What is a Perfect Credit Score? 5 Must-Follow Tips to Get a High Score

BL

Last updated 03/15/2024 by

Ben LuthiYour credit score is a three-digit snapshot of your credit history and provides lenders with an idea of how trustworthy you are as a borrower. The better your credit score, the easier it is to get approved for loans and credit cards and score low interest rates along the way. But what is a perfect credit score?

Achieving a perfect credit score isn’t easy. According to reports from FICO, only 1.4% of the population has a perfect credit score. But is it worth it? Or do you just get bragging rights? Here’s what you need to know.

Compare Credit Report Services

Compare multiple vetted providers. Discover your best option.

What is the perfect credit score?

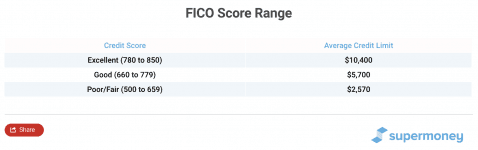

The basic FICO scoring model has a range of 300 to 850, so an 850 credit score means that your credit is in perfect shape. Here’s a full range of the FICO credit score:

Here’s what you’d need to do to achieve a perfect credit score of 850:

- Have no negative items on your credit report at all.

- A zero balance on most of your credit cards and ultra-low balances on the others.

- Have a credit history for around 30 years or longer.

In other words, you can have a healthy relationship with credit, but the key is that your length of credit history must be substantial.

Does a perfect credit score matter?

In a word, no. A perfect credit score gives you bragging rights, but it won’t necessarily get you a lower interest rate than, say, a score of 780, and here’s why.

The FICO credit scoring model and other scoring models are designed to help lenders determine if a borrower is risky or not. Someone who has made payments late or carries a high credit card balance is generally seen as riskier than someone who has never paid late and keeps their credit card balances low.

To achieve a very good credit score, you need to be extremely responsible with your credit. So, to lenders, someone who meets that criteria is generally responsible enough that they’d qualify for the best terms the lender has to offer.

“I would focus on establishing the habits that will lead to a better credit score rather than just chasing a number,” says Steven Millstein, a certified credit counselor at Credit Zeal.

“I believe that anyone can reach an 850 credit score in the long run, provided they focus on forming the habits that will lead to great credit.”

5 tips for getting a high credit score

If you want perfect credit, we’ll be the first to cheer you on. But if you’re fine with achieving good enough credit, the tips are all the same. Here’s what you need to do.

1. Always pay on time

Your payment history makes up 35% of your FICO score, so it’s critical that you avoid missing payments.

One way to do this is to set up all of your loan and credit card payments on autopay. Then, be sure to keep enough cash in your checking account, so the payment doesn’t get returned.

Remember, late payments don’t show up on your credit report until 30 days after they’re late. So, if you do make a mistake, fix it quickly. And don’t beat yourself up over past mistakes.

“You might not be able to change the past, but you can impact what goes on your credit report from this point forward,” says Millstein.

2. Keep your credit card balances low

How much you owe is the second-most important factor in your credit score, making up 30% of the calculation. The biggest aspect of this factor is your credit utilization, which is your balance divided by your credit limit.

The goal is to keep your credit utilization as close to zero as possible, at least on the day the card issuer reports the balance. To do this, call the issuer and ask when it reports your balance to the credit bureaus.

Then, remember to make a payment each month before that date to make sure the reported balance is low. Alternatively, you could make multiple payments throughout the month to keep the balance low.

3. Be patient and keep old accounts open

Your length of credit history makes up 15% of your credit score and includes both how long you’ve had credit in general and your average age of accounts. As a result, there are two recommendations for this one.

The first is to simply be patient. The average person with an 850 score has roughly 30 years of credit history, so it can take time to prove your track record.

Second, keep old credit card accounts open to boost your average age of accounts. If you’re afraid of them getting closed due to inactivity, set up a small recurring charge, such as your Netflix or Spotify subscription, and put the account on autopay.

4. Add more credit diversity

Your credit mix accounts for 10% of your credit score because lenders like to see that you can responsibly manage different types of debt. So, look to get a good mix of credit, including credit cards, auto loans, mortgage loans, and more.

“This is particularly true if you have a short credit history because there is less information used to calculate your score,” says Millstein.

Of course, avoid taking out debt just for the sake of improving your score. The interest likely won’t be worth it. But at the same time, don’t shy away from debt if you need it.

5. Apply for credit only when necessary

Every time you apply for a loan or credit card, it can knock a few points off of your credit score. What’s more, these hard inquiries stay on your credit report for two years.

“If you actually open the account, your overall account age will drop dramatically,” says Millstein. So, it’s important to avoid applying for credit unless you absolutely need to.

Your next steps

Achieving a perfect credit score of 850 takes a lot of time and effort, but all that work might not be necessary. Instead, focus on establishing good credit habits and practice them over a long period. Get on a good payment plan and get out of debt if you can.

As you do so, your credit will get to the point where you’ll qualify for the best terms lenders have to offer, even if you don’t have a perfect credit score.

As you work toward achieving your goal, be sure to check your credit score often. And if you need a credit card, personal loan, or another type of loan, do your research to make sure you get the best one for your needs.

BL

Ben Luthi is a personal finance writer and a credit cards expert who loves helping consumers and business owners make better financial decisions. His work has been featured in Time, MarketWatch, Yahoo! Finance, U.S. News & World Report, CNBC, Success Magazine, USA Today, The Huffington Post and many more.

Share this post: