How To Respond To IRS CP14 Notice

DH

Last updated 03/20/2024 by

Denicki HolcombSummary:

The IRS sends a CP14 Notice when you owe money on unpaid taxes. The document explains 1) what years you owe taxes for, 2) how much you owe, and 3) the deadline before penalties and interest begin. Find out how you can respond to a CP14 Notice and when it’s a good idea to hire a tax professional.

It can be scary to receive mail from the IRS, especially if it’s unexpected. However, there is no need to panic. The CP14 is the first debt notice the IRS sends. So, you usually have plenty of time and options available to handle your tax debt. Having said that, owing the IRS money is not a joking matter, so it’s a good idea to act fast. Here’s what you need to know.

End Your IRS Tax Problems

Get a free consultation from a leading tax expert.

It's quick, easy and won’t cost you anything.

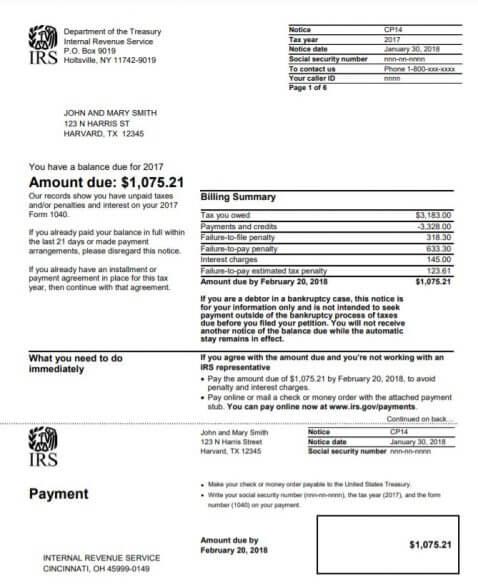

What is the CP14 Notice?

The IRS uses the CP14 Notice to inform taxpayers they have unpaid taxes. The tax debt balance in a CP14 may also include tax penalties and interest on those tax debts. This can happen for many reasons, such as filing a tax return with a balance due and failing to pay for it on time. It may also be triggered by a tax audit that reveals unreported income.

A CP14 will provide the following information:

- The year for your unpaid taxes, or the period you owe for

- The amount of taxes, interest, and any penalties you may owe

- The deadline for the payment

You can receive a penalty if you don’t file your tax return during a specific period, or on time. You can also receive one if you do not pay the entirety of your quarterly tax payments.

Here is a comprehensive list of notices and letters the IRS uses to communicate with taxpayers.

What should you do if you receive a CP14 Notice?

Dealing with a large tax debt can be overwhelming. However, ignoring your situation is not a good idea when dealing with the IRS. Here is a step-by-step guide of what you should do.

- Read the CP14 Notice carefully. You definitely want to focus on how you owe and your repayment options.

- If the amount the IRS claims you owe is correct and you can afford to pay it, do so as soon as possible. You don’t want to owe money to the most powerful debt collector in the United States if you can avoid it.

- Check the deadline for paying the tax debt in the CP14 Notice before interest and penalties start accruing.

- If you find errors or discrepancies in what the IRS is claiming you owe, you must act quickly. The IRS needs to be informed in writing about the discrepancy within 60 days of the date on the CP14.

If you agree with the CP14 Notice

If you agree with the IRS but you can’t afford to pay your debt, you can either contact the IRS and negotiate directly or hire a tax professional to help you out. You can call the IRS number printed on the CP14 Notice, and ask for a payment plan, or a possible OIC (or offer in compromise). The OIC requires filling out an application form, either a 433-A or a form 656 for businesses. Form 656 requires an application fee of $205, which has to be paid when you send in the form.

Note that filing for an installment loan may not be the best option available for you. And filing for an offer in compromise can be complicated. Consider getting a free consultation with a tax relief professional to assess your options before you make a decision. Here is SuperMoney’s list of the best tax relief companies.

If you disagree with the CP14 Notice

If you disagree with the amount shown on the CP14, you will need to collect evidence to prove your case before the IRS. You can do this yourself or get the help of a tax relief company. Make sure you choose a firm that hires tax attorneys or enrolled agents.

What happens if you don’t respond to a CP14 Notice?

If you don’t respond to the CP14 in due time, (which is typically 30 days), you will receive a CP501, and if it is not paid by that point, a CP503 then a CP504. At this point, the IRS will take one of several steps to obtain the money which you owe, including:

- Starting a wage garnishment, which will pull money from your paychecks until the amount is paid

- A levy from your social security benefits, or a bank levy which will take the funds directly from your bank account

- File a Notice Of Federal Tax Lien, which will put a public record showing an IRS lien against your property.

What to do if you have already made a payment?

The IRS can take up to 21 days to process a payment, in which case, you can disregard the payment options and anything on the Notice. It will be updated soon, and show that you have made the payment, which will stop any bills from being sent to you about the tax payments.

What if you already set up a payment plan?

The IRS uses an automated system for their payment plans, so you will continue making the payments for the plan you’ve chosen unless it shows a new amount on the CP14. In that case, you will contact the number on the CP14 letter, and discuss the matter with an IRS agent to find out if you need to change the amount you pay.

Read this for a detailed review of available IRS payment plans.

Key takeaways

- The IRS uses the CP14 Notice to inform taxpayers they have unpaid taxes. The tax debt balance in a CP14 may also include tax penalties and interest on those tax debts.

- Read the CP14 Notice carefully. You definitely want to focus on how you owe and your repayment options.

- Check the deadline for paying the tax debt in the CP14 Notice before interest and penalties start accruing.

- If you agree with the IRS but you can’t afford to pay your debt, you can either contact the IRS and negotiate directly or hire a tax professional to help you out.

- If you disagree with the amount shown on the CP14, you will need to collect evidence to prove your case before the IRS. It may be helpful to hire a tax relief firm that employs tax attorneys or enrolled agents.

Share this post: