Asset Seizure – How Does It Work?

AL

Last updated 03/19/2024 by

Andrew LathamFact checked by

If you owe back taxes and don’t arrange to pay, the IRS has the power to take your property as payment through a process called asset seizure.

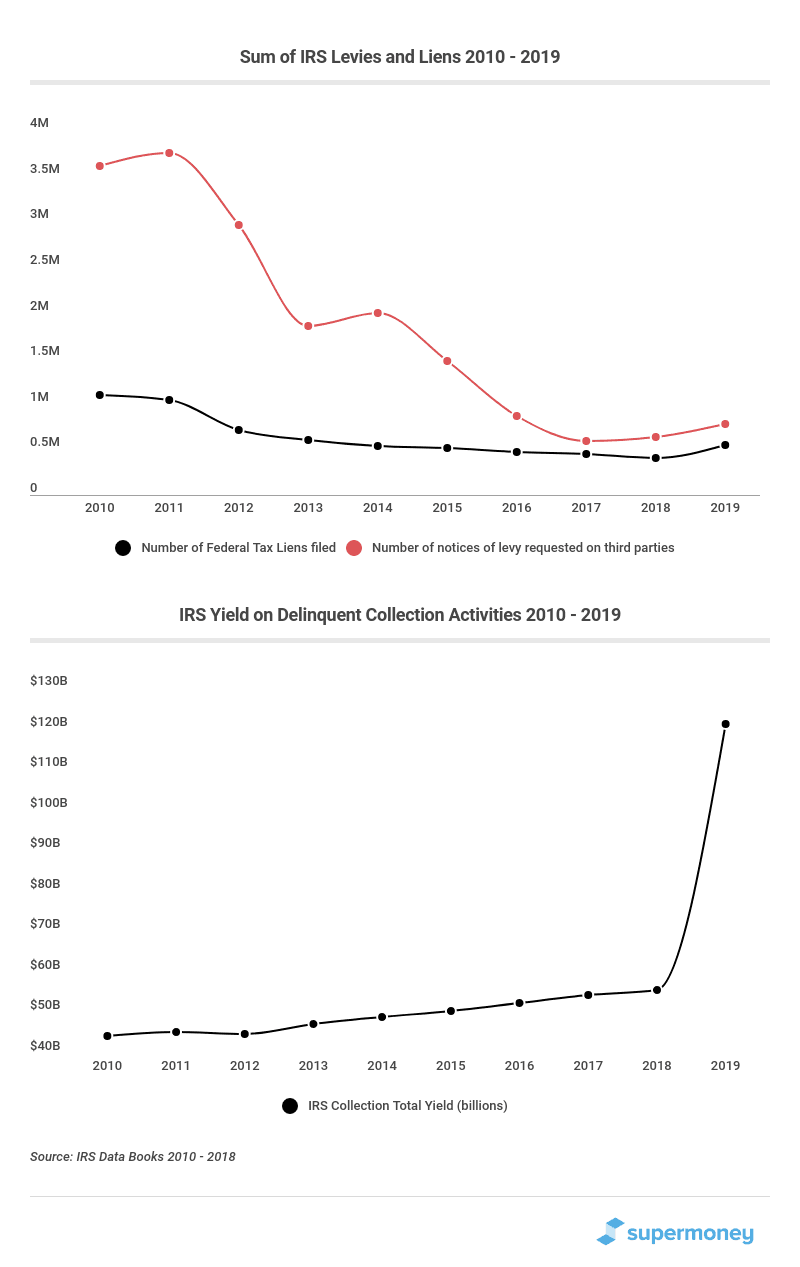

Tax levies are by far the most common method of asset seizure. In this case, the IRS takes your wages or the money in your bank account to pay your back taxes. In 2019, the IRS issued 782,735 levies to third parties like employers and banks. It’s rare for the IRS to seize your personal and business assets like homes, cars, and equipment. The IRS seized those kinds of properties only 228 times in 2019.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How does IRS asset seizure work

Whenever you owe taxes to the U.S. Treasury and don’t pay, a claim against you by the federal government arises by law. (Internal Revenue Code § 6321.) This claim is called a tax lien.

The tax lien automatically attaches to just about everything you own or have a right to. If you owe interest and penalties on the tax, which is often the case, the lien covers these amounts as well.

This guide will answer your questions about asset seizures and how you can protect yourself, your family, and your business, specifically answering the questions:

- When would the IRS seize your assets?

- Can you go to jail for unpaid taxes?

- How long does it take the IRS to seize?

- What can the IRS seize?

- What can the IRS not seize?

- How can you get your seized property back?

- After the IRS sells your seized assets, what do they do with the funds?

- How to prevent asset seizure?

When would the IRS seize your assets?

Believe it or not, the IRS does not want to seize your assets. The IRS’s preferred course of action is for you to pay your taxes when they are due. If you’re unable to do so, your best option is to file your tax paperwork and request a payment plan to repay your debt in installments.

Even if you fail to file your taxes, the IRS will take steps to secure the money without asset seizure. They will send notices informing you about your unpaid debt. If there is no response, the IRS will attach a tax lien to your real estate or other assets. A lien signifies that you owe the IRS money, and you need to pay it if you sell the attached property.

At this stage, if you pay your debt (or set up a payment plan), you can avoid asset seizure. However, if you fail to file your taxes and refuse to respond to a written communication from the IRS, the situation will escalate.

Finally, the IRS will levy your assets. A tax levy is a notification that your assets are subject to asset seizure. In other words, the IRS will take your assets of value, sell them, and use the proceeds to cover your debt.

Since 2011, the IRS has drastically reduced the number of tax liens and levies it places on taxpayers. Instead, it uses other tax relief tools to encourage taxpayers. The graphs below seem to indicate this tactic has been successful.

Can you go to jail for unpaid taxes?

Generations ago, it was possible to go to debtor’s prison if you owed money and could not pay it back. Fortunately, the United States banned this process in 1833. If you owe money to the IRS and cannot pay, you will not go to jail for it.

However, it is against the law to lie to the IRS, file falsified tax returns, or hide assets, known as tax evasion. Popular figures like actor Wesley Snipes, rapper Ja Rule, and professional baseball player Darryl Strawberry have gone to jail for failing to disclose income and filing false tax returns.

How long does it take the IRS to seize?

The IRS will not perform an asset seizure without providing notice. The IRS wants to get paid for the taxes owed — they don’t want your items. To legally seize your assets, the IRS must go through a three-step process, with some exceptions. These steps are designed to ensure that the IRS adequately notifies you and follows the law before issuing a levy:

- The IRS sends a Notice of Demand for Payment. In other words, the IRS sends you a tax bill.

- You ignore, neglect, or fail to make payment arrangements while the IRS waits for a response.

- The IRS issues the Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

The final notice is delivered to the taxpayer personally, left at the taxpayer’s last known address, or sent by registered or certified mail. At this point, you have 30 days to appeal or make payment arrangements. If you fail to make arrangements, the IRS can start taking your assets after 30 days.

What can the IRS seize?

Can the IRS seize my personal property?

The IRS can seize your personal property and real estate, even if it is not in your physical possession. For example, if you have a boat stored at a friend’s house, the IRS can take that.

The IRS can also take wages, payments from your clients, rent from your tenants, money in your bank account, and retirement funds. The IRS contacts whoever is holding your money and gets them to send it directly to the IRS.

Can the IRS seize my home?

The Internal Revenue Service cannot seize your primary residence without a judge’s approval. However, they can place a lien on the property to ensure that you pay your taxes when you sell the property.

Do you have to let the IRS into your home?

IRS agents can’t enter your home without your permission or a legal document authorizing them to. However, if you refuse to allow an IRS agent to enter your home, they will come back with a legal writ from a judge.

If the IRS agent has evidence that you are removing or hiding property to avoid seizure, they can enter without your permission; known as exigent circumstances. In exigent circumstances, authorities may enter your home to prevent physical harm, destruction of evidence, or hiding of assets. But the IRS agent must have actual evidence of this happening, not just a suspicion.

Can the IRS seize jointly owned property?

Yes, the IRS can seize jointly owned property. When the IRS seizes co-owned property, the co-owner may receive compensation.

Tenants-in-common each own a specific percentage of the property. The IRS must pay them as per that percentage when it sells the property.

Joint tenants are treated as if they each own the whole property. When the IRS seizes and sells an asset, joint tenants may not receive any money if the unpaid taxes are of higher value than the sale proceeds.

And if you added a co-owner to a property without receiving fair compensation, the IRS can invalidate their ownership interest.

Can the IRS seize inherited property?

Yes, the IRS can seize money or property you inherited to satisfy your tax debt. If the person passing on the inheritance is still alive, there are methods to protect it from the IRS. For example, it is sometimes possible to structure the inheritance as a trust instead of giving it directly to the taxpayer.

What can the IRS not seize?

When performing an asset seizure, the IRS can’t take everything you own. There are rules in place so that you are not left destitute and unable to feed your family. The IRS can seize a wide range of income, wages, and property. However, according to Internal Revenue Code 26 U.S. Code § 6334, the IRS may not seize the following:

- Clothing and school books that are deemed necessary.

- Personal effects, furniture, firearms, and livestock not exceeding $6,250 in total value.

- Books and tools of the trade necessary for your profession or business, under $3,125 in value.

- Unemployment benefits.

- Undelivered mail.

- Some annuity and pension payments.

- Worker’s Compensation.

- Judgments for support of minor children entered before the date of levy.

- Wages, salary, and other incomes over the minimum exempted.

- Certain service-connected disability payments.

- Certain public assistance payments.

- Assistance under the Job Training Partnership Act.

- Personal residences in small deficiency cases where the taxes owed are less than $5,000.

- Personal residences and certain business assets you use in your trade or business (unless a judge or magistrate changes that).

Note that the value for the items mentioned above is not based upon the retail value or the amount you originally paid for these items. The value is based on the fair market value that someone would pay for them today.

How can you get your seized property back?

Contact the IRS immediately to resolve your tax liability and request a seizure release. You can do this directly or through a tax professional. There are several ways to negotiate a settlement with the IRS that allows you to recover your property. A tax relief professional can walk you through your options and discuss the best option for you.

When must the IRS return seized assets?

The IRS will release your assets if:

- You paid the taxes owed.

- The collection statute of limitations expired before the IRS issued the levy.

- You convince the IRS that the assets will help you repay the taxes you owe.

- You have an installment agreement that specifically halts the levy.

- An economic hardship related to the asset seizure prevents you from affording basic living expenses.

- The asset’s value is greater than the balance owed, and releasing the levy will not hinder the IRS’s ability to get paid.

For example, let’s say you own multiple properties, and the levy is attached to all of them. The IRS may release the levy from one or more properties to let you sell or refinance it to settle your unpaid taxes.

Note that the release of a seizure does not mean you don’t have to pay the balance due. You must still arrange with the IRS to resolve your tax debt, or a seizure may be reissued.

Before selling your property, the IRS will calculate a minimum bid price. The IRS will also provide you with a copy of the calculation. When you receive this notice, you have an opportunity to challenge the Internal Revenue Service’s fair market value determination. The IRS will then provide you with the notice of sale and announce the pending sale to the public, usually through local newspapers or flyers posted in public places. After giving public notice, the IRS will generally wait at least 10 days before selling your property.

How to get professional help

During this process, you can plead your case and negotiate with the IRS to get your seized property back. A recent report by the Treasury Inspector General for Tax Administration (TIGTA) titled, Review of Compliance With Legal Guidelines When Conducting Seizures of Taxpayers’ Property, identified errors committed by the IRS conducting seizures. These are instances in which the IRS did not comply with a particular Internal Revenue Code section or an internal procedure resulting in violation of taxpayer rights and taxpayer burden. Errors identified related to the collections process, nonjudicial sale notices, and property valuations.

These findings underscore the need for competent legal counsel when facing a potential IRS levy or seizure. Often, a knowledgeable tax attorney can prevent an imminent IRS seizure and may be able to craft a long-term resolution to a tax problem that avoids a seizure altogether. When the IRS engages in an improper seizure, such as those at issue in the TIGTA report, the law provides the potential for recourse. You must contact the IRS immediately if you want your property back. Working with a tax attorney can raise your odds of success. Research this area and get as much knowledge as you can.

By making the case that the asset seizure caused immediate economic hardship, it is possible to get your items back. If the IRS denies your request, you can always appeal. You may appeal before or after the IRS seizes and sells. Again, having a competent tax attorney or accountant on your side can greatly increase your chance at a successful appeal.

After the IRS sells your seized assets, what do they do with the funds?

When the IRS performs an asset seizure, money from the sale pays for the cost of seizing and selling the property and, finally, your tax debt. If there’s money left over from the sale after paying off your tax debt, the IRS will tell you how to get a refund.

How to prevent asset seizure?

If you have already received the Final Notice of Intent to Levy and Notice of Your Right to a Hearing, take immediate action. At this stage, you can stop an IRS asset seizure in the following ways:

- Negotiate with the IRS and enter into an installment agreement to chip away at your debt in a series of monthly payments.

- See if you qualify for an IRS hardship program.

- Apply for an offer in compromise, wherein you agree to pay less than the total amount you owe. You can pay in a lump sum or installments. To qualify for this option, you must prove that paying the full amount would result in financial hardship.

- Convince the IRS that the targeted asset has little value.

- Provide evidence that the levy will directly create a financial hardship that will make it harder for you to pay your taxes.

- File bankruptcy to stop all creditor collection activity. The IRS cannot proceed with asset seizure without permission from the bankruptcy judge. Be wary of this option, as it will hurt your credit score for up to a decade.

In summary

The most effective way to stop an IRS asset seizure is to pay what you owe. However, if that is not an option, you can apply for multiple tax relief programs. A tax relief professional can provide guidance on which program is best for you. If you don’t have the savings to cover your tax debt and you don’t qualify for tax relief, there is the option of borrowing the money you need. If you own your own home, you can refinance your home or take out a home equity line of credit.

However, borrowing to pay the IRS is not always a smart move. Consult with a tax professional and find out which options are best suited for your circumstances.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: