What is Debt Service?

EG

Last updated 03/15/2024 by

Erin GoblerSummary:

Your debt service shows how much you owe in a particular period. This differs from a debt service coverage ratio (DSCR), which determines how your total debt payments compare to your income. Debt service is important when qualifying for a loan, especially for a mortgage. Lenders use your debt service to calculate your DSCR, which is a key factor when determining loan eligibility.

When you’re applying for a loan, whether it’s for personal or business use, prospective lenders will want the full picture of your financial health. Two of the most important figures they’ll look at are your debt service and your debt service coverage ratio.

If you’re planning to apply for a loan soon or simply want to understand your financial health better, then debt service matters. Keep reading to learn more about what debt service is, why it’s important, and how to calculate your debt service ratio.

End Your Credit Card Debt Problems

Get a free consultation from a leading credit card debt expert.

It's quick, easy and won’t cost you anything.

What is debt service?

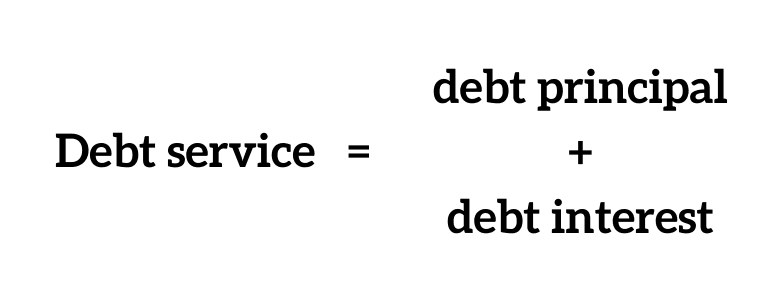

Debt service refers to the amount a borrower has to pay in a specific period in both interest and principal on a debt. It’s an important concept for anyone who borrowed — or is considering borrowing — money, whether it be student loans, credit cards, auto loans, or a mortgage.

A simpler way to explain debt service is that it’s your minimum payment for a given period. For example, if you have a student loan payment of $250 per month, your monthly debt service on that loan is $250. Your annual debt service on the same loan is $3,000. You can choose to pay more, but debt service refers to the amount you’re required to pay to meet your minimum debt obligations.

Just like debt service can refer to an individual’s debt obligations during a particular period, it’s also used by companies to calculate their debt payments. The concept is the same — a company’s debt service is the amount of interest and principal it must pay in a certain period. This number also helps determine a company’s ability to make payments and potentially take on additional debts.

How does the total debt service ratio differ?

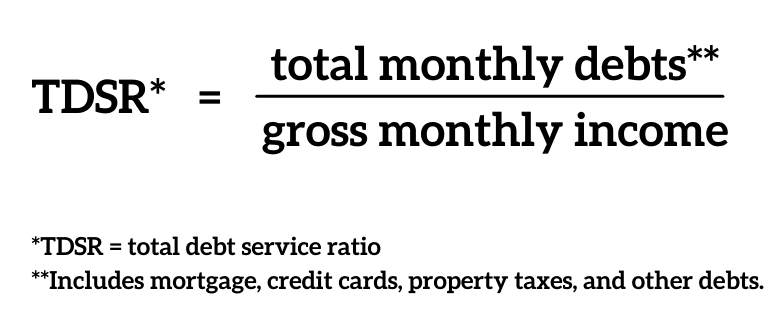

The total debt service ratio measures the percentage of someone’s annual income (or net operating income, in the case of a business) that’s required to cover their debt payments for the year.

Not only does your total debt service ratio tell you how much of your income will go toward debt in the coming year, but it’s also a tool used by lenders to determine eligibility for loans. Ideally, lenders want to see a small percentage of earnings dedicated to debts.

What is debt service capacity?

Debt service refers to the amount a company or individual owes in principal and interest payments over a particular period. On the other hand, debt service capacity refers to the amount they’re actually able to pay back. An individual or company’s debt service capacity should always exceed their actual debt service number.

What is a debt service coverage ratio (DSCR)?

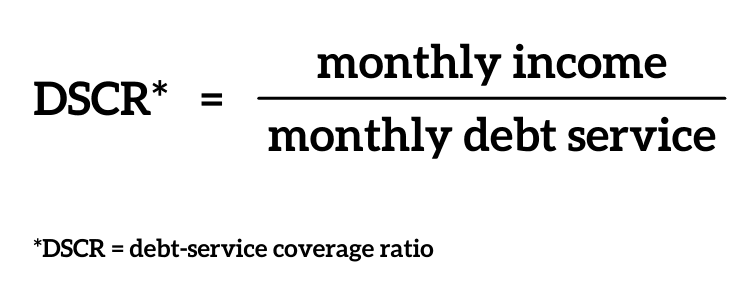

Debt service coverage ratio (DSCR) measures how much of your income goes toward minimum debt payments. It’s calculated by dividing your current income during a particular period by your debt payments for the same period. For example, someone with monthly debt payments of $500 and a monthly income of $2,500 would have a DSCR of 5.0.

IMPORTANT: You’ll generally want a DSCR of at least 1.0, though higher is better. A DSCR of at least 1.0 generally means you have positive cash flow. That being said, lenders generally prefer a DSCR of at least 1.25–1.5.

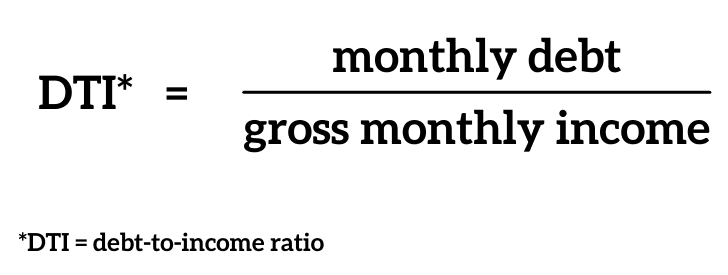

DSCR isn’t frequently used in personal finance but is more common when calculating a business’s debt obligations. When it comes to an individual’s financial picture, the more common calculation used is the debt-to-income ratio (DTI). Just like DSCR, it’s a calculation of how much of someone’s income goes toward debt.

Calculating DSCR and DTI

The major difference between DSCR and DTI, aside from how they’re used, is how they’re calculated. They both measure how much of a person or company’s incoming cash flow goes toward debt service.

However, while DSCR is found by dividing income by debt, DTI is found by dividing debt by income. So using our same example of someone with $500 of debt and $2,500 of income, their DTI would be 20%.

However, both DSCR and DTI are usually calculated using your gross annual income. This is your income before taxes and other deductions are taken out.

Debt service coverage ratio and your financing options

This may sound like too much math to care about, but it’s important information for your future. If you’re interested in finding a single-family home or townhouse to settle down in, estimating your DTI is the first step to getting a mortgage. The second step? Finding a lender. You can start that process with some of the lenders below.

Or maybe you’ve already gone through the process of getting a mortgage, and now your DTI is climbing. To bring down that percentage, consider refinancing your mortgage. This may help your DTI decrease and open other loan opportunities.

What is the difference between DSCR and debt service?

While they sound similar, your DSCR is not your debt service, and it can get a little confusing. Your debt service is simply the money necessary to pay your debt principal and interest for a period of time.

Your debt service coverage ratio calculates the borrower’s ability to repay the loan using the debt service. The DSCR takes into account the cash flow of a person or company to determine whether the borrower can afford additional debt.

Why is DSCR important?

It’s one thing to know what your debt service is and how to calculate your DSCR. However, it’s equally important to understand the role that debt service plays in your finances.

Your debt service coverage ratio is most important when it comes to qualifying for a loan, especially a mortgage. Lenders want to know that you’ll have plenty of money in your budget to make your monthly payments. And one of the best ways for them to determine this is by calculating the percentage of your income going toward debt.

When you’re applying for a mortgage loan, a mortgage lender will look at two different numbers. First, they’ll look at the debt service ratio on your prospective mortgage and what percentage of your income it would make up. They’ll also look at your total debt service, including the mortgage, to see how much of your income will go toward debt.

Ultimately, whether it’s for an individual or a business, the debt service ratio is one way of measuring financial health and whether someone is stretching themselves too thin with the debt they’ve taken on.

Your debt service ratio isn’t just relevant when it comes to qualifying for a mortgage or another type of loan, but it’s also a number to pay close attention to yourself. Ultimately, you want to make sure that your debt never becomes overwhelming, even if you face a financial setback.

Debt service ratio example

Let’s say you’ve decided to purchase your home and you want to make sure you can qualify for a mortgage. You’re planning to finance a home valued at $300,000 with a 10% down payment (or $30,000).

Based on your credit score and the current market interest rates, you learn that you could get a rate of 4% on a 30-year fixed-rate loan. If you pay $120 per month for homeowners insurance and $500 per month for property taxes, then your monthly payment would be $1,909.

But to ensure you’ll actually qualify for the loan, you want to calculate your debt service ratio.

First, the debt service on your new mortgage would be $1,909 per month, which comes to $22,908 per year. If you have a gross income of $90,000 per year, then your DSCR on your mortgage is 3.93, which is considered in the healthy range. Your DTI would be 25%.

But when it comes to qualifying for a mortgage, it’s far more than just the debt service on your mortgage that matters. Lenders look at your entire debt picture to see how your mortgage would fit into it.

Let’s say you also have a student loan with a minimum monthly payment of $250 and an auto loan with a minimum monthly payment of $325.

When you add in those debts, your total monthly debt obligations come to $2,484, for an annual debt service of $29,808. Based on your annual income, your total DSCR is 3.02, while your DTI would be 33%.

When qualifying for a mortgage, most lenders look at your DTI instead of your DSCR. The good news is that you can usually qualify for a mortgage with a DTI of 43% (though some lenders allow up to 50%).

That being said, many financial experts recommend a DTI of 36% or lower to buy a home. So in our example, you would be in great shape with your DTI of 33%.

EG

Erin Gobler is a Wisconsin-based personal finance writer with experience writing about mortgages, investing, taxes, personal loans, and insurance. Her work has been published in major outlets, such as SuperMoney, Fox Business, and Time.com.

Share this post: