Do I Have To Pay Taxes On My Checking Account?

EA

Last updated 03/26/2024 by

Emily AfricaSummary:

You do have to pay taxes on the interest you earn from your checking account. This is because the IRS requires you to report all income earned, including any interest earned from your checking account. However, there are ways to lower the taxes you pay on earned interest.

Checking accounts are a great way to store your money and make it work for you. But did you know that you have to pay taxes on the interest from your checking account? In this article post, we will cover the basics of paying taxes on earned interest on your checking account balance. For some background knowledge, read SuperMoney’s guide to checking accounts.

Compare Checking Accounts

Compare checking accounts. Discover your best option.

What is taxable interest income?

Some financial institutions offer interest payments on your checking account balance in the form of interest. The interest rates will be lower than most other savings accounts or money market accounts, but if you’re looking for more accessibility, then this might just do the trick! All interest earned from your bank accounts is taxable.

Learn more from SuperMoney about the other benefits of checking accounts.

How much interest income do you have to report?

The IRS requires you to report all income, even if it is small. This includes any side businesses and interest or dividends from stocks.

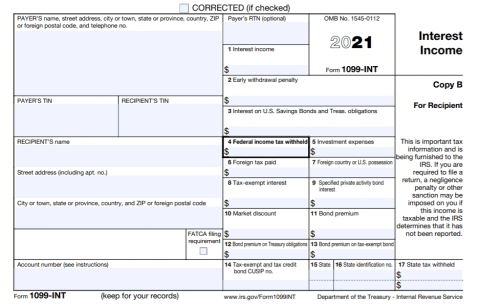

When it comes to your checking account, the bank will send you Form 1099-INT at year’s end. You only receive this form if you’ve earned more than $10 in interest. To stay compliant with tax laws, you need to report all income, even if you earned less than $10 in interest and don’t receive Form 1099.

How much interest do you earn on a checking account?

Nobody likes paying taxes, but you probably won’t have to pay much on the interest you earn from a checking account — mostly because checking accounts pay very little interest. If you earn more than $10 in interest from your checking account, you probably should find a new investment.

For example, the average checking account pays 0.03% interest on your balance. So, if you have an average of $3,000 in your account and you earn a 0.03% APY, you will get a whopping $0.90 in interest by the end of the year. Before taxes that is.

Do banks report your checking account information to the IRS?

Banks are required to report 1099s to the IRS, even if you don’t receive one. This is why it is always a good idea to report all of your interest income. Check with your bank if you have any questions about what they report on their end. If the IRS audits your taxes and finds that you have under-reported income, there could be penalties for not reporting all interest income.

How much can you have in a bank account before paying taxes?

It’s worth repeating that the IRS requires you to report all income when you file your taxes. You will pay taxes on earned income before it enters your checking account, so your balance doesn’t determine how much you pay in taxes. Interested earned on that balance, however, must be reported.

Do I need a tax form for my checking account?

Interest is taxed at your marginal rate and your income determines your tax bracket. Your tax bracket and tax rate will depend on your income, interest earned, and filing status.

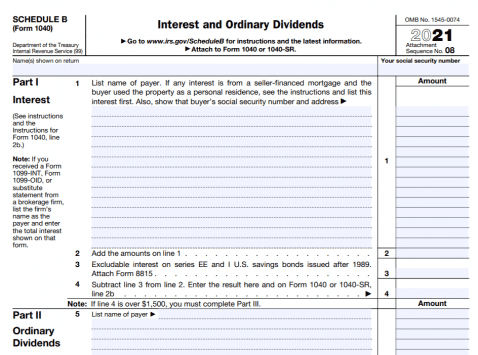

If your interest earnings are less than $1,500, you can report your income on your Form 1040. If you make more than $1,500 in interest for the year, you will file a Schedule B with the IRS. Note that filing a Schedule B makes you ineligible to file a 1040A.

How do I legally avoid paying taxes on interest income?

You can’t legally avoid paying taxes on the interest you earn from a regular checking account. However, there are ways to avoid paying interest on certain savings accounts and there are plenty of methods for lowering your overall tax bill. Here are three examples.

- Contribute to a health savings account (HSA): Under a High Deductible Health Plan, you can save money for your healthcare needs. The money you contribute to your HSA can be deducted from your taxable income at the end of the year!

- Opt into your employer’s retirement plan: Lower your taxable income by contributing to your 401(k), a 403(b), a 457, or Thrift Savings Plan.

- Contribute to your Individual Retirement Account (IRA): You can write off money contributed to your IRA and therefore lower your taxable income. This is another great way to save money during tax season.

Do you have to pay taxes on your checking account?

The IRS requires you to report any interest earned on your checking account. You’ll have to pay taxes on those earnings per your tax bracket’s tax rate. However, there are some ways that you can save this money elsewhere by contributing to health savings or retirement accounts that lower your taxable income.

If you are interested in opening a checking account with a new bank, check out some of the best checking accounts. Better yet, try browsing through some of the best free checking accounts.

Key Takeaways

- The IRS requires you to report any earned income on your taxes, even the interest you receive from your checking account balance.

- Depending on how much interest you earn, you may have to file various forms. Visit the IRS website for more information.

- To avoid paying taxes on the interest earned in your checking account, you can contribute to a health or retirement account.

Share this post: