First-Time Home Buyer Guide

AL

Last updated 03/14/2024 by

Andrew LathamFact checked by

Embarking on the journey to buy your first home can be a daunting experience if you’re not well-versed in the mortgage industry. The process is often intricate, and complex, and can be frustrating for those unfamiliar with its ins and outs. Considering that it will take decades to pay off the loan, the stakes are undeniably high.

Navigating the mortgage process and borrowing criteria can be challenging, as they differ significantly between lenders. But negotiating with lenders is only the tip of the iceberg – you’ll also have to engage with sellers, real estate agents, title companies, and more.

Fear not, our comprehensive guide is here to assist you in understanding the essentials of the home-buying process, from shopping around to finally closing the deal. With this first-time homebuyer’s guide, you’ll be well-equipped to make informed decisions and successfully secure your dream home.

Compare Home Equity Lines of Credit

Compare rates from multiple HELOC lenders. Discover your lowest eligible rate.

How to buy a home in 10 steps

Before delving into the various mortgage options available for buying a house, let’s quickly summarize the key steps involved in the home-buying process:

- Assess your financial situation: Determine your budget and evaluate your credit score, which will affect your mortgage eligibility and interest rates.

- Get pre-approved for a mortgage: Approach lenders to obtain a pre-approval, which gives you an estimate of how much you can borrow and demonstrates your credibility to sellers.

- Find a reliable real estate agent: A knowledgeable agent can guide you through the process, help you find suitable properties, and negotiate on your behalf.

- House hunting: Browse listings and attend open houses to find a property that meets your requirements and budget.

- Make an offer: Submit a written offer to the seller, detailing your proposed price and any contingencies, such as financing or a home inspection.

- Home inspection: Hire a professional home inspector to assess the property’s condition and identify potential issues or repairs needed.

- Finalize mortgage details: Once your offer is accepted, work with your lender to finalize the mortgage terms and lock in an interest rate.

- Appraisal: Your lender will arrange an appraisal to determine the property’s market value and ensure it aligns with the agreed-upon price.

- Secure homeowners insurance: Obtain a suitable insurance policy to protect your investment.

- Closing: Attend the closing meeting to sign the required paperwork, pay the down payment and closing costs, and officially become a homeowner.

Now that you have a general understanding of the home-buying process, let’s explore the various mortgage options available to help you finance your dream home.

Types of mortgage loans

There are several different types of mortgage loans. Which type is best for you depends on your personal and financial circumstances. Here’s a quick summary of your options.

Conventional loan

A conventional loan is a traditional mortgage loan that isn’t backed or insured by a government agency. You’ll typically need a credit score of 620 or higher to qualify for a conventional loan. And you’ll have to make a 20% or higher down payment if you don’t want to have to pay for private mortgage insurance (more on that later).

FHA loan

FHA loans are mortgage loans insured by the Federal Housing Administration. If your credit score is 580 or higher, you can secure your home with a down payment as little as 3.5%. If your score is between 500 and 579, you can still get approved, but with a down payment of 10%.

Instead of charging private mortgage insurance, FHA loans charge mortgage insurance premiums, which can be more expensive than private mortgage insurance over time.

VA loans

VA loans are designed for eligible members of the military community and their families. They’re insured by the U.S. Department of Veterans Affairs. While the VA doesn’t have any credit score requirements, most VA lenders typically require a credit score of 620.

VA loans don’t require a down payment. However, they do charge a VA funding fee of up to 3.3%. That fee will depend on your eligibility status, your down payment, and how many VA loans you’ve had.

USDA loans

Insured by the U.S. Department of Agriculture, these loans incentivize people to buy homes in eligible rural areas. USDA lenders typically require a credit score of 580 or higher, but they will make exceptions.

Like VA loans, USDA loans require no down payment, though they do charge an upfront and annual guarantee fee. However, these fees are lower than those of VA and FHA loans, and cost less than private mortgage insurance (PMI).

Which type is best?

When shopping around for a mortgage, compare at least three or four mortgage lenders to see what rates and other terms they offer. Don’t be afraid to compare even more than that to make sure you’re getting the best deal.

Mortgage closing costs

One of the more frustrating aspects of the home-buying process is the process of closing. Why? Because closing on your mortgage isn’t just complicated, it’s also costly. Depending on your circumstances, closing costs can range from 2% to 5% of your total loan amount.

As a result, it’s critical to keep these in mind when saving up for your house. If you only save for a down payment, closing costs may overwhelm your budget. In some cases, the seller will cover the closing costs, but this only works if they are desperate to get rid of the property.

You can also ask your lender to cover closing costs in exchange for a slightly higher interest rate. However, this strategy is somewhat short-sighted. You’ll likely pay more in interest over time than you would have if you’d simply paid your closing costs up front.

Types of closing costs

There are many types of closing costs you might run into. Here’s what you should expect:

- Application fee: Covers the cost of the loan underwriting process.

- Appraisal fee: Paid to the appraisal company to determine the fair market value of the home.

- Attorney fee: Pays an an attorney to review the final loan documents. Not required in all states.

- Courier fee: Covers the cost of expediting documents to ensure you close on time.

- Credit report fee: Pays to pull your credit report during the underwriting process.

- Discount points: Allows you to lower your interest rate with a lump-sum payment.

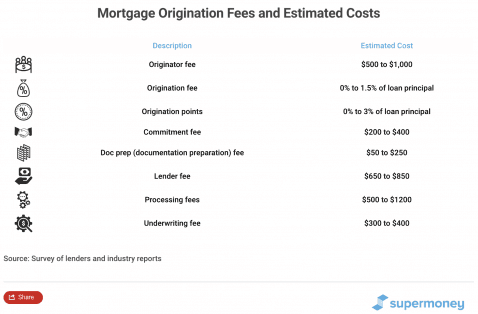

- Document preparation fee: Pays for the time spent preparing your loan documents.

- Escrow fee: Paid to the company responsible for closing your loan, typically a title or escrow company.

- Escrow deposit: A lump-sum payment to cover a couple of months’ worth of property tax and mortgage insurance.

- Flood determination fee: Covers the cost of a third party determining if your house is located in a flood zone.

- Home inspection fee: Paid to verify the condition of the property and determine if repairs are necessary.

- Homeowners association (HOA) dues: If applicable, may include an investment fee to join, plus some prepaid dues.

- Homeowners insurance: Typically paid annually and due at closing.

- Origination fee: Includes administration and processing fees.

- Prepaid interest: Includes interest that will accrue between closing and your first payment.

- Recording fee: Paid to the city or county office responsible for recording public land records.

- Survey fee: Paid to a surveying company to verify property lines.

- Title insurance: Paid to protect the lender if there’s an issue with the title.

- Title search fee: Paid to the title company for doing a property records search.

- Transfer taxes: Paid to transfer the title.

Other mortgage loan costs

Depending on the type of loan you have, there may be other fees and costs. Here’s a breakdown of the fees you can expect for each type of loan.

Conventional mortgage

- Cost: Private mortgage insurance (PMI).

- Amount: 1% – 5% of the loan amount annually.

- How to avoid it: Put down at least 20%.

FHA loan

- Cost: Mortgage insurance premium (MIP).

- Amount: 75% upfront; 0.45% to 1.05% annually.

- How to avoid it: MIP cancels after 11 years if you put down at least 10%. If your down payment is less than 10%, these charges continue indefinitely.

VA loan

- Cost: Funding fee.

- Amount: 25% to 3.3% of the loan amount.

- How to avoid it: All VA loans charge a funding fee, but you can get a lower fee by putting down a larger down payment.

USDA loan

- Cost: Guarantee fee.

- Amount: 1% upfront, 0.35% annually.

- How to avoid it: It’s unavoidable. All USDA loans charge an upfront and ongoing guarantee fee.

How much house can you afford?

Before you start house hunting, it’s important to set a budget. It’s important to avoid being “house poor” — having such high monthly payments that you can barely afford your household budget.

To determine how much house you can afford, focus on the monthly payment rather than the total home price. Your monthly payment will be made up of the following elements:

- Principal and interest: This is the basic payment to satisfy the loan.

- Mortgage insurance: Depending on your loan type and down payment amount, you may not need mortgage insurance. Read on to learn more about mortgage insurance and how much it can cost.

- Property taxes: Your county assessor’s office will determine the percentage you’ll pay in property taxes. Take that percentage and divide it by 12 to get the monthly amount.

- Homeowners insurance: You’ll need it to finance a home, and it’s a smart way to be ready for potential crises.

- Homeowners Association (HOA) fees: If applicable.

Depending on your budget and goals, you can generally choose a 15-, 20-, or 30-year mortgage. The shorter the repayment period, the higher your monthly payment. But the longer you take to pay off your loan, the more money you’ll end up paying in interest overall.

“I try to encourage first-time homebuyers to consider a 30-year mortgage,” says Michael Dinich, a financial advisor, “because payments will be much lower. It seems like no matter how much you research or plan ahead, something unexpected will pop up.”

Having a lower monthly payment can give you the flexibility to pay more if you can afford it. You can also save extra cash on the side for any big repairs and maintenance costs. As you tally up these costs, it’s important to know whether you can afford your dream home.

Here are some rules of thumb to help you design the perfect mortgage for your circumstances.

Mortgage rules of thumb

28% rule

According to this rule, your total housing expenses (including mortgage insurance and property taxes) should be no less than 28% of your gross monthly income. So, if you earn $4,000 per month before taxes, the maximum you should pay each month is $1,120.

36% rule

If you’ve accrued other debts in addition to your mortgage, consider the 36% rule. According to this rule, your total debt payments should be no less than 36% of your monthly income. That includes your student loans, auto loans, credit cards, etc., as well as your mortgage payments. This is a helpful limitation to consider if you’re balancing multiple monthly payments.

If your gross monthly income is $4,000, that means your total monthly debt obligations should be no more than $1,440.

And be wary about juggling too many debts. Lenders may refuse to offer you a loan if your debt-to-income ratio is as high as 43%.

Calculating the home value

Once you know how much you can afford to pay each month, you can use market interest rates to approximate how much you can spend on a home.

For example, let’s say your total monthly mortgage payment caps out at $1,120, and the market rate is around 4.5%. If you get a 30-year mortgage, you can expect to qualify for a mortgage worth roughly $221,000.

If you have $20,000 saved for a down payment, that means you can get a home worth closer to $241,000. Just remember to keep closing costs in mind as you do these calculations.

How to find the right real estate agent

Without specific expertise, it can be hard to discern a good deal from a scam. An experienced real estate agent can be your secret weapon, helping you to understand benefits and detriments that you might otherwise overlook.

A real estate agent can also help you find a home that suits your preferences, and negotiate with sellers to score better rates. They can be your personal advocate to guide you through the mortgage process.

This is the person you’ll lean on the most throughout the home-buying process. Real estate agents can be expensive, but if you’re new to the home-buying process, their expertise can save you a lot more than they cost.

Tips for finding the right realtor

If you want to get the right real estate agent for your needs, use some or all of these tips:

Ask around

Do you have friends in the area who have bought a home recently? Ask them for recommendations! Make sure that they can vouch for the realtor’s skill, and not just their character.

Interview them

This may take some time, but it’s important to make sure that a realtor can meet your needs. They may have been great for your friend, but people have different expectations for professional relationships. You’ll have to meet them to ensure that you’re professionally compatible.

“A good real estate agent should understand the type of home you’re looking for and your budget,” says Dinich. “If you find that the agent is only interested in showing you their listings or listings outside of your price range, consider a different agent.”

Do some research

The internet makes this part of the process easy. Take some time to research the agent. Visit LinkedIn, realtor websites, and review pages to see how much experience the agent has, whether they have any special certifications, and how they treat their clients.

If you can’t find any information, it’s likely that they’re new to this. Since this is your first time, focus on finding someone who has been in the game for a long time.

How to choose the right home

Once you know your budget and you’ve secured a good real estate agent, you’re ready to find your home. This stage can be the most challenging, as your emotions about the homes you see can cloud your judgment.

As you visit different houses, you may fall in love with one of them. Resist the urge to allow your emotions to guide such a long-term financial decision.

Instead, start by setting firm size and feature requirements with your agent. Do you want two or three bedrooms? How big should the home be? Does the pantry need to be large? Do you need a mudroom? A wheelchair-accessible bedroom? How big should the backyard be?

Establish a list of what you need in a home and what you want. Keep that information in mind as you look at different homes within your price range. Don’t fall for the temptation of checking out houses above your budget, “just for fun.” Letting yourself fall for a home you can’t afford is a bad idea.

If you love a home that doesn’t include all of your needs, ask yourself whether you’ll be happy with the home in five years.

Also, be sure to get pre-approved for a mortgage loan before you start house hunting. If you want to make an offer, the seller will want to know if you’re likely to go through with the deal. Pre-approval can show them that you can afford the home.

Getting started

Now that you have a good understanding of the basics of the home-buying and mortgage process, take the time to determine whether you’re financially ready for a home. If you are, establish a budget, and then look for a real estate agent.

And before you start looking at houses and applying for a mortgage, don’t forget to check out other home buyer tips. Compare mortgage rates from several lenders to make sure you get the best deal. You can also consider working with a mortgage broker to improve your chances of getting a good rate.

“Working with a broker can make sense if anything is out of the ordinary with your situation,” says Dinich. “Brokers tend to know which lenders are more likely to be agreeable to your unique situation, and may end up saving you money.”

Ready to get started? Click here to compare top mortgage lenders side-by-side.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: