prime interest rate increases or decreases, so will your monthly payments.

The advantages of a fixed rate are you will always know what you need to pay, while the disadvantage is that if the prime interest rate falls, your rate stays the same. The advantage of a variable interest rate is more cash in your pocket when prime lending rates fall, while the disadvantage comes if rates increase and you have to pay more on your installment each month.

Recommended uses

Personal loans are recommended to cover large costs that are hard to pay out of pockets, such as medical bills, home improvements, energy efficiency upgrades, and educational costs. These are all necessities or investments that will provide returns in the long run. Another popular reason to get a personal loan is to consolidate debt. In doing so, you can potentially get control over a growing debt and reduce the interest and fees you are paying. Personal loans are not typically recommended for unecessary expenses such as vacations, weddings or consumer purchases. These are quickly consumed but would be paid for over years with no return on investment.

Home equity loans

If you own property, a home equity loan allows you to borrow against the equity you have gained in your home. So if you owe $100,000 and your home is now worth $250,000, you can borrow against that $150,000. These function as a second mortgage of sorts.

You can receive a lump sum as a home equity loan or if you don’t need the money up front, you can set up a home equity line of credit (HELOC) that allows you to spend as you need to. These are secured loans, as your house is the collateral, making them less risky for lenders but more risky for borrowers.

Recommended uses

Home equity loans are recommended for home renovations, paying for your children’s education, consolidating higher interest debt, or perhaps even paying for the purchase of another property. Think along the lines of how the money can be used to invest in something that will provide long-term benefits. You don’t want to use it frivolously, as you may find yourself with high monthly payment and nothing to show for it. You may also lose your house if you default on the loan.

Top picks

Here are leading lenders to consider.

CapWest Mortgage Lenders

As one of the U.S.’ largest retail mortgage lenders, CapWest provides a range of mortgage options. It has an A+ rating with the Better Business Bureau and offers competitive rates.

USAA

USAA is a lender that specializes in serving members of the armed forces and their families. It also has an A+ rating with the Better Business Bureau and is known for its flexible eligibility criteria and low-interest rates.

Which credit type is best for you?

Credit cards are great for building your credit and financing relatively small purchases. Personal loans are recommended for more expensive, necessary costs such as medical emergencies or investments in your home, family or vehicles. A home equity loan should be used for larger investments, such as the purchase of a second property, home renovations or your children’s education.

FAQ on Types of Credit

What credit score do you need to get a home equity loan?

To qualify for a home equity loan, here are some minimum requirements: Your credit score is 620 or higher — 700 and above will most likely qualify. You have a maximum loan-to-value ratio, or LTV, of 80 percent — or 20 percent equity in your home. You have a documented ability to repay your loan.

What is a home equity loan and how does it work?

A home equity loan is basically a second mortgage, in which you take out the total amount you intend to borrow in one lump sum and pay it back every month. The time period is typically 5-15 years. A home equity line of credit, or HELOC, gives you the ability to borrow up to a certain amount over a 10-year period.

Which credit type is best for you?

Credit cards are great for building your credit and financing relatively small purchases. Personal loans are recommended for more expensive, necessary costs such as medical emergencies or investments in your home, family or vehicles. A home equity loan should be used for larger investments, such as the purchase of a second property, home renovations or your children’s education.

What are the types of personal loans?

Common types of personal loans include unsecured, fixed- and variable-rate, and debt consolidation loans. The best choice depends on your own circumstances. Most personal loans are unsecured with fixed payments. But there are other types of personal loans, including secured and variable-rate loans.

Do personal loans hurt credit?

A personal loan can consolidate credit card debt and improve your credit score for several reasons: A personal loan is an installment loan so debt on that loan won’t hurt your credit score as much as debt on a credit card that’s almost to its limit, thereby making available credit more accessible.

Once you know the best option for you, it’s time to find the lender that will suit your needs. If you want to review more options, visit our pages dedicated to personal credit cards, personal loans and home equity loans. When you do, you can easily compare lenders as well as read reviews about the various products they offer.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: