What is a 3/1 ARM and is It a Good Idea?

LS

Last updated 04/08/2024 by

Lacey StarkSummary:

Most home mortgage loans have simple terms, last between 15 and 30 years, and have fixed rates. You get an interest rate that is good for the life of the loan and your monthly mortgage payment stays the same. But this type of loan isn’t for everyone — maybe you’re looking for a lower monthly payment in the short term or you want to sell within a few years. In those instances, a 3/1 adjustable-rate mortgage, also known as a 3/1 ARM, might be the right choice for you.

As you start looking for a home to buy, unless you’re paying cash, you need to obtain a mortgage. Lenders have a multitude of mortgage options to consider. Each kind carries different terms and interest rates, and your loan officer will help you decide which option is appropriate for your specific circumstances. You might want to ask a real estate agent about other mortgages, too. Experienced realtors are likely familiar with all types, and they’ll have a unique perspective separate from mortgage lenders.

For now, let’s talk about adjustable-rate mortgages (ARM) and the individual conditions that could make this the ideal home loan for you. Specifically, let’s examine the 3/1 ARM — what it means, the precise terms of the loans, the risks and rewards, and exactly when this might just be the perfect option for you.

What is a 3/1 adjustable-rate mortgage?

A 3/1 ARM is a type of loan where the interest rate is the same for the first three years and then adjusts up or down each year for the remainder of the loan term. These loans offer a much better interest rate for the first three years than you could hope for with a traditional fixed-rate mortgage.

You can probably guess the obvious downside — you have no idea what your interest rate will be for the remaining years, and it changes every year. However, there are situations where this type of loan (or its siblings, the 5/1, 7/1, or 10/1 ARMs) is attractive to a buyer. It’s a great idea if they plan on selling before the fixed-rate period is over.

If you can’t imagine where to start looking for an adjustable-rate mortgage, look no further. SuperMoney collects and compares a variety of ARMs that are available to you with a simple click.

What is a 3/1 conforming ARM?

A 3/1 conforming ARM is a an adjusted rate mortgage that meets the dollar limits set by the Federal Housing Finance Agency (FHFA) and the funding criteria of Freddie Mac and Fannie Mae. If you have excellent credit a conforming loan can be a good option because they provide competitive interest rates.

What does a 3/1 hybrid ARM loan mean?

A hybrid loan means the mortgage is a combination of fixed interest and adjustable rates. It differs from a fixed-rate loan, which has a, well, fixed rate throughout the entire loan term.

What is a 3/1 loan term?

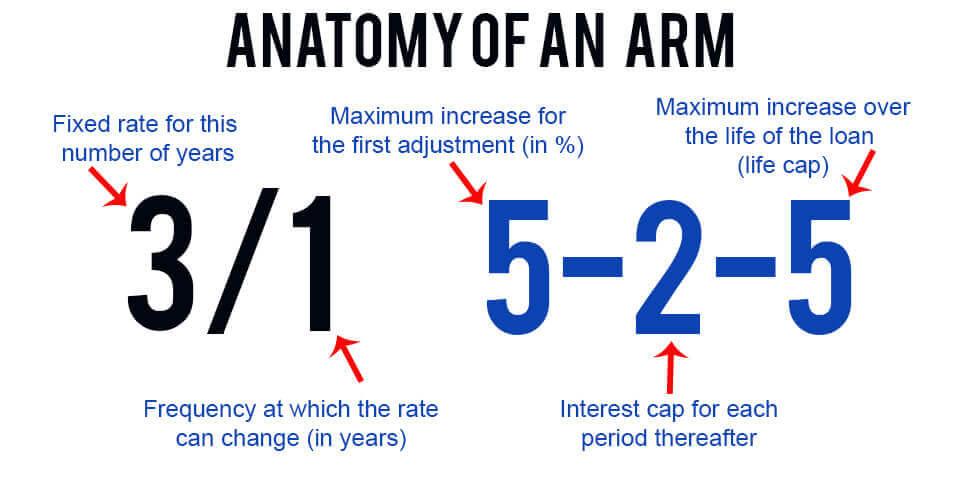

A 3/1 term describes mortgage loans that carry fixed rates for the first three years and then move to adjustable interest rates for the remainder of the loan. The three in the 3/1 is the initial three-year period, and the one in 3/1 refers to the fact that the rate will be adjusted every year.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

3/1 ARM Rates

As of early February 2022, the average national home mortgage rate hovered in the 3.4% range. By comparison, a 3/1 ARM rate is about 2.8%. That’s a pretty hefty difference and saves you a ton of money in interest fees. As mentioned previously, though, that interest rate is subject to fluctuation after the three years is over. Let’s take a look at how this might affect your mortgage payments.

Example:

Imagine buying a house right now for $300,000 when you’re planning to move to Italy in two or three years. This makes you an ideal candidate for a 3/1 adjustable-rate mortgage. Let’s also assume you come prepared with a 20% down payment and your interest rate is 4% for the initial fixed period. Your monthly payment is about $1,409 (excluding taxes and insurance), which you can expect for the next three years.

Imagine buying a house right now for $300,000 when you’re planning to move to Italy in two or three years. This makes you an ideal candidate for a 3/1 adjustable-rate mortgage. Let’s also assume you come prepared with a 20% down payment and your interest rate is 4% for the initial fixed period. Your monthly payment is about $1,409 (excluding taxes and insurance), which you can expect for the next three years.

Then consider what happens after that three years is up. Your mortgage rate may increase by two percentage points. Now your payment is $1,702 per month. And, in a few years, the rate goes up yet again another two points, so now you’re looking at a $2,025 monthly mortgage bill. This is a simple example, but it illustrates a worst-case scenario of what could happen if you don’t leave that mortgage before the fixed-rate period ends.

A note about caps and floors

While it’s unlikely mortgage interest rates will swoop as high as they did in the 1980s — when, yikes, they reached the upper teens — fluctuation will happen. This is why lenders add rate caps and floors to an ARM.

Caps: Interest rate caps protect the borrower from ridiculously elevated interest rates after those first three years. Caps often look something like this: 2/2/5. In this case, your cap, after the fixed-rate period, is set at two (the first number). This means your first interest-rate adjustment can’t go higher than two percentage points. So, for example, if your initial interest rate was 2.84%, your new rate couldn’t be any more than 4.84%. Not too bad. Yet.

But there’s a twist. When your rate adjusts the following year, it could go up another two points (that second number), making your rate as high as 6.84%. Then there’s the third cap (the five in that 2/2/5 example) that says your maximum interest rate can’t go up by more than five points for the life of the loan. It won’t get any higher than that, but you could still pay an interest rate of 7.84%. Ouch. That’s incredibly high by today’s standards. Yes, rates can go down (hello, pandemic) but you can’t plan for that. And that is why, one way or another, you need to get out of a 3/1 ARM before your initial three years are up.

Floors: Floors are put in place to protect the lender. Let’s assume the floor is set by the lender at a rate of 3.50%. This means that no matter what happens with the economy, the mortgage company will never get less than a 3.50% interest rate on your mortgage loan. Let’s face it, mortgage lenders will do everything they can to protect their investment in you and make a profit, and we as buyers are at their mercy.

Pro Tip

As you research adjustable-rate mortgages, compare rate caps along with interest rates. Lenders might offer the same fixed interest rate upfront but offer different rate caps. This could impact your monthly mortgage payments if you’re saddled with that loan for longer than intended.

When should you consider a 3/1 ARM?

A 3/1 ARM is not usually a good option for people who intend to live in the house for a long time. In that case, you’re better off getting a traditional loan for 15, 20, or 30 years — whichever is most feasible for your budget. An exception to that scenario, however, is if you know you can pay off your house in three years. In that case, by all means, get the lower interest rate and pay that sucker off as soon as you can.

The ideal candidates for this loan, usually, are buyers that plan to sell and move in less than three years. This way they never have to deal with that pesky adjustable rate. Sure, the interest rate could go down, but you can’t expect or plan for that. Another option is to refinance the house after three years, but this can be risky too.

Perhaps you experienced a reduction in income, your credit score dropped, or your house is worth less than you originally paid for it. Any of those factors, or a combination thereof, may make it impossible to refinance. Then you’re either stuck with the terms of the loan or have to sell the house.

3/1 ARM vs. 5/1 ARM

While the 3/1 ARM has a fixed initial interest rate for three years, the 5/1 ARM — you guessed it — gives you five years at that stable rate. This is a less risky proposition for the borrower because you get two extra years of breathing room along with a lower mortgage payment. For those without a secure plan after three years, a 5/1 ARM might be the loan for you.

What are the pros and cons of a 3/1 ARM?

Key Takeaways

- If you plan on selling within three years, the 3/1 adjustable-rate mortgage is an excellent option.

- Pay attention to the interest rate caps offered by different lenders since they do vary.

- If you’re planning on living in the house for a long time, this isn’t the mortgage for you.

- Consider 5/1 adjustable rate mortgages (or 7/1 or 10/1) if you need a little more time to make your plans, but don’t want to live there forever.

Share this post: