Earthquake Insurance

AL

Last updated 03/14/2024 by

Andrew LathamFact checked by

Some people assume earthquakes in the U.S. don’t cause mass destruction, but this is incorrect.

In 1994, the Northridge earthquake caused $15.3 billion of insured damages ($25.6 billion in 2017 dollars). This disaster was the 5th costliest disaster of all time.

But homeowners insurance and renters insurance policies may not cover damages. That’s where earthquake insurance comes into play. Here’s what you need to know to help you decide if earthquake insurance is right for you.

Compare Home Insurance Providers

Compare multiple vetted providers. Discover your best option.

Why you need earthquake insurance

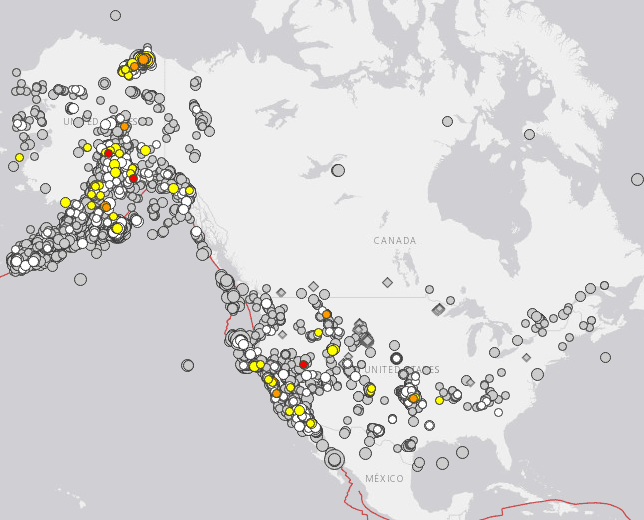

From September 2017 to September 2018, over 4,960 earthquakes of a magnitude of three or more hit North America. Earthquakes can cause destruction to your home. They can damage the foundation of your home, collapse your walls, or even destroy family keepsakes. It all depends on the magnitude of the tremor.

If an earthquake causes a fire, a standard policy may pay for some repairs. The policy may also cover additional living expenses if your home is unlivable. But the majority of homeowners and renters insurance policies will not cover direct destruction caused by earthquakes.

What is covered by earthquake insurance?

Earthquake insurance covers most repairs needed. If you have additional structures attached to your home, such as a garage, your policy may cover the damages.

Earthquake insurance may also cover the additional costs to get your building up to code and replace structural damage to your property.

Homeowners or renters insurance does not cover earthquake damage. You need to add it on as an endorsement or written agreement. This may increase the insurance premium.

Sometimes it makes sense to get a separate policy. Speak with your insurance agent and discuss the best option for your insurance needs.

What isn’t covered by earthquake insurance?

Earthquake coverage doesn’t cover all loss or financial burden due to an earthquake.

Exclusions may vary by insurance provider, but here are a few of the most common exclusions:

- Fire: Your home insurance policy usually covers damage due to fire. Earthquakes can puncture gas lines that can lead to fires.

- Vehicles: Your auto insurance policy may pay for the damages to your vehicle. If your car is parked in your garage, earthquake insurance will not cover the damages.

- External water damage: If an earthquake were to cause a flood and water damage, your policy may not pay for repairs. This is what a flood insurance policy is for.

- Land: Generally, this coverage won’t cover sinkholes or erosion to your property due to an earthquake. There may be an exception if your policy includes Engineering Cost coverage. This coverage will pay a portion of the cost to stabilize the land.

- Previous damage: If your property has pre-existing damage from an earthquake, your policy will not cover it.

- Brickwork: If you have any masonry veneer—brickwork, stone, or rock that covers your home, you will want to discuss this before purchasing a policy. Some insurance policies may not cover the costs of masonry veneer. They may evaluate the cost of repairs using sliding materials or stucco.

How much coverage do you need?

Most earthquake insurance policies have limits to their coverage. They may also have sublimits that limit the amount of coverage you can receive for a certain category. For example, the policy could have a sublimit of $4,000 for computers.

When you insure your home for the appraisal value or loans value, you will generally have enough to cover the reconstruction of the home.

Dwelling coverage on your homeowners and earthquakes insurance usually have the same limit. Regularly review your policy and make sure your dwelling coverage doesn’t drop below 80% of your home’s value.

If it does drop below 80% of the home’s value, the insurance company may reduce the amount they will pay on a claim.

When determining how much coverage you will need, here are some important questions you should ask yourself:

- How much would it cost if your home was destroyed? What portion of the damages could you pay?

- How much would it cost to repair the damages to your household items, such as furniture or personal items? Is this something you could afford to repair?

- If something happens to your home that makes it unlivable, could you pay for additional accommodations while your home was rebuilt? Will you need a temporary housing option?

Is it worth it to buy earthquake insurance?

According to the United States Geological Survey’s (USGS), nearly half of all Americans are at earthquake risk. This number includes 143 million people and 48 states.

Purchasing earthquake insurance could be worth it even if you don’t live near a fault line. As a result of oil drilling, some cities experience an uptick in seismic activity, such as Oklahoma.

If you are considering buying a home in areas that have frequent earthquakes, you may want to entertain purchasing earthquake insurance.

Here are a few questions to consider when determining if earthquake insurance is worth it:

- Could you afford to pay for temporary housing and additional expenses?

- If your personal items and furniture are damaged, could you afford to replace it?

- Could you afford the expenditures for reconstruction of your home if it was damaged?

Assess your policy needs and determine if you need earthquake insurance to fill in the financial gap.

How do earthquake insurance companies calculate your premium?

Earthquake insurance premiums may vary by location and property characteristics.

Some of the most common factors insurance companies use when determining earthquake insurance premiums include:

- The age of the home: If you have an older home, your premium could be higher.

- The location of the home: If your home is located in an earthquake-prone area or a fault line, premiums tend to be higher.

- The structure of the home: Does your home have a concrete foundation or a slab block foundation? Does your home have a wood frame or brick structure? How many stories is it? Does it have a finished basement? These are all factors that can have an impact on an earthquake insurance premium.

- The estimated expense of rebuilding the home: There are two options for replacing the contents of the home. You can choose to get a policy that provides replacement value, which will replace the contents of the damage. Another option is to select a policy with a cash value offer that pays a cash value for contents of home based on age and wear.

- The deductibles: You can also select a larger deductible to lower your premium. However, if an earthquake were to take place and cause damage, you’ll need to pay the full deductible amount.

There are many factors that will determine your premium. That’s why it’s important to shop around for the best insurance policy.

Another factor to consider is that, as with other types of residential insurance, your earthquake insurance policy is not tax deductible.

Reach out to several insurance companies and get an earthquake insurance quote. This will help with the decision-making process.

How to find the best earthquake insurance

Once you decide you need earthquake insurance, you will want to begin the shopping process. However, it can be a challenge finding the best policy. That’s why it’s important to do research in advance.

First, start with your current home insurance provider. Your insurance provider may be able to add coverage as an endorsement or written change to your policy. If your current insurance provider is unable to add the additional coverage, ask to be connected with another insurance agency.

If there has been a recent earthquake occurrence, agencies may not sell policies for 30 to 60 days. You will have to wait until the hold period passes before purchasing coverage.

Insurance agencies will have a variety of rates for your coverage. Many insurance providers have varying levels of customer service and claim procedures.

Note that earthquake insurance deductibles tend to be higher than a home insurance or renters insurance policy. They can range from between 5% and 25% of the policy limit.

These are also important factors when selecting an insurance provider.

Best earthquake insurance companies

Now that you understand the importance of earthquake insurance—even if you don’t live in California—you should identify the best earthquake insurance companies.

Here are some top insurance providers to consider:

- Geico offers coverage in all 50 states including Washington D.C. They have a SuperMoney financial rating of A+. This means it has a strong ability to pay its contracts and policies.

- Progressive also offers coverage in all 50 states including Washington D.C. They have a financial rating of A+.

- USAAhas a financial rating score of A+. They offer coverages in all 50 states including Washington D.C.

- Nationwide offers coverage in 42 states including Washington D.C. They also have a financial rating of A+.

- Farmers Insurance Groupoffers coverage to 47 states including Washington D.C. They have a financial rating of an A, which is the second highest score available.

The bottom line

You never know when an earthquake could harm your home. And not all insurance policies are the same, so make sure to do your research before purchasing one.

Identify your insurance priorities and visit our home insurance page to find the best policy for your needs and location. On it, you’ll find a complete overview of today’s leading providers.

Carefully compare their rates and coverage side-by-side, and select a plan that will best help protect your property in case of an earthquake.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: