What Is The 10/20 Rule Of Thumb?

LS

Summary:

The 10/20 rule, more commonly known as the 20/10 rule, is a rule of thumb to help consumers determine how much consumer debt is “too much.” The “rule” states that your debt should equal no more than 20% of your annual net income (not counting mortgage debt). The “10” indicates that only 10% of your monthly after-tax income should go toward paying those debts. It’s a useful standard, but it doesn’t take into account your overall financial picture.

As you try to understand your financial situation, it’s confusing to know where you are on the spectrum. You don’t want your expenses to outweigh your income, but it can be tricky to determine how much is “too much” when it comes to debt. Rules of thumb like the 10/20 rule can help.

One way to look at your entire financial picture is to examine your debt to income ratio. We’re Americans—we “all” have debt. In fact, U.S. households have over $15 trillion dollars in debt as of November 2021, according to the Federal Reserve Bank of New York’s Center for Microeconomic Data.

Fortunately, we have multiple strategies to help you manage your portion of this debt. In this article, we’ll discuss what the 20/10 rule is, how you can use it to plan your debt payments, and how this “rule” can help you reach your personal finance goals.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What’s the purpose of the 20/10 rule?

The point of the 20/10 rule of thumb is to get a handle on your debt (minus mortgage payments) in relation to your annual and monthly take-home pay. In other words, it’s designed to help you avoid getting into more debt than you can afford.

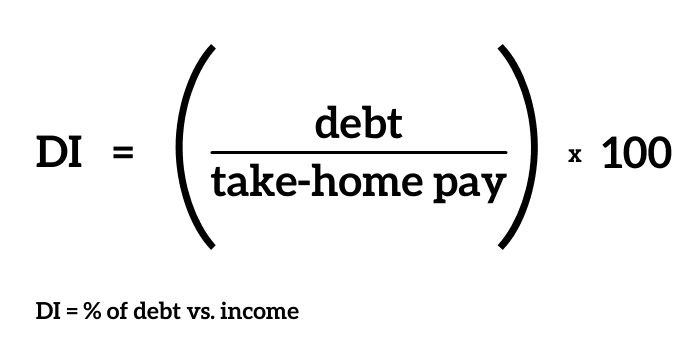

For the 20% part of the equation, you’ll want to calculate if your consumer debt (credit cards, car loans, student loans, etc.) exceeds 20% of your annual after-tax income.

Example:

Let’s say you take home $50,000 a year after taxes. You have a car loan balance of $10,000, owe $5,000 to your student loans, and have $2,000 in credit card debt. That’s a total debt of $17,000, which, when you divide that sum by net income, means your debt is 34% of your yearly take-home pay.

Not great by the standards of the rule (ideally you would have no more than $10,000 at that income level), but not terrible. This tells you it’s time to make some changes to pay off some of those bills.

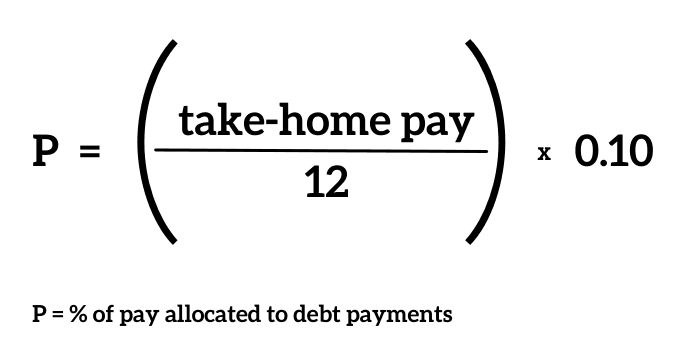

Looking at the 10% portion of the rule, you want to use 10% or less of your monthly take-home funds for debt payments.

Let’s go back to the above example. If you’re bringing home $50,000 a year, divide that by the 12 months in a year, and you get $4,167, which is your net monthly income. Of that number, you should ideally only spend about $417 per month on monthly debt payments.

Is the 20/10 rule realistic?

It’s a great benchmark, but it doesn’t necessarily work for everyone. Maybe you came to this concept later in life and now wonder if it’s too late. It’s never too late to start on the path to financial health. The rule tends to come from the standpoint that you’re already in good financial standing, but that’s not realistic for many people.

For example, the model can feel particularly troublesome for individuals with student loan debt. Say you got a job right out of college and have an annual after-tax income of $30,000. You owe $5,000 on your car and have a balance of $1,000 on a credit card.

By the 20/10 rule, you’re in excellent shape at 20% on the dot. Then six months later, $20,000 in student loans come due, and suddenly the model is blown up. Now you’re at about 86% debt. Yikes. All you can do is try to work on that debt repayment before borrowing more.

Pro Tip

Remember that this is just a “rule of thumb,” not a hard and fast rule. Many people go way over this ratio and are just fine. Real estate investors are a good example; they borrow a lot to make a lot.

More important than absolute numbers is how you manage your debt. If you use common sense and stay in good standing with your accounts, you’re probably in the right place even if you don’t exactly hit those numbers. If, however, you’re having trouble managing your debt, it’s time to take a closer look at your personal finances and make some changes.

The 10/20 rule and lenders

Although lenders review your debt-to-income ratio, they typically don’t use the 10/20 rule. Instead, lenders often only consider borrowers with a debt-to-income ratio at or below 36%. However, some lenders will still consider borrowers with a higher ratio.

What about the rest of my spending?

While the 20/10 rule provides some guidance on your debts and income, it doesn’t consider your other spending habits. This is where the 70/20/10 financial model takes the equation a step further, which can be useful in planning your total budget.

The 70/20/10 rule

This rule—maybe “suggestion” is better—suggests that 70% of your monthly net income should be allotted for the necessities to live. In addition to necessities, this 70% includes things you want but don’t need to survive. That then leaves 20% to go toward savings and the final 10% for monthly payments to your consumer debt.

The 70% is broken down by your needs, which include mortgage or rent, utilities, food, and insurance. After necessities come your wants, such as dining out, gym memberships, streaming services, new clothes, etc.

The model recommends that the next 20% of your monthly income gets allotted for savings. This could be money put into an emergency fund (the standard advice on that is to have at least three months’ pay socked away), retirement accounts, or any other savings goals you might have.

Then, reserve the final 10% left over from your paycheck for monthly payments of your consumer debts, just as the 20/10 rule also suggests.

How about the 50/20/30 rule?

Another financial tool is the 50/20/30 budget model. This model was first proposed by Senator Elizabeth Warren in her 2005 book All Your Worth: The Ultimate Lifetime Money Plan. The rule suggests that 50% of your monthly budget is for living expenses and needs. Of the remaining funds, 20% goes toward debt and savings and the final 30% is to be spent on whatever you want.

- Needs. This includes money spent on rent, food, utilities, transportation, insurance, and minimum debt payments. Whatever is the lowest payment you can get away with on your credit card balance, for example, is categorized as a need in this budget model.

- Debts and savings. When you’re figuring out how to allocate that 20% of your monthly income, along with adding to your retirement accounts and emergency fund, you also want to factor in what additional money could go toward your debts. How much debt you have and your long-term goals will impact your decision making.

- Fun money. Finally, the Warren model allows for 30% of your income to be spent on things you want—fancy new shoes, books, restaurants, or a trip to a museum, for instance.

How does this differ from the 30/30/3 rule?

This budget model focuses specifically on home mortgages. Recently developed by Sam Dogen (owner of Financial Samurai), this budgeting strategy breaks down how to afford a home mortgage without breaking the bank.

Using this idea, Dogen suggests that only 30% of your monthly income should go towards your mortgage payment. Over time, you save up another 30% of the home’s value through both savings, cash, and investments. With this much in savings, you can use 20% for the down payment and the remaining 10% as a buffer.

The final “3” represents the maximum home price you can afford, which you can do by multiplying your annual gross income by three. Let’s say you make $50,000 a year. Then you shouldn’t look for a home with a sticker price above $150,000.

Pro Tip

In the interest of your financial future, you might want to use that 20% to tackle your high-interest debt, such as credit cards. Then consider adding to your monthly car payments or even spending money on extra mortgage payments.

Which model is right for me?

There are a lot of ways to get yourself out of debt and save money in the process. The first step is to take an honest look at your finances and analyze (possibly with the help of a professional) the best way to reach your goals.

With that being said, you don’t have to pick just one model—feel free to adapt the pieces that make sense to you. As mentioned before, look at these financial or budgeting models as guidelines on how to manage your debt in relation to the rest of your budget. However, be sure to do this while keeping your financial goals in mind.

The path to financial freedom

If you feel overwhelmed by your debts and figuring out your budget, make some changes to reach those financial goals.

Talking to a debt counselor is one option. They might advise things like consolidating loans or credit cards, moving to a less expensive apartment, or spending less on clothes and entertainment.

Taking a step further in analyzing your finances, you might look at the fine line between wants and needs. For instance, maybe you want a new car, but you don’t really need one. Or, if you live in a city with great public transportation, you might not need a car at all. Getting rid of that expense will save you a ton on car insurance, monthly payments, gas, and routine maintenance.

Key Takeaways

- The 20/10 rule recommends having debt equal to 20% or less of your after-tax income, with no more than 10% of your monthly paycheck being used to pay it back.

- If you need to get a little deeper into your finances, you can use the 70/20/10 rule. This rule suggests, after taxes, that 70% of your check is spent on wants and needs, 20% on savings, and 10% on paying back consumer debt.

- The 50/20/30 model says you spend 50% of your money on living expenses, 20% on debt and savings, and 30% on whatever you want.

- These aren’t hard and fast rules—they’re guides on how to manage your bills.

- If you feel overwhelmed by your finances, talking to a counselor or consolidating your debt are ways to get back on track.

Share this post: