Cash to Close vs. Closing Costs: What’s the Difference?

LS

Summary:

In a nutshell, total closing costs (costs paid to the mortgage lender) are just one part of the amount needed to close the sale on a mortgage. The total cash you bring to your mortgage closing is referred to as cash to close (which, by the way, shouldn’t be actual cash).

If you’ve reached this point in the home-loan process, know that you’re almost at the finish line. And by this time you already know there’s a lot of paperwork and hoops to jump through to finalize your mortgage loan. Now it’s important to be prepared for the final costs you’re responsible for to successfully transfer the title into your name and get the keys to your new house.

Read on to learn the difference between cash-to-close vs. closing costs and what you need to know before you arrive at your closing date.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

Cash to close vs. closing costs

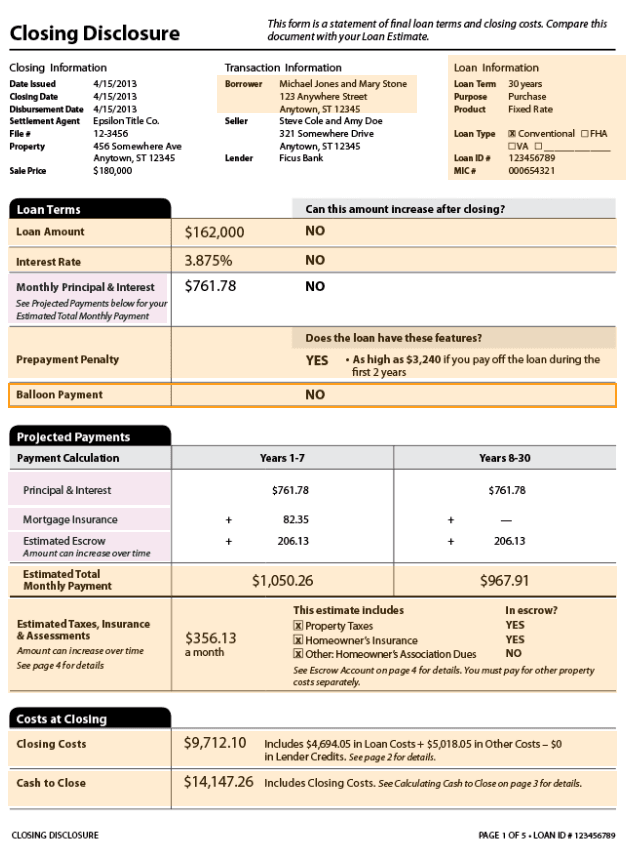

A few days before you close on your new home, you’ll be sent a closing disclosure. This is an official document that will tell you the total amount you need to bring to the closing table. Within this document, you’ll find:

- A summary of your loan terms, including the loan amount, interest rate, and monthly payment.

- Estimated property taxes, insurance, and other assessments.

- Costs due at closing, broken down into total closing costs and total cash to close.

- A detailed breakdown of how each cost was calculated.

The final line item on the first page of the closing disclosure is the cash to close, which covers closing costs as well as the remainder of your down payment. It will also include any expenses you need to pay in advance like property tax, homeowners insurance, and HOA fees (if applicable) plus any seller or lender credits.

It’s a good idea to compare the closing disclosure against the loan estimate, which you would have received at the beginning of the home-purchase transaction. The loan estimate and closing disclosure should be pretty similar. If there are any major discrepancies, you’ll want to discuss this with your mortgage lender to find out why.

Closing costs explained

To help distinguish closing costs from cash to close, remember that closing costs refer directly to charges and fees paid to the mortgage company to close on the loan. The various kinds of closing costs you pay depend on factors such as the state you live in, the type of loan you have, and the size of the down payment. The following are some of the more common costs you may encounter.

Application fees

Application fees, sometimes known as processing fees, are what you pay the lender for administrative costs to process your loan application. This is usually a non-refundable fee and could cost as much as $500 — only to find out you lack the credit history to obtain a mortgage.

If possible, shop for lenders who don’t charge an application fee — many online lenders don’t, for example. At the very least, get pre-approved for the loan first, which is typically a quick (and free) procedure.

Origination fees

An origination fee is what you’ll pay to cover the costs of the underwriting of your loan. Underwriting is where the lender determines if you’re eligible for the mortgage loan by examining your credit report, income, assets, and debt-to-income ratio (DTI), among other details of your financial situation. And, though costs are lower than they were in the 1990s, origination costs are gradually increasing.

At this point, it’s common for mortgage lenders to ask for additional documentation from you such as an explanation of bank deposits or proof of assets. The underwriting process can take a long time — weeks, maybe — but you can help speed up the procedure by providing all of the necessary documents in a timely manner.

To avoid origination fees altogether, take a look at some of the mortgage lenders below.

Recording fees

These are the fees paid to record the transfer of ownership from the seller to the buyer. The cost of recording fees varies depending on the county where the property is located. Your property’s location will also affect how the fee is charged: either as a flat fee or a fee for the first page and a smaller charge for each additional page.

Your real estate attorney or agent should be aware of the cost of recording fees in your county, or you can look it up online.

Appraisal fees

Mortgage lenders require a property to be appraised to ensure that the home’s purchase price (and therefore your loan amount) isn’t more than the property is actually worth. And, of course, there’s a fee for an independent appraiser to come out and determine the value of the property.

Title insurance and title search fees

Title insurance is meant to protect you in the event of any third-party claims against your property. You’ll usually pay upfront for title insurance on your closing day, and it provides protection for as long as you own the property. In some cases, the seller may be required to pay for this insurance.

The title search is the procedure where attorneys or title companies investigate public records to look for liens, debts, or other encumbrances to the property. This ensures the seller is legally able to sell to you and that the title is free and clear of any claims.

Related reading: To learn more about encumbrances in general, take a look at our article that discusses encumbrances in-depth as well as the different kinds of encumbrances.

Attorney fees or settlement fees

Some states don’t require an attorney to be present at a mortgage closing, but if so they’ll handle the title transfer and generally help facilitate the real estate transaction. If an attorney isn’t required, an escrow agent, settlement agent, or similar will handle the transfer of the title for a settlement fee.

PMI

Private mortgage insurance (PMI) is usually required by lenders if you’re making a down payment of less than 20%. For example, if you’re buying a house for $200,000, you’d need to put down at least $40,000 to avoid a monthly PMI payment (which is typically rolled into your mortgage payment). PMI is protection for the lender in the event that you default on the loan.

Fees for government-backed loans

If you have a government-backed loan, such as an FHA or VA loan, you may have to pay other fees on top of what’s required for a conventional loan. For example, if you have an FHA loan, you’ll pay an upfront mortgage insurance premium (MIP) at closing and a monthly premium as well.

Despite the additional fees, these loans can provide financing for first-time homebuyers or other buyers that may be in a difficult financial spot. To see how government-backed loans compare to conventional mortgages, take a look at the options below.

Home inspection fees

While a home inspection isn’t usually required by lenders, it’s important to have one anyway. A lot of issues with a home are visually undetectable. An unbiased third-party home inspector will examine your house from top to bottom and alert you of any problems. Things they’ll look at include the roof, attic, basement, foundation, plumbing, electrical, and HVAC systems.

Oftentimes the home inspection will reveal issues that the homebuyer may want to ask the seller to rectify before the sale goes through. Alternatively, you can ask for seller credits to offset the price of repairs you may need to make.

Sometimes the problems the home inspector finds may be so severe you decide not to go through with the purchase altogether. In that case, if you’ve already paid earnest money, you should be able to get that deposit back.

IMPORTANT! Keep a careful record of any closing costs you paid prior to the closing day. Check this against your closing disclosure to make sure there aren’t any discrepancies. You want to make sure you’ve been credited for any payments you’ve already made.

Can you negotiate on closing costs?

Depending on the housing market, there are various ways to lower your costs at closing. This is why it’s so important to shop around for the best deals and be sure to read the fine print.

“I prefer to use direct lenders who will match rates and don’t have a lot of junk fees,” says Kristen Conti, Broker-Owner at Peacock Premier Properties.

Pro Tip

“I always recommend that clients initially start with their current insurance provider and find out if they have a homeowners insurance product and what that pricing might be especially to find out if there’s any preferential pricing for current clients,” advises Nicole Beauchamp, Senior Global Real Estate Advisor and Licensed Associate Real Estate Broker at Engel & Volkers.

Cash to close breakdown

Again, the cash to close includes your closing costs, which are outlined above. But in order to estimate cash to close, you’ll need to factor in the rest of your down payment, pro-rated mortgage interest, and any taxes or insurance you’ll need to prepay at the closing table.

Remainder of down payment

When you initiate a real estate purchase, you’re usually required to pay earnest money. This basically shows you’re serious about the property and is often a percentage of the home’s purchase price.

For example, if the purchase price is $200,000 and the earnest money required is 1%, you’ll pay $2,000 in earnest money. So if you’re putting 20% down, or $40,000, you’ll only owe an additional $38,000 for the down payment in your cash-to-close costs.

Prepaid expenses

Also included in the cash-to-close tally are items that you need to pay in advance. For example, you’ll have to prepay some of your mortgage interest, which is pro-rated from your closing day to when you start making payments. You also need to prepay a portion of your homeowners’ insurance and taxes.

Together, these costs make up your cash-to-close costs. Keep in mind, there may also be credits, discounts, or other adjustments from the seller or lender that will reduce your total cash-to-close expenses.

How to calculate cash to close

You probably don’t need to calculate cash-to-close costs as the full amount will be listed on your disclosure. However, if you want to know sooner than a few days before the closing day, and make sure you have enough money in your bank account, you can figure out the estimated cash you’ll need ahead of time.

First add up your total closing costs, plus the down payment and prepaid costs like insurance, taxes, and mortgage interest. From there you’ll subtract any seller or lender credits, the earnest money you’ve spent, and any of the closing costs you’ve already paid for prior to the closing day. This should bring you to the estimated cash you’ll need at the closing table.

How to pay your cash to close

As mentioned, on your closing day, you’ll need to pay any outstanding costs associated with the home purchase transaction. The preferred payment method may differ depending on your lender and other factors, but most lenders probably won’t accept a personal check, credit card, or debit card. In general, there are three preferred payment methods.

- Wire transfer

- Cashier’s check

- Certified check

Traditional lenders will likely accept a cashier’s check or certified check, but online lenders or others may prefer to deal with wire transfers. If you do a wire transfer, be sure you verify the details of the process before you get to your closing day.

FAQs

Can cash to close cash be rolled into a loan?

Some, but not necessarily all, costs associated with closing on your home loan can be rolled into the mortgage. You’ll need to talk to your lender about what you can and can’t include in your loan.

However, keep in mind that you’ll now have to pay interest on those closing fees, which means you’re ultimately paying more for your mortgage in the long run. It’s typically in your best interest to pay any upfront costs out of pocket if you can.

Can I use a cash advance for closing costs?

While you can get a cash advance from a credit card to pay for your closing costs, you’re not doing yourself any favors. For one thing, the interest rate on a cash advance is much higher than you’ll pay for regular purchases.

In addition, fees associated with cash advances are usually 3% to 5% of the withdrawal. Even at the low end of the spectrum, and aside from the exorbitant interest charges, a $10,000 cash advance at 3% will cost you an additional $300.

Key Takeaways

- Cash to close is all the money you need to bring to the closing table to finalize the real estate purchase.

- Closing costs are just a portion of the cash-to-close costs you have to pay on your closing date.

- Closing costs include charges paid directly to the lender. These costs include multiple fees, such as application fees, appraisal fees, origination charges, and attorney fees. Additional other costs may apply depending on your state, loan type, and the amount of your down payment.

- Cash to close also includes the rest of your down payment, a pro-rated amount of mortgage interest, and any other prepaid expenses like property tax and insurance.

- Your cash-to-close costs are reduced by any seller credits or lender credits.

- Government-backed loans, such as VA loans or USDA loans have their own fees you’ll also need to factor into your cash-to-close expenses.

Share this post: