Annuity Payments Vs. Lump-Sum Payments: Pros and Cons of Each Payment Method

JW

Last updated 03/20/2024 by

Jessica WalrackWhen you have a large sum of money at your disposal, whether it’s a pension, settlement, or something else, you often have the choice of taking all the money at once or choosing annuity payments instead.

We’ve all heard the stories of people hitting the lottery and quickly squandering their winnings when they could have been set for life. On the other hand, a large amount of cash provides access to additional investment opportunities. So when is a lump sum the right choice, and when should you opt for annuity payments? Here’s what you should know to make the right decision for your situation.

Compare Life Insurance Providers

Compare multiple vetted providers. Discover your best option.

What is an annuity?

To understand annuity payments, think of life insurance in reverse. You invest a large sum of money upfront and receive regular disbursements for the rest of your life. Many institutions offer annuities, including banks, insurance companies, independent brokers, and other financial groups. However, they are insurance products, and only insurance companies issue them.

When do you need an annuity?

The goal of an annuity is to protect people from outliving their income. It guarantees income for the rest of your life or a specific term. This insurance product often comes in handy for people nearing retirement who want to ensure their pensions or savings last. Additionally, annuities may be useful when a large sum of money is obtained from another source, such as from a lawsuit settlement, winning the lottery, or an inheritance.

Lump-sum vs. annuity payments

When you are faced with the choice to take a lump sum or monthly annuity payments, what should you consider?

Lump-sum payment

The main advantage of a lump sum payment is you have full control over the money and how it is used. You can spend it and invest it how you want. The downside is, you may overspend or take losses on investments that leave yourself short on cash later in life.

Annuity payments

The main advantage of annuity payments is the certainty they offer. You know how much you will receive each month and can count on it. The main drawback is the lack of flexibility. If you need more money for an emergency, you won’t be able to get it out of your annuity plan. Additionally, if you pass away sooner than expected, you’ll receive less than if you had taken the lump sum.

The right choice for you will depend on your unique financial situation. Are you in need of a guaranteed monthly income to cover your essential living expenses? Then go with the annuity payments. Do social security and other income cover your basic expenses? Are you confident in your ability to earn bigger returns by taking the money and making investments? Then, the lump sum would probably be more advantageous. The best solution may even be a combination of both if the annuity company allows it.

Which method of payment is most common: annuity payments vs lump-sum?

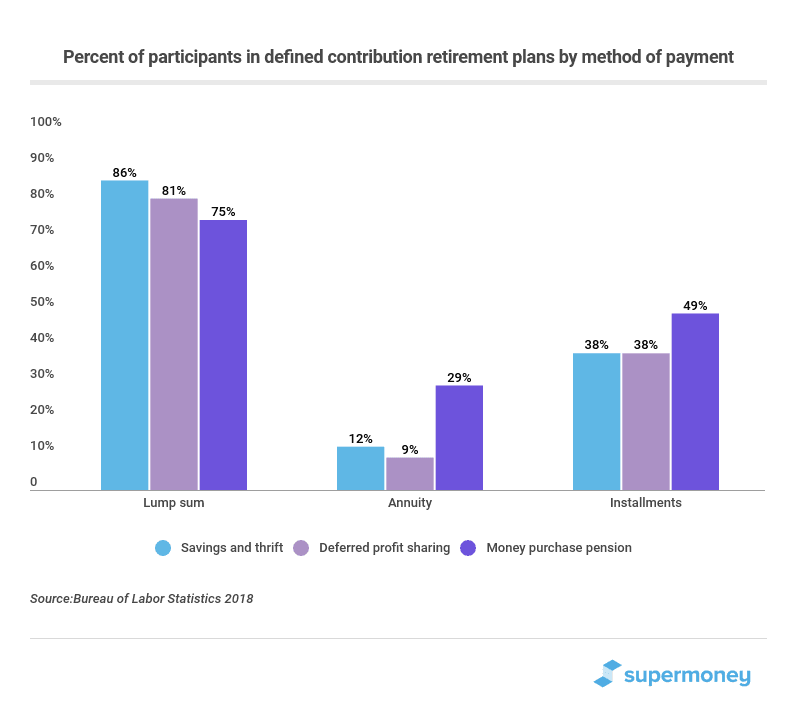

According to the latest data by the Bureau of Labor Statistics, among private industry workers in defined contribution plans, most participated in savings and thrift plans (73%) (source). Other common plan types include deferred profit sharing (25%) and money purchase pensions (18%). A lump sum was the most common payment option available to workers in these plans.

A lump sum provides retiring workers the full amount of their retirement savings and earnings with no further benefits received from the plan. Annuity payments were available to 29% of participants in money purchase pension plans. That was more than the share of workers who could receive an annuity in savings and thrift plans (12%) or in deferred profit-sharing plans (9%). Annuity payments provide a periodic (usually monthly) payment for the life of the retiree. With installment payments, the retiree receives part of the account balance in regular payments until the balance reaches zero. If the account balance is greater than zero when the retiree dies, the retiree’s beneficiaries receive the balance. Installment payments may occur monthly, quarterly, or yearly for 5 to 20 years.

What are savings and thrift plans?

Savings and thrift plans work much the same way as 401(k) plans. You can choose to divert part of your salary into the plan. Your employer deducts the money directly from your paycheck and is not taxable. The money grows tax-deferred until it’s withdrawn.

What is a deferred profit-sharing account?

Deferred profit-sharing programs are a type of pension fund. Periodically, the employer shares the company’s profits with a designated group of employees through the DPSP. These contributions and the interest they accrue are not taxed until the money is withdrawn.

What is a money purchase pension?

Money purchase pensions are a type of defined contribution retirement plan offered by some employers. They are similar to 401(k) and 403(b) plans, in that both the employer and employee make contributions to the plan. The main difference is the employer is required to make fixed contributions. In other words, employers must contribute a fixed percentage of each eligible employee’s salary annually to their retirement accounts.

What types of annuity payments exist?

When looking at annuities, there are many variations to consider, which can factor into whether they are a better solution than a lump sum.

Immediate vs. deferred annuity

An immediate annuity is an annuity that begins disbursing payments right away while a deferred annuity begins disbursements at a date in the future.

Term vs. life annuities

A term certain annuity will guarantee a set monthly income for the recipient that lasts for many years. Usually, it will pay a scheduled amount until the individual is 90 years of age. If all the payments have not been paid out before death, the remaining payments or lump sum will be made to the estate.

A life annuity is set up to pay a specific amount every month, quarter, or year until the recipient dies. At that time, no further payments will be made to the estate. However, there are other options you can add to a life annuity policy to make that happen.

As an example, an annuity can be set up to make payments to your living spouse upon your death. Additionally, you can purchase an annuity that will automatically increase the amount of income you receive based on current inflation rates. Typically, an extra option that is purchased toward the policy tends to lower the monthly payment.

Fixed vs. variable vs. indexed annuities

You also have several options when it comes to an annuity’s payout potential and level of risk. You can choose from the following varieties:

- Fixed annuities: With fixed annuities, the payouts are guaranteed based on the account balance. They offer low risk with modest returns and high predictability.

- Variable annuities: With variable annuities, the funds are invested in a selection of mutual funds, and payouts depend on the performance of investments. While you stand to gain higher returns, you also face more risk.

- Indexed annuities: With indexed annuities, a portion of your disbursements are tied to the performance of a market index, but you also get a guaranteed minimum payment. As a result, you take moderate risks and gain a moderate potential reward.

The type of annuity you need will depend on your life expectancy, income needs, risk tolerance, and preferences.

Should you sell an annuity?

What if you have an annuity but want access to the money? When your personal or financial needs dictate a change, it might make more sense to convert the annuity into a large lump sum of cash. Then, you can diversify investments give to family, or use the money to achieve other goals. Some people choose to convert their annuity into a lump sum of cash to pay down medical debt, take a vacation, or build an addition on their home.

However, it’s essential to look into any surrender fees or penalties you may face for withdrawing the funds from the annuity early. Further, be sure to consider if sacrificing the security of scheduled payments will be beneficial in the short and long-term.

If you would like to learn more about annuities, lump-sum payments, and other wealth management topics, reach out to a trained professional. They can help you understand all of the possible options and which will be the best for you. Compare leading firms below.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: