What Is Interest Income?

CS

Summary:

Interest income is the income you earn from depositing money in savings programs, buying certificates of deposit (CDs) investing in bonds, or lending your money. In most cases, interest income is taxable and should be reported on your tax return.

You can earn income interest through a form of investment, but this doesn’t just mean money coming from stocks. Income interest includes money coming from your untouched savings account as well. While this is an easy way to get interest income, there are a few more ways that people aren’t aware of.

Keep reading to learn some low-risk ways to build interest, and how to report it on your tax return.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is interest income?

Interest income is the money you earn from lending money. This does now just include regular loans but also the mone you make when “lend” money to institutions by buying bonds or investing in deposit accounts, such as CDs, money market accounts, and savings accounts. You may also hear a similar banking term “net interest income.” Net interest income refers to a company’s revenue from interest-bearing assets minus any expenses related to paying for its interest-bearing liabilities.

One way you’ve probably already received interest income is through your savings account. Depositing and leaving money untouched in a savings account will accumulate interest over time through a system called fractional banking.

What is the difference between interest earned, paid, and expense?

After you make an investment, the interest you eventually earn passes through a few stages before reaching your bank account.

- Interest earned. This refers to the interest an investment will earn over the course of the investment.

- Interest accrued is practically the same thing as earned interest. However, it’s sometimes used to differentiate interest you earned and is accessible to you in your account and money you are earning but that you have not collected yet. For example, in a savings account you may accrue interest every day but the money isn’t deposited into your account until the end of the month.

- Interest paid. This is interest gained as a payment into your account.

- Interest expense. This is the cost of borrowing money from lenders, bond investors, and other financial institutions.

Let’s say you have $10,000 into an investment that earns 5% interest each year. At the end of the year, your investment’s earned interest is $500. Once the $500 enters your bank account, it becomes interest paid.

On the other hand, maybe you kept $10,000 in your savings account. Over the course of several weeks, your account accrues interest. At the end of the month, the money earned from interest is deposited into your account, where it becomes interest paid.

How can I earn interest income?

Earning interest income may sound restricted to business or finance professionals, but this isn’t the case. You can earn interest income through any of the below options.

1.) Certificates of deposit (CD)

When you open a certificate of deposit, you agree to leave money in the deposit for a certain amount of time. For example, if you open a six-month CD, you will leave a set amount of money in there for six months. Withdrawing that money before six months can result in a financial penalty.

A CD has a fixed income rate, so you receive the same rate regardless of changes in the market. You don’t have as much flexibility with withdrawing money with a CD. The benefit, however, is that it usually has a higher interest rate than a normal savings account.

2.) Online checking and savings account

A simple way to earn interest income is by opening an online checking or savings account, and there are a few benefits to it.

First, many online banks have higher interest rates because they have lower fixed costs. Second, a lot of online financial institutions omit servicing fees. So not only will you have a higher interest income, but you also can save some money by not paying servicing fees.

You can also look specifically for high-interest checking accounts to help gain more interest.

3.) Money market account

Money market accounts have higher interest rates and allow you to withdraw money frequently. However, the fees and minimum balance requirements are higher than savings accounts. Also, be aware that the interest rates on money market accounts may not be much higher than a savings account.

4.) Buy bonds

Buying a bond is essentially lending money to a large organization or company. At the end of the term, you get your money back along with any interest income. There are three types of bonds you can invest in: corporate bonds, municipal bonds, or treasury bonds. Each bond has its own interest rates and compensation period.

Companies issue corporate bonds. They tend to have the highest risk, but also the highest reward. State, cities, and countries may issue municipal bonds. The U.S. Department of Treasury, on the other hand, issue Treasury bonds. This is usually the safest and most common bond investment.

While bonds are risky, some view them as less risky than stocks. You also do not have access to your money before the maturity date.

What is CD or bond laddering?

For those looking to have more flexibility when withdrawing money, you can still receive the high-interest rates of CDs or investment benefits of bonds through laddering. Laddering refers to an investment strategy where you invest in multiple CDs or bonds with different end or maturity dates.

For example, you may open three CDs and put a small sum in each. One ends in January, one ends in February, and the third ends in March. Each has a high-interest income and you’re still able to withdraw money at the end of the month.

Can lenders earn interest income?

Actually yes. When you make payments on a loan, that payment includes both the regular monthly rate and the interest rate. This is true of commercial real estate loans, personal loans, and auto loans. That interest portion is then included as part of the lending institution’s interest income.

How to calculate interest income

You can calculate how much interest you made three simple steps:

- Convert your annual interest rate from a percentage to a decimal figure. This can be done by dividing the percentage by 100.

- Multiply the decimal figure by the number of years the money was borrowed.

- Take that number and multiply it by how much is in your account.

Example:

George has $7,000 in his account with a 2% interest rate. He divides this by 100 and gets 0.02. The money was borrowed for 2 years, so he multiplies 0.02 by 2. This equals 0.04. George multiplies 0.04 with 7,000. This means he earned $280 in interest income over those two years.

How to report interest income

The Internal Revenue Service considers interest income to be taxable income in most cases. Municipal bonds and personal activity bonds are free from federal income tax. More tax-exempt interest examples can be found on the IRS website. Make sure to report all interest income on your tax return.

- Savings bonds interest

- Interest from treasury bills, notes, and bonds

- Interest on most accounts, including bank accounts, money market accounts, CDs, corporate bonds, and deposited insurance dividends

Pro Tip

A full list of taxable interest can be found on the IRS website. Be sure to report any of these that apply to you on your federal income tax return.

If you’re not comfortable with determining your taxable interest, tax preparation software may be able to help. Compare user reviews and software features before making your decision to ensure you find the best help.

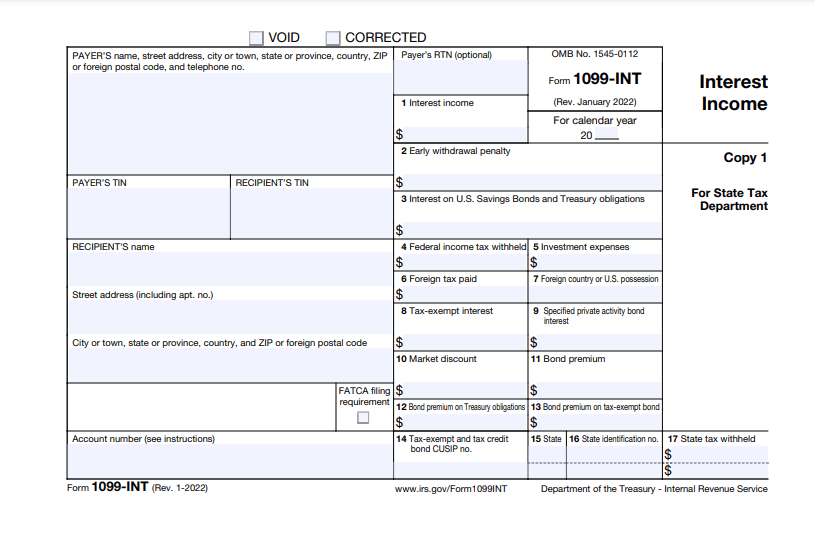

What is form 1099-INT?

You will fill out form 1099-INT to report interest income on your tax return. Here is a simplified version of what the first ten boxes mean on this form:

- Income interest. Enter the total taxable interest amount earned. Be sure to review what the IRS considers taxable interest income. You may want to fill out Box 3 before you fill out Box 1, as you list some specific income interests there, too.

- Early withdrawal penalty. If you withdrew your money from a CD before the maturity time was up, you receive a withdrawal penalty. Put the total amount of that here.

- Interest on U.S. Savings Bonds and Treasury Obligations. List any interest earned from a U.S. Savings Bond, Treasury bills, Treasury notes, or Treasury bonds.

- Federal income tax withheld. Write any backup withholding you have, if applicable.

- Investment expenses. This is only for deductible expenses applicable to single-class real estate mortgage investment conduits (REMIC).

- Foreign tax paid. Write the total amount of foreign taxes paid on interest in U.S. dollars.

- Foreign country or U.S. possession. Enter the foreign country referenced in Box 6.

- Tax-exempt interest. The total amount of any interest earned that is tax-exempt. Tax-exempt income could be municipal bonds or personal activity bonds.

- Specified private activity bond interest. The total amount of accrued interest from any private activity bond.

- Market discount. If you received a market discount on a debt, enter the total amount here.

Remember, you can always enlist the help of tax preparation software if you struggle with these forms.

Key Takeaways

- Interest income is the money you earn from lending money. This includes the money you “lend” when you buy bonds or invest in deposit accounts, such as CDs, money market accounts, and savings accounts.

- Net interest income is a different term that describes a company’s revenue from interest-bearing assets minus any expenses related to paying for its interest-bearing liabilities.

- Just like most other types of income, interest income is typically taxable.

- Report your interest income on form 1099-INT on your tax return.

CS

Camilla has a background in journalism and business communications. She specializes in writing complex information in understandable ways. She has written on a variety of topics including money, science, personal finance, politics, and more. Her work has been published in the HuffPost, KSL.com, Deseret News, and more.

Share this post: