What Is the Average Credit Score After a Chapter 13 Discharge?

CS

Summary:

Chapter 13 discharge is the final step of Chapter 13 bankruptcy and, on average, lowers your credit score by 150 to 200 points. It releases debtors of all payments and ensures that creditors cannot come to collect more payments from them. A Chapter 13 discharge lowers credit scores and stays on credit reports for seven years.

Many people who find themselves drowning in debt end up filing for bankruptcy. In some cases, they file for Chapter 13 bankruptcy, which helps them reconstruct their debt payments. At the end of your payments, you are “discharged,” meaning you no longer have to make payments.

So, what happens to your credit score at this point? Does it go back to where it was before? Will the bankruptcy filing still show up on your credit report? Keep reading to have these questions answered.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is Chapter 13 discharge?

Chapter 13 discharge is the final step of Chapter 13 bankruptcy (also referred to as wage earner’s plan). This article goes more in-depth on what Chapter 13 bankruptcy is, but we’ll give a brief rundown of it here.

Chapter 13 bankruptcy helps an individual with regular income develop a plan to repay all of their debts. It is usually a three-to-five-year payment plan.

Chapter 13 debt discharge is the final step in the Chapter 13 bankruptcy process and usually occurs six to eight weeks after your final payment is made. Chapter 13 debt discharge releases debtors of certain debts. This means creditors are not allowed to try to collect money from the debtor.

Pro Tip

You’ve probably heard of bankruptcy, but do you know what it means? Read SuperMoney’s ultimate guide to bankruptcy to understand bankruptcy and when it may be necessary.

Dischargeable debts

Not every debt is forgivable under Chapter 13 bankruptcy. Here are a few debts that can (and some that cannot) be forgiven:

| Dischargeable debts | Non-dischargeable debts |

|---|---|

| • Breach of contract debt | • Child and spousal support claims |

| • Credit card debt | • Criminal fines |

| • Debt from property damage, done willfully and maliciously | • Criminal restitution |

| • Debt from an unsuccessful bankruptcy case | • Drunk driving liabilities |

| • Debt incurred to pay non-dischargeable taxes | •Mortgage loans |

| • Government fines, forfeitures, and penalties | • Student loans |

| • Medical bills | |

| • Negligence-related debt | |

| • Uncollateralized personal loans |

Pro Tip

If you’re overwhelmed with student or mortgage loan debt, you’re not alone. Many are struggling with these types of debt. The good news is that you do have options.

There are various mortgage relief programs you can look into if you’re worried about your mortgage. Federal student loan consolidation is an option for those struggling with educational debt. If you’re looking for some general tips on how to get out of debt, SuperMoney has some tips for that, too.

Are you eligible for Chapter 13 discharge?

The Chapter 13 process is a long one, so before you start, be sure that you qualify. Note that only individuals (and not businesses) can apply for Chapter 13. Here’s a look at other eligibility requirements for Chapter 13:

- Combined secured and unsecured debts must be under $2,750,000.

- Not have a bankruptcy petition dismissed in the last 180 days due to failure to appear in court or comply with the court.

- Have no voluntarily dismissed bankruptcy filings in the last 180 days after your creditors pursued court relief to recover property they had a lien on.

- May not be a debtor under Chapter 13, within 180 days before filing, unless you receive credit counseling from an approved credit counseling agency.

What happens to my credit score after Chapter 13 discharge?

Alright, so we have a basic understanding of what Chapter 13 discharge is. Now it’s time to dive into how Chapter 13 affects your credit score.

First and foremost, it’s important to know that all major credit bureaus will note your bankruptcy filing on your credit report. During this time, your credit score will be lower. Low credit scores make it difficult to obtain new credit, and when you do, it usually comes with fees and high interest rates you wouldn’t otherwise have. Poor credit scores also make it difficult to purchase a house, property, and more.

The good news is that Chapter 13 will not be on your credit report forever. Chapter 13 bankruptcy is removed from your credit report after seven years. Once it is removed from your credit report, your credit scores will increase. From there, you can start to rebuild your credit.

What’s the average credit score after Chapter 13 discharge?

What your credit score drops to after filing bankruptcy depends on what it was before. Usually, the higher the credit score, the bigger the drop there is. On average, credit scores drop between 150 to 200 points. It’s fairly common for a credit score to be around 579 after filing for bankruptcy.

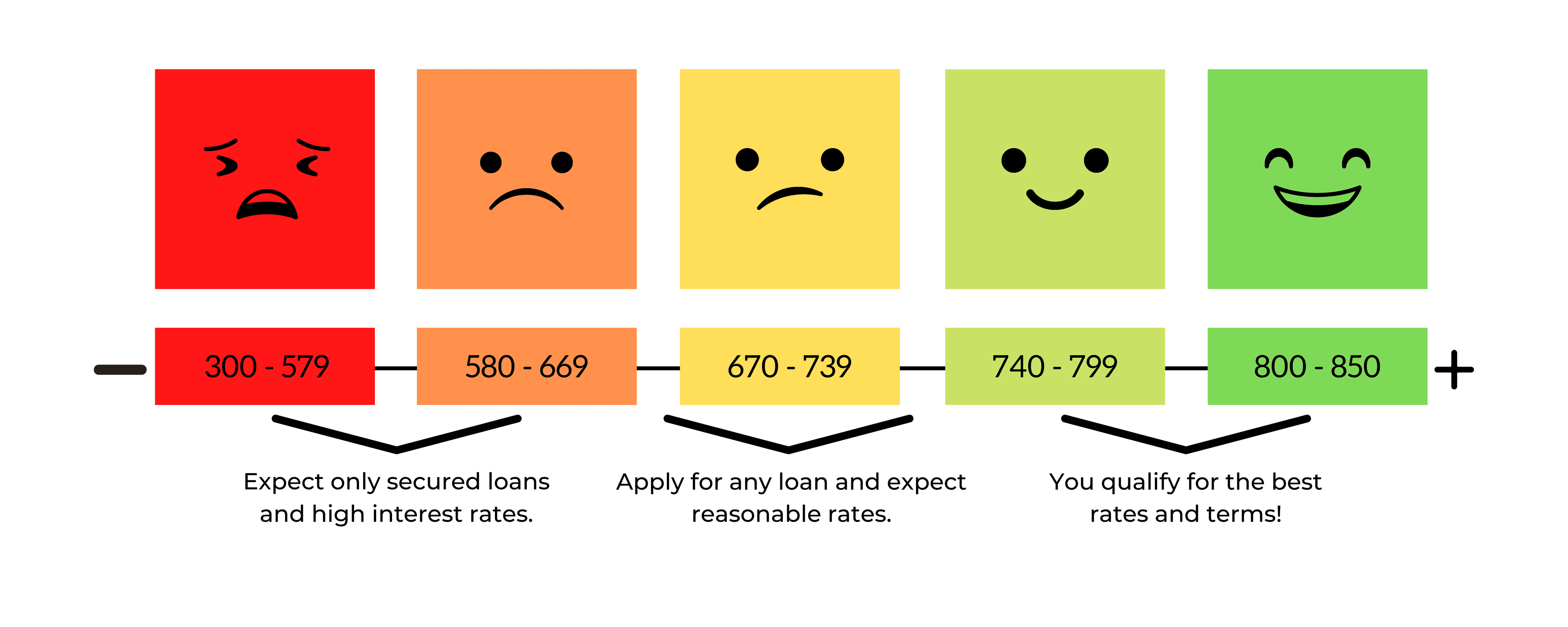

FICO scores are categorized based on the following ranges:

Unfortunately, it’s likely that you will have a fair or poor credit score when filing for bankruptcy and afterward. In the case of Chapter 13, however, bankruptcy will be removed from your credit history after seven years. This will help improve your credit score, but not by too much. It will still need some work.

How soon after bankruptcy will your credit score improve?

You can start the process of improving your credit score around 12 to 18 months after you file bankruptcy. You cannot remove bankruptcy from your credit report, and because many credit card companies require a good credit score to open new credit, your options are limited.

The best way to improve your credit score while bankrupt is to make timely monthly payments on your bills. This may seem small, but it makes a difference.

Ways to improve your credit score

Rebuilding and improving your credit score takes time, work, and self-discipline. But it’s definitely achievable and very important. Credit reports impact your ability to get loans, cars, property, and more. Be sure to start rebuilding your credit as soon as possible.

Here are some things you can do after bankruptcy to improve your credit score:

- Make on-time payments. This is one of the best and most consistent ways to improve your credit score. Late payments can hurt your credit, so keep on top of those due dates and make sure that you’re paying bills on time.

- Get a cosigner. A cosigner is someone who agrees to make payments if the primary borrower cannot. A cosigner is usually a family member or close friend. Having a cosigner can make it easier to get a credit card when you have poor credit.

- Become an authorized user. An authorized user is someone who has a credit card in their own name that is attached to someone else’s credit card account. You can make purchases using this account, but do not monitor the account itself. If you go this route, be sure that you work with someone you trust. If they fail to make payments on time, your credit score could be impacted.

- Check your credit report and credit score. Monitoring your credit report and credit score can help you keep track of your progress and see where you can improve.

- Reduce credit card use. You can avoid poor spending habits (and falling into bankruptcy again) by reducing how much you use your credit card. This can help you from getting into too much debt that you can’t pay off.

- Create new lines of credit. This is generally recommended to do once you can afford to pay off the balances each month.

- Get a secured credit card. Secured credit cards are opened when you make a small cash deposit. This could be a great way to build your credit and avoid falling into debt again.

FAQs

How long does it take to rebuild credit after Chapter 13?

There isn’t one exact timeline for rebuilding your credit. Depending on what your score was before, it could take months or years to rebuild your credit to your previous score. However, by making consistently timely payments, working with a cosigner, and being smart with your financial decisions, you can gradually rebuild your score.

How hard is it to get a loan after Chapter 13 discharge?

It can be difficult to get a loan while Chapter 13 is still on your credit report. Having a bankruptcy on your report classifies you as a high-risk applicant. It could be easier to get a loan after seven years when Chapter 13 is removed from your credit history.

What happens after you pay off Chapter 13?

Any remaining qualifying balances are discharged once you complete the payment plan. This means that you no longer have to make payments, and creditors cannot try to collect those debts.

Key Takeaways

- Chapter 13 discharge releases debtors of eligible debts so they no longer have to make payments towards them. Creditors also can no longer try to collect money from them for these debts.

- Chapter 13 discharge is the final step of the Chapter 13 bankruptcy process.

- Your credit score will lower dramatically due to Chapter 13 being on your credit report. It will be removed after seven years.

- Credit scores tend to drop between 150 to 200 points after filing for bankruptcy. The average score is around 579.

Learn about more ways to get out of debt

Bankruptcy isn’t the only option you have to get out of debt. There are many strategies available to help people get back to financial stability, such as debt management programs and debt settlements.

Whether you’ve already filed for bankruptcy or are just struggling to make your current loan payments, take a minute to read about possible strategies and more here.

CS

Camilla has a background in journalism and business communications. She specializes in writing complex information in understandable ways. She has written on a variety of topics including money, science, personal finance, politics, and more. Her work has been published in the HuffPost, KSL.com, Deseret News, and more.

Share this post: