3 Reasons Why You Should Make a Down Payment on Your VA Loan

BL

Last updated 03/15/2024 by

Ben LuthiFor veterans and active-duty military, the VA loan program offers much-needed assistance in buying a home.

The biggest advantage of a VA Loan is that there is no down payment required”

“The biggest advantage of a VA Loan is that there is no down payment required,” says John Cooney, veteran and owner of Green and Gold Financial Planning.

That’s because the Department of Veteran Affairs insures VA loans, limiting the risk to lenders. In contrast, conventional mortgage lenders that allow 0% down payments are few and far between.

But just because you don’t have to put any money down doesn’t mean you shouldn’t. Here are three reasons why you should consider making a down payment on your VA loan.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

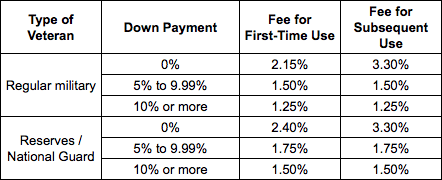

1. Your funding fee will go down

One of the drawbacks of VA loans is the VA funding fee. This upfront fee can range between 1.25% and 3.3% of the loan.

“The funding fee is essentially how the government insures itself against a veteran defaulting on a loan,” says Cooney. Here’s how it breaks down:

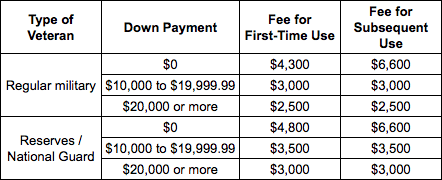

To show how much you could save in real dollars, let’s say that you’re buying a house worth $200,000. If you’re regular military, this is your first VA loan, and you put down nothing, the VA funding fee will be $4,300.

If, however, you put down 5%, or $10,000, your VA funding fee drops to $3,000. Put down 10%, and the fee goes down to $2,500, saving you $1,800.

Here’s how it breaks down for all scenarios:

2. You’ll save money over the long run

With a down payment, you instantly decrease the amount you owe to the lender.

Not only could this help you qualify for a lower interest rate, but it will also lower your monthly payment and, thus, your overall interest costs.

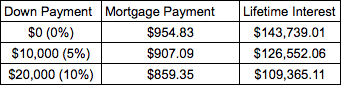

With a $200,000 purchase price and a 4.00% interest rate on a 30-year loan, here’s how the math works based on a 0%, 5%, and 10% down payment:

As you can see, putting down 10% would save you roughly $95 a month and $34,374 over the life of your loan. If you’ve got the cash now, you’ll easily make up for it in savings.

3. You’ll immediately have equity in your home

Before the U.S. housing market crashed in 2006 and 2007, many lenders were making it easy for just about anyone to get a mortgage loan. A lot of these people put little or no money down on their houses.

The problem? As soon as the market crashed, they were “underwater” on their loan, meaning the home’s value was less than the loan amount.

So, if they wanted to sell the house, they wouldn’t get enough from the sale to pay off their mortgage. As such, there was a wave of foreclosures when people could no longer make their payments because they simply didn’t have any other option.

If you put down a 5% down payment on a $200,000 loan, you’ll have $20,000 equity in the home right out the gate. If your home’s value drops a bit, you might still have equity.

Also, you’ll have access to home equity loans and home equity lines of credit, in case you want to use one to finance a home renovation or something else.

Do what’s best for you right now

There are a lot of benefits of putting a down payment on your VA loan. But if you’re struggling to come up with the money, the good news is that you won’t get turned away.

When it comes to a VA loan down payment, there’s no right answer. You simply need to consider the trade-offs and decide which path is better for you.

Doing an analytical approach can help you make the decision. But you also have to consider external factors.

For example, a $20,000 down payment in the above example would save you $36,174 total. But what if you’re not planning on staying in the house for very long? And what if you need that cash for another short-term goal?

The best way to decide how much you should put down on your VA loan, if at all, is to research all the options and do the math. Use a down payment calculator to see how much you’d need to reach the breakpoints on the VA funding fee.

Also, compare several mortgage lenders to see how a down payment can affect your interest rate.

If you choose to make a down payment, Cooney recommends to “identify an amount you would like to save and make monthly savings towards this goal a line item in your budget, just like you would a utility bill or rent payment.” This can help you avoid the temptation to spend that money and get you to your goal faster.

BL

Ben Luthi is a personal finance writer and a credit cards expert who loves helping consumers and business owners make better financial decisions. His work has been featured in Time, MarketWatch, Yahoo! Finance, U.S. News & World Report, CNBC, Success Magazine, USA Today, The Huffington Post and many more.

Share this post: