15-Year Fixed Mortgage: Pros and Cons

MG

Last updated 03/21/2024 by

Marcie GeffnerA 15-year fixed mortgage can be an attractive choice for home buyers and homeowners who want to refinance their current home loan. However, it’s not always a smart or even viable option. Here are the pros and cons you should consider before applying for a mortgage refinance.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

15-Year mortgage: pros and cons

On the pro side, this mortgage offers a shorter term compared with a 30-year mortgage, and it comes with an interest rate that’s fixed for the entire term of the loan.

The chief advantage of a 15-year fixed mortgage is that the rate should be slightly lower than the rate for a 30-year fixed mortgage, if everything else—loan amount, loan type, down payment percentage, and so on—is the same.

The lower rate can mean big savings.

Also on the pro side, the 15-year loan has a set schedule of monthly payments to pay off the loan in half the time compared with a 30-year mortgage.

This faster pace can help you stay on track to own your home free and clear sooner. It can also help you build equity, which you can borrow against in a cash-out refinancing.

On the con side, the 15-year loan has a higher monthly payment than a 30-year loan because the term is shorter.

Pros and Cons of a 15-Year Mortgage

15-year vs. 30-year mortgage

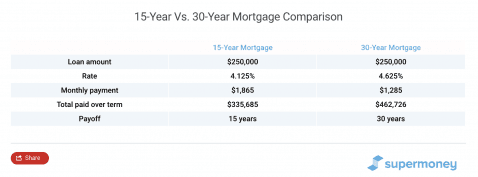

Suppose you borrowed $250,000 with a 30-year term and a fixed rate of 4.625%. Your monthly principal and interest (P&I) payment would be $1,285, and you’d pay a total of $462,726 over the entire term of that loan.

Now suppose you borrowed $250,000 with a 15-year term and a fixed rate of 4.125%. Your monthly P&I would be $1,865, and you’d pay a total of $335,685 over the entire term of that loan.

Compared with the 30-year loan, you’d save $127,041. That’s a lot of money.

Comparison of $250,000 Mortgage With 30-Year Term or 15-Year Term

Bigger rate discount

The differential between the 15-year and 30-year rates is an important factor to consider. In the above example, the differential is 4.625% minus 4.125% or 0.5%.

If the differential is relatively small, the 15-year term is less attractive. If it is relatively wide, the shorter term is more attractive.

The differential fluctuates over time due to mortgage market conditions.

Can you afford a 15-year mortgage?

Whether the rate differential is smaller or larger, your payment will be higher. And whether you feel comfortable with that higher payment depends on your personal financial situation and tolerance for risk.

Ask yourself if you can manage the higher payment, if you feel secure in your financial situation, and if that payment fits into your budget and financial plans for the future.

Advice for borrowers

If you’re buying your first home and have a long time horizon, a 30-year mortgage can boost your buying power. You’ll be able to borrow more because your payment will be more affordable relative to your income.

If you’re refinancing, a 15-year loan might help you become mortgage-free before you retire from the workforce.

If you like the accelerated payoff of the 15-year mortgage, but you’re not comfortable with the higher payment, get a 30-year mortgage and make higher payments or extra payments along the way.

Making higher or extra payments helps you pay off your mortgage sooner.

Should you get a 15-year mortgage?

Given these pros and cons, is a 15-mortgage a good idea?

The answer is up to you, with the advice of your mortgage lender, says Bill Packer, executive vice president of American Financial Resources, a mortgage lending company in Parsippany, N.J.

“The decision requires an understanding of the consumer’s goals,” Packer says. “The right (mortgage advisor) can fully assess the borrower’s needs, and financial situation to best guide them toward the right length of the loan.”

To find your best option, start by reviewing a wide list of top lenders and comparing their terms side-by-side on SuperMoney’s mortgage refinance page.

MG

Marcie Geffner is an award-winning freelance reporter, editor, writer and book critic. Her work has been featured online and in print by The Washington Post, Los Angeles Times, Chicago Sun-Times, Urban Land, Business Start-Ups and Fox Business Network Online, among many other newspapers, magazines, and websites. With a bachelor’s degree in English from UCLA and MBA from Pepperdine University in Malibu, Geffner has impressive credentials in both story-telling and business management. A second-generation native of Los Angeles, Geffner now lives in Ventura, California, a surf city northwest of her hometown.

Share this post: