Can You Use A Personal Loan To Buy A House?

WM

Last updated 03/14/2024 by

William MorrissSummary:

You can use a personal loan to buy a house, but it’s usually a bad idea. However, there are special cases when buying a house with a personal loan could be your best option.

Using a personal loan to buy a home may sound unusual. It’s not often used to purchase a home but there are circumstances in which it’s possible. In certain cases, personal loans provide a better deal than a mortgage loan.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

Purchasing a home with a personal loan

Personal loans are a very popular financing method. In 2021, the personal loan market was worth $1.6 trillion (source).

However, personal loans are usually not a good way to buy a home because interest rates are higher and loan amounts are lower than those of mortgages. There are some scenarios, though, where a personal loan can be a good option.

Buying a tiny home, small home, or a mobile home

Many Americans are downsizing to smaller houses for a variety of reasons. They are more affordable and more environmentally friendly. They also have lower building costs and can be made mobile for traveling. You also save time and money on less cleaning and organizing. Not to mention the savings on moving costs if you frequently relocate or travel.

If you are considering building a tiny home or purchasing a smaller house that costs less than a single-family, personal loans may be a good choice. Personal loans can be a preferable option because some mortgage lenders may not wish to finance a tiny or mobile home.

In fact, many personal loan lenders offer loans that are designed for buying or building small and/or mobile homes. Be aware that if you use a personal loan in this way, you typically can’t use the home as collateral for the loan. The personal loan is given as a cash offer. One of the effects may be that the seller will be more interested because they don’t have to worry about a mortgage process when selling to you.

Buying a typical single-family House

In a scenario where you are purchasing a regular single-family home then personal loans may not be the optimal solution. A mortgage would likely be better in this case. This is because personal loans operate with a shorter repayment period. They can also include higher interest rates than many mortgages offer. These two factors make them less than ideal in this situation.

Taking out a personal loan for a down payment

Most homebuyers who want a standard single-family house will be looking for a typical mortgage. For a traditional mortgage, you can expect the lender to want between 3% and 20% as a down payment. The percentage they require will vary based on the lender you pick and your circumstance.

For example, some government-insured loans require a lesser down payment than conventional mortgages. You may be thinking about using a personal loan for that 3% down payment but it may not always be the best option here.

A lender will look at your debt-to-income ratio (DTI). If you use a personal loan to fund your down payment that increases your debt. This has an unfavorable impact on your ability to be approved for the mortgage. Furthermore, this can be a signal that you have issues managing money properly which presents more risk for them.

There are lots of uses for a personal loan but using them for a down payment may cause problems with the mortgage lender. Personal loans typically get used for debt consolidation, paying for emergency expenses, starting a business, home renovations, and financing a big expense.

Alternative ways to pay for a house

If you are unsure a personal loan is a good option for you or you are looking for alternative ways to finance a home, there are other choices. Alternatives to personal loans include grants, state programs, or other government-insured loans.

Both federal and state governments, as well as nonprofit organizations, provide aid for homebuyers. Some of these are geared toward first-time buyers but many apply to all home buyers generally. Furthermore, these payment assistance programs are still relevant if you have owned a home before. This is because of how they define a first-time buyer. Usually, a first-time buyer is any person who has not owned a house in the past three years.

Government agency—insured loans

These are a type of loans insured by a government agency. For example, the Federal Housing Administration (FHA) provides FHA loans. They call for a minimum down payment that starts at 3.5%. The Department of Veterans Affairs and the Department of Agriculture also provide loans. These are made for veterans or those looking to buy a house in a rural area, respectively. Both of these types of loans have no minimum down payment obligation.

Down payment grants

Many payment assistance programs make grants as opposed to loans. The benefit of a grant is that you don’t need to pay back the down payment. For instance, the National Homebuyers Fund provides a down payment assistance grant. The value of the grant is up to 5% of the loan amount for low- and medium-income homebuyers. What’s more, is this applies to you no matter if it is your first home or not. All qualified homebuyers can take advantage of the grant.

Home equity investments

If you already own a home, home equity investments can be a smart alternative for many homeowners because they offer cash in exchange for a share in the future value of your home. This means no debt, no interest, and no monthly payments to worry about until you sell your house or the contract ends. You can also use home equity investments to finance a down payment, renovate your new house or equip it for better security.

Here is SuperMoney’s list of the best home equity investors for financing a second property.

Secondary loan programs

Several states provide homebuyers with a secondary loan to assist with a modest down payment and closing costs. This includes programs like the California MyHome Assistance program. Tennessee’s Great Choice Plus program also offers similar assistance. These are not the only state programs, so it is a great idea to check your state for others to see what options it has on offer.

Traditional mortgages

Traditional loans are mortgages not backed by a government agency. However, certain loans supported by Fannie Mae and Freddie Mac will accept down payments of just 3%. Use SuperMoney’s free tools to compare mortgage lenders.

How buying a house with a personal loan can impact your credit score

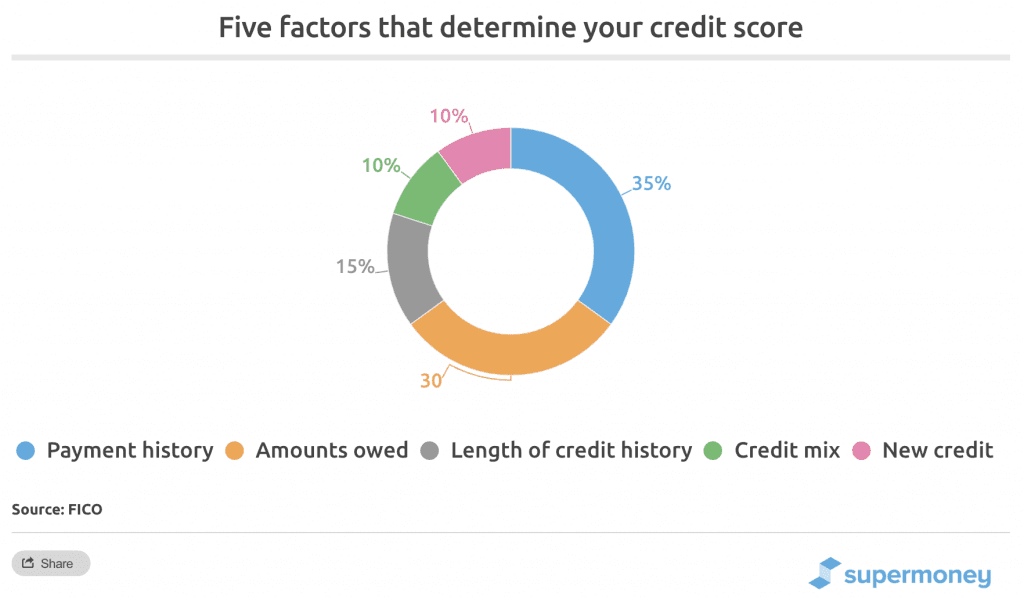

Whether you are using a personal loan or a mortgage, it’s important to understand the impact it may have on your credit. Your credit score helps lenders determine if you qualify for future loans as well as determine your interest rates. Typically, the higher your credit score the lower the interest rate but, it is not the only factor considered.

Usually, applying for personal loans will ding your credit score by several points. This is because a lender does a hard inquiry on your credit report. Although you may see a temporary dip this score is updated every month and is not stagnant. In other words, the change is not going to be permanent.

The way a personal loan impacts your credit will depend on you manage your monthly payments. If monthly payments are made on time and this activity is reported to the credit bureaus, your credit score should improve. Conversely, if you don’t pay on time or don’t pay at all, it will tank your credit score. Even if you can keep your current home after defaulting, this is going to make buying a home in the future very difficult. It will also impact your ability to apply for other forms of credit including things as simple as a credit card.

Automatic payments are some of the best ways to keep on top of your monthly payments. You may even be able to save money by doing this because many lenders offer a discount when you set it up. If you aren’t up for automatic payments, then consider setting a monthly reminder on your cell phone calendar. Both of these methods will help ensure your credit score doesn’t take a dip and you can get the best interest rate possible.

Check your credit report before applying for a loan

Whether you plan on using a conventional mortgage or a personal loan to buy a home, you should check your credit report first. It will let know where you stand in terms of your ability to qualify for the loan. It will also give you an indication of what kind of interest rates and terms you can expect. By knowing these factors, you can ensure you can get the best loan possible.

The major credit bureaus typically offer a free annual credit check. The report is accessible through their respective websites:

You should also check your credit report for any possible errors. Errors of a credit report can negatively impact your score and impact your ability to get favorable terms. You should address any of these inaccuracies before applying for personal or mortgage loans by filing a dispute. The turnaround time on a credit bureaus dispute can be a few weeks so act as soon as you see any issues in your report.

After you have checked your credit report for incorrect information and are informed on what kind of loan you want, you may want to shop around. Comparing different lenders will also make sure to get the optimal rate and save money.

Key takeaways

- If you are buying a home, personal loans are the most helpful if the property is a tiny home, smaller home, or mobile home.

- If you a buying a conventional single-family home, then a traditional mortgage may be better.

- Using a personal loan for a down payment may not be advisable because it increases your Debt-to-income ratio. This is a key factor in determining eligibility for a mortgage. It may give you the needed cash for the down payment but decrease your chances of getting approved for the mortgage after you take it out.

- There are alternative ways to pay for a house that include government-insured loans, programs, grants, and home equity investments. These options can reduce the down payments to as low as 3%.

- Applying for a personal loan can temporarily decrease your credit score so, be sure to make on-time payments to help it recover.

- Checking your credit score before applying for a loan and shopping around will make sure you get the best interest rates.

Conventional mortgages are usually the best option when buying a home, but if a personal loan makes sense for you, check some strategies on how to qualify for a personal loan. You may also want to compare the best personal loans so you know you get the best deal.

WM

Will Morriss is a writer for SuperMoney and an expert in financial services with a Master's in Business Administration. He has experience as a manager in sales and marketing and enjoys sharing his expertise with consumers and small businesses to help them solve problems and grow.

Share this post: