CPN Number: What Is It and Do You Need It?

JA

Summary:

A CPN, short for credit privacy number or credit protection number, is a nine-digit number that works just like a Social Security number (SSN). Fraudulent companies sell this number to customers with bad credit to help them hide the poor credit history associated with their original SSN.

Credit scores are often used by lenders to determine your creditworthiness and which interest rates to offer you. For this reason, having a below-average credit score can make it difficult to get approved for a loan with reasonable terms. Moreover, a low credit score can also make it harder to rent an apartment or get a job. This is where CPNs come in. This nine-digit number essentially helps you create a new credit identity and improve your creditworthiness. But is it legal? And what are the consequences of using it?

Though this may seem viable, it’s not legal by any means. In fact, you could risk getting yourself into serious legal trouble if you’re caught using a CPN. In this article, we’ll dive deeper into how this number works, why you shouldn’t attempt to get a CPN, and explore the steps you can take to revive your credit score the legal way.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Why buying a CPN number is a scam

Wiping your slate clean with a CPN may seem like a great deal, but it’s actually a scam. When you use a CPN, financial institutions and credit card companies are alerted that your CPN doesn’t match the SSN you’ve used in the past. These numbers aren’t issued by the federal government and have no legal standing whatsoever — it’s considered a federal crime to use a CPN. And even if you don’t get caught right away, you could still face future criminal charges.

If you see internet ads or credit companies claiming that they can offer you a CPN (or a secondary SSN), know that they are scammers. Trusting them with your personal information could result in legal and financial issues that could further worsen your situation.

Why would some people use CPN numbers?

Why would anyone attempt to use a CPN number when it’s so risky? Well, there are some scenarios where having a CPN can seem like a good option. For example, some consumers use CPNs as a way to try to shield their SSNs and protect themselves from identity theft. Instead of using their SSNs in credit applications and job applications, they use CPNs to avoid letting their confidential information fall into the wrong hands.

Another one of the most common reasons why many people resort to CPNs is to hide their poor credit history and start fresh in their credit journey. Having a low credit score can be a hindrance to many opportunities such as landing a job or getting an apartment. So, for these consumers, the idea of using a CPN in place of their SSN can seem like an appealing option.

CPN alternatives: Legitimate ways to improve your credit

Instead of figuring out how to obtain a CPN, it’s much safer and wiser to dedicate that time to legally improving your credit score. There are a number of ways to improve your credit without dealing with fishy companies that aren’t in your best interest. As long as you are persistent in rebuilding your credit, you’ll see your hard work pay off.

Lower your credit utilization ratio

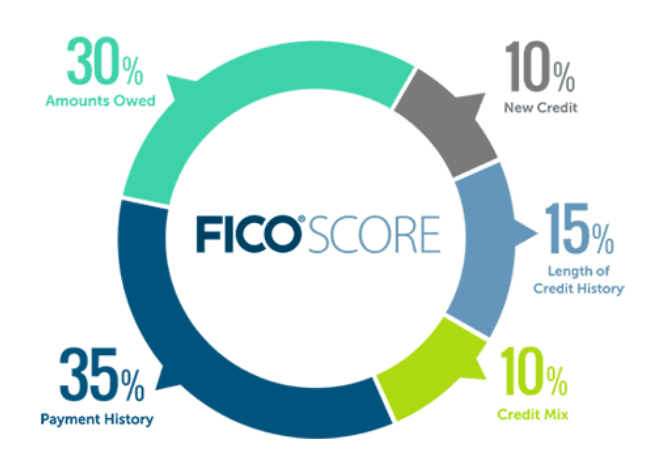

Your credit utilization ratio makes up about 30% of your credit score (below shown as “Amounts Owed”). So, if you want to effectively increase your score, consider focusing on your credit utilization rate.

In simple terms, your credit utilization ratio is the percentage of your available credit that you are using at any given time. If you have a credit limit of $1,000 and you’re carrying a balance of $500, your credit utilization ratio would be 50%.

In general, financial experts recommend keeping your credit utilization ratio under 30%. The higher your credit utilization, the riskier you are in lenders’ eyes. In contrast, if your credit utilization is low, it indicates to lenders that you have no problem managing your finances and additional debts.

Dispute errors on your credit report

There are a number of steps you can take to improve your credit score, and one of the most effective way is to dispute errors on your credit report. The three major credit bureaus are required to investigate any disputed items within 30 to 45 days. And if they find that the information is inaccurate, they must remove it from your report.

If you don’t have the time to search for errors, or worry you won’t know how to navigate the dispute process, credit repair companies can handle that work for you.

Pay bills on time

When you pay your bills on time, it shows creditors that you’re a responsible borrower and less likely to default on your loans. Paying your bills on time can also help you avoid late fees and other penalties, which can further damage your finances.

If you’re having difficulty keeping up with your bill payments, there are a few things you can do to make it easier.

- First, set up automatic payments so you never have to worry about missing a payment.

- You can also create a monthly budget to help you track your expenses and ensure that you have enough money to cover your bills.

- Finally, make sure to always pay at least the minimum amount due on each bill to avoid racking up more interest charges.

Limit applying for new accounts

Another way to improve your credit score is to limit the number of new credit accounts you open. Each time you apply for a new credit card or loan, lenders will do a hard inquiry on your credit report. Too many hard inquiries can lower your credit score and make it more difficult to open new lines of credit in the future.

Of course, there are some situations where you may need to do this, such as when you’re buying a car or a house. In these cases, before you apply try to shop around for the best rates and terms.

How long does it take to see changes in your credit scores?

How long it takes to see changes in your credit score will depend upon the behavior of each loan provider. For example, some creditors update credit information every 30 days, while others update it every 60 days. But in general, you should be able to see the updates reflected in your account anywhere from 30 to 60 days.

So if you just paid down your student loan debt or car payments, don’t expect to see your loan balance change immediately on your credit report.

Pro Tip

The Fair Credit Reporting Act (FCRA) allows all consumers to get a free credit report from each of the three major credit bureaus every 12 months. You can visit AnnualCreditReport.com to get your free credit report if you haven’t already.

FAQs

Can you open a bank account with a CPN?

No, you cannot use a CPN to open a bank account. It’s illegal, and you could end up in a lot of trouble with the federal government.

Can you go to jail for using a CPN?

Yes, you could potentially get locked away if you attempt to use CPN to improve your credit score or establish a new credit identity. Under federal law, lying on a credit or loan application and misrepresenting your Social Security number is considered a crime.

Can you get a new Social Security number?

If your poor credit is due to bad money habits, buying a CPN (illegal SSN) will only make the problem worse. However, if the following situations apply to you, the Internal Revenue Service (IRS) might issue you a new SSN:

- Sequential SSNs assigned to members of your family are causing problems

- You’re assigned the same SSN as someone else

- You’re a victim of identity theft

- You’re harassed, abused, or your life is in danger

- There are religious or cultural reasons to why you can’t use certain numbers or digits in the SSN

Even if the above mentioned situations apply to you, the process of getting a new SSN isn’t exactly hassle-free. You’ll have to provide extensive documentation to prove that obtaining a new SSN is necessary for your case.

Key Takeaways

- A CPN (credit protection number or credit privacy number) is a nine-digit identifying number that’s often illegally used in place of SSNs.

- Fraudulent companies market CPNs as a way to help consumers hide their bad credit history and apply for credit with a “clean slate.”

- Using a CPN on your credit or loan application is considered a federal crime. Doing so can leave you with a hefty fine and even jail time.

- Instead of illegally trying to improve your credit score, dedicate that energy to repairing your credit score with safe and effective methods.

- To raise your credit, make sure to pay your bills on time, limit the number of new accounts you apply for, lower your credit utilization ratio, and dispute errors on your credit report.

Get started rebuilding your credit

Having the opportunity to get a fresh start on your credit journey and erase all of the credit mistakes you’ve made sounds enticing. However, when something sounds like it’s too good to be true, it usually is. So, never attempt to change credit scores illegally or buy a CPN to replace your SSN. Doing so can put you in a worse financial situation and even get you into legal trouble.

If you suffer from bad credit and need help repairing your credit, consider seeking help from credit repair companies. Just make sure to do research beforehand and confirm that the company is reputable and reliable.

Share this post: