Why Successful People Achieve Their Financial Goals And You Don’t!

TG

Last updated 04/09/2024 by

Tania GallowayWell, here we are, starting another new year! It’s the time of year when we’re all inspired to work on improving our health, lifestyle, and finances once again. We renew our commitment to betterment in general and promise ourselves that this is the year we make it happen. Then, usually by about February or so, most of us forget all about the determination we felt on January 1st and quietly fall back into our old habits.

Do successful people do different things? What is it that you always miss your goals and they do?

It doesn’t need to be that way. There is a science behind making realistic, attainable goals and achieving them. By following these simple steps, you can ensure that you meet all your financial expectations and more!

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

1. Take Baby Steps

When it comes to financial goals, the key to success is simplicity. Personal finance can be daunting, but it doesn’t need to be complicated. Keep your financial goals straight forward and focus on the basics. I know it’s tempting to make resolutions in January that cover the coming calendar year but break it down into smaller, tiered goals. Why not make monthly or quarterly goals instead of annual ones?

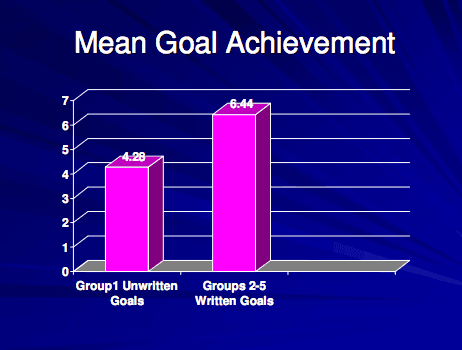

2. Write It Down

By committing your goals to paper, you vastly increase your chances of achieving the goal. A study done at Dominican University showed that a group who wrote their goals down was almost 50% more likely to achieve them than a group who only thought about the goals they wanted to achieve.

3. Connect With Your Goals Emotionally

You have to really, really want to achieve your goals. In other words, you aren’t likely to find the motivation to power through or make sacrifices to achieve a goal if it’s not deeply, personally important to you. A worthwhile exercise is to take the list of goals you’ve written down and write down at least one emotional reason for each, explaining why you MUST achieve it. By doing this, you’ll ensure that the goals are actually your own and not just things you feel you should do to please someone else or conform to social conventions.

4. Make Goals Specific And Measurable

The vaguer a goal is, the easier it is to lose your focus, get sidetracked, or lose sight of it entirely. A specifically worded goal that has milestones or is easily measurable is definitely the way to go. For example, a vague goal would be to “pay down your credit card”, but a specific and measurable goal would be to “pay your specific credit card to $0 by September 1st by making regular monthly payments of $450 without accruing any additional debt on it along the way”.

5. Be Realistic

The surest way to doom a financial goal is to pull it out of thin air. Finances are a numbers game, based on actual money flowing in and out of your account. Therefore, any financial goal needs to work within your budget. The goal above, to pay down the credit card, for example, would only be attainable if you’d gone through the exercise of making sure you had the $450 available in your budget on a monthly basis to make the payments.

6. Keep Yourself Accountable

Peer pressure and your own sense of pride are amazing forces to be reckoned with. It’s very easy to let yourself off the hook on a goal if no one else knows about it. Keeping yourself accountable to others is a great way to pressure yourself into achieving it, no matter what. Find yourself a budgeting buddy or an online group of strangers to whom you report your goals, timelines, and results.

7. Get Everyone On Board

If you have a significant other, it’s very important to make financial goals a family affair. Come up with the goals together, making sure that everyone feels emotionally attached to success and get everyone’s buy-in on the methods for achieving the goals. Even the kids can be brought on board. After all, they may be asked to make sacrifices for the general good of the budget as well.

8. Give Yourself Deadlines

Again, in the interest of making specific and measurable goals, don’t just throw a goal against the wall and hope it sticks. Instead, make a hard deadline for the achievement of it. Or break it down into measurable chunks with each piece having a specific end date. Then, mark those dates on the calendar and check in on your progress frequently.

9. Track Your Progress

Play games with yourself and make it as fun as possible. Instead of tracking results on a boring spreadsheet, why not have a color-in chart or a sticker board you fill-up? Saving for a vacation? Why not draw a palm tree in sections and color it in as your bank account grows?

10. Adjust Goals As You Go

Making the goal is only the first step. After that, you must not only track your progress against it but also tweak it as you go along. Nothing is more discouraging than falling behind on a goal or feeling like it’s an impossibility. If you realize that a goal was less than realistic, scale it back a bit, change the deadline, reduce the number, make whatever change is necessary so that it becomes achievable. Remember, achieving part of your original goal is still better than giving up and not achieving any part of it at all.

11. Challenge Yourself

By contrast, if you notice that your original goal was easier than you thought to achieve, up the ante. Don’t make goals so easy that you get complacent about your money. Get yourself excited about achieving more than you thought was possible. Why not take last year’s goals that were achieved and add 10% to each number?

Why not challenge yourself to find additional sources of income or additional potential savings in your expenses?

Share this post: