What is a Credit Card CVV? And 9 Other Credit Card Questions You’re Too Embarrassed to Ask

BL

Last updated 03/15/2024 by

Ben LuthiUnless you work in the credit card industry, chances are you don’t know a lot about the plastic you carry around every day in your wallet. But understanding how credit cards work can help you better manage your spending, protect your sensitive information, and take advantage of credit card perks.

To help you get started on the right foot, here are answers to the top 10 credit card questions you’re too embarrassed to ask.

Compare Credit Cards

Compare the rates, fees, and rewards of leading credit cards.

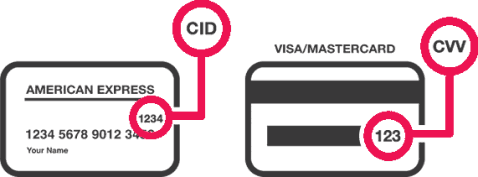

1. What is a credit card CVV?

One way that credit card issuers protect your card’s security is through the CVV code.

“These three- and four-digit codes provide extra security when authenticating transactions when the credit card isn’t present, such as phone or internet purchases,” says Jason Steele, a credit card expert and journalist.

There are actually two different CVV codes:

- CVV1: This code is embedded into the card’s magnetic stripe.

- CVV2: This code is printed on the card, and you’ll typically get asked for it when paying for something over the phone or online.

Since the CVV2 code is printed on the card, an identity thief can’t make those kinds of purchases if they just steal the information from your magnetic strip.

American Express cards also have a 4-digit security code on the front of the card.

2. How does my credit card know which rewards to give me?

If you have a rewards credit card that offers bonus categories, you may be wondering how the credit card issuer knows when you’ve made bonus purchases.

This is done through merchant category codes (MCCs). Each merchant has an MCC based on their primary business when their code is established.

MCCs are then grouped into different categories, such as groceries, travel, or gas. So, when you use your credit at a Kroger, HEB, or Trader Joes, your card issuer knows that you made a purchase at a grocery store. It then posts your rewards accordingly.

3. How many credit cards should you have?

There’s no right answer to this question. Rather, it’s based on your ability to manage your credit.

“I think that it’s important to have at least two or three credit cards to build your credit history and take advantage of the benefits offered by different cards,” says Steele.

“However, you should never have more than you can responsibly manage. Those who can’t pay their bills on-time and control their debt should use other forms of payment.”

Yes, that means that, for some people, having no credit cards at all is the best choice.

4. Do I need to carry a balance to build credit?

The answer to this question is a resounding no. Your payment history, which is the most important factor in your FICO and VantageScore credit scores, is based on whether or not you make your monthly payments on time.

The credit bureaus don’t register how much you paid and whether it was a full or partial payment. As a result, the only one who benefits from you carrying a balance each month is the credit card issuer.

Do yourself a favor and pay your balance on time and in full each month.

5. How does a secured credit card work?

“A secured card works much like any other credit card, except you must submit a refundable security deposit before your account can be opened,” says Steele. “But after your account is open, your card will work just like any other credit card.”

With most secured cards, your credit limit is equal to your initial security deposit and you can usually add more deposits to increase your limit.

The credit card issuer uses the security deposit as collateral in case you default on your payments, and you’ll typically get it back when you close the account in good standing.

6. How do I close my credit card?

It depends on the issuer, but you can usually cancel your credit card simply by calling the number on the back of the card.

You may want to do this if you’ve just paid it off and don’t want the temptation, or the card charges an annual fee and it’s not worth keeping.

Keep in mind, however, that there are some situations when canceling a credit card is a bad idea. Make sure you understand the negative impact of canceling your card so you don’t hurt your credit.

7. How do cash advances work?

Most credit cards allow you to convert some of your available credit to cash through an ATM or at a bank teller counter. For the most part, however, this is a bad idea.

“Most cash advances incur a higher interest rate and have no grace period, so you can’t avoid interest by paying your statement balance in full,” says Steele. Also, you can be charged a cash advance fee, which may be $10 or 5%, whichever is higher.

Consider other options for quick cash before you opt for a cash advance.

8. How do I avoid overspending with my credit card?

Popular personal finance gurus like Dave Ramsey recommend avoiding credit cards at all costs. But for most people, credit cards aren’t the problem; lack of spending discipline is.

If you want to avoid overspending with your credit card, it’s important to create and maintain a monthly budget. Set spending goals and keep track of your spending so you don’t exceed them.

As you do this, you’ll have a much better chance of avoiding credit card debt now and in the future.

9. Can you use a credit card to buy a money order?

“You can only purchase a money order with cash, and sometimes with a debit or prepaid card,” says Steele.

In some situations, you may be able to buy a Visa or Mastercard gift card with your credit card, then use that gift card to buy a money order. But doing so is against your credit card agreement, so it’s not advisable.

10. What’s with the chip on my credit card?

The magnetic strip on the back of your credit card contains static information about your credit card. As a result, it’s vulnerable to fraudsters.

The chip on the front of your card, which is called an EMV chip, helps secure your card information. Its data is dynamic in that, every time you use the card, it gives a unique token to process the payment.

If an identity thief stole that token information, it would no longer work because it’s for one use only. Of course, it’s not foolproof, but it can help protect you from becoming a victim of fraud.

FAQ on Credit Card

What is the CVV in credit card?

The CVV Number (“Card Verification Value”) on your credit card or debit card is a 3 digit number on VISA®, MasterCard® and Discover® branded credit and debit cards. On your American Express® branded credit or debit card it is a 4 digit numeric code.

Do all credit cards have CVV?

All credit cards have CVV numbers, below the black magnetic strip on the credit card. This CVV number acts as a unique security code. It’s a common understanding that we shouldn’t share our debit and most important credit card details with anyone.

Can I borrow money from my credit card?

A cash advance is a short-term loan from your credit card issuer. You can access the advance from an ATM or the bank. In most cases, the credit card company won’t let you borrow money in the full amount of your credit line—rather, they’ll cap your withdrawal at a portion of your credit limit.

Can I transfer money from credit card to bank account?

Money transfer credit cards enables, pay into your bank account from credit card. Once the money is in money transfer credit card, it can be withdrawn or used via debit card. Some banks charge 0% interest rates on the transferred cash for an agreed period.

Do cash advances on credit cards hurt your credit?

While simply taking out a cash advance and paying it back promptly will not affect credit, neglecting to pay back the loan will. Cash advance payments are meant to bridge the gap between bill due dates and your next pay check. So long as the loan is paid back promptly, a cash advance does not hurt your credit score.

Conclusion

The more you know about your credit card, the better. That’s why we’ve created an easier and quicker way to find the right information so that you can be confident you’re making the right decision.

If you’re considering getting a new credit card, take a look at SuperMoney’s credit card review page to see which cards are best for your needs. You’ll be able to read reviews and quickly compare rates side-by-side.

The more time you spend understanding each available option, the easier it will be to get the most out of your card.

Related reading: On the subject of credit card security, you may wonder if a PIN could offer an added layer of protection alongside the CVV. Read Do Credit Cards Have PINs? to find out.

BL

Ben Luthi is a personal finance writer and a credit cards expert who loves helping consumers and business owners make better financial decisions. His work has been featured in Time, MarketWatch, Yahoo! Finance, U.S. News & World Report, CNBC, Success Magazine, USA Today, The Huffington Post and many more.

Share this post: