How To Get Late Payments Removed From Your Credit Report

JA

Summary:

Late payments can have a significant impact on your credit score. A single late payment can drop your score by over 50 points, and if you constantly miss payments, your score could plummet even further. This negative record can also stain your credit report for up to seven years. Fortunately, you might be able to remove late payments from your credit report if they were inaccurately reported or if there were unique circumstances that contributed to the late payment.

When you’re applying for a loan, the last thing you want is for your lender to take one look at your credit history and immediately write you off as a risky borrower. Unfortunately, that’s often what happens when you have a history of late payments.

According to FICO data, a 30-day late payment can cause a very good credit score (between 740 and 799) to drop 63 to 83 points. Thankfully, though late payments can seriously damage your credit score, it’s not impossible to remove them from your credit report.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How to remove accurate late payments

Sometimes, life happens. You might have had a period of unemployment or an unexpected medical emergency that caused you to fall behind on your bills. While late payments can have a significant impact on your credit score, there is some good news. You can remove an accurately reported late payment from your credit report by writing a goodwill letter to your creditor.

In the letter, explain the circumstances that led to the late payments and request that they be removed. Be sure to include any documentation that supports your claim. The more, the better. And while creditors aren’t obligated to remove your late payments, it’s worth a shot.

Here are some circumstances where a lender might be willing to remove your late payment information:

- You missed a payment due to hardships like experiencing a natural disaster, a global pandemic, or a hospitalization.

- The late payment was due to the fault of others. For example, your bank or credit card company made an error.

- You’ve always made payments on time, and this late payment was a one-time mistake.

How to remove inaccurate late payments

If you have an incorrect late payment record on your credit report, don’t panic. You can get this negative information removed from your credit history by taking the steps below.

1. Dispute the negative account information with the credit bureau

If you have late payments on your credit report that are inaccurate, you can file a dispute with the credit bureaus to have them removed. Each credit bureau has a slightly different dispute process, so head to each of their online dispute centers for how to start a dispute.

Generally, you can initiate a dispute by phone, online, or by mail. Once the credit bureau receives your dispute, they will have around 30 to 45 days to investigate and determine whether or not to remove the late payment from your report. If they find that the late payment is inaccurate, it will be removed.

Pro Tip

You’re entitled to one free credit report from each of the three credit bureaus every year. If you haven’t already, head to AnnualCreditReport.com to request copies of your credit reports so you know where you stand in terms of your credit health.

2. Hire a credit help company

Disputing credit report errors can be time-consuming and frustrating, especially since you have to contact all the credit bureaus. The process can feel never-ending if you have several inaccurate negative items on your report. Fortunately, there is another option: hire a credit help (aka credit repair) company.

Credit repair companies will work with the credit bureaus on your behalf to get the inaccurate information removed. While hiring a credit help company can save you the hassle of filing disputes and repairing credit yourself, it’s important to be careful. Make sure to read the fine print before signing any contracts. And don’t forget to watch out for red flags, such as a company that asks for a huge sum of money upfront before they provide any services.

You can ensure you choose the right credit repair company by comparing all of your available options. Start by reviewing the companies below.

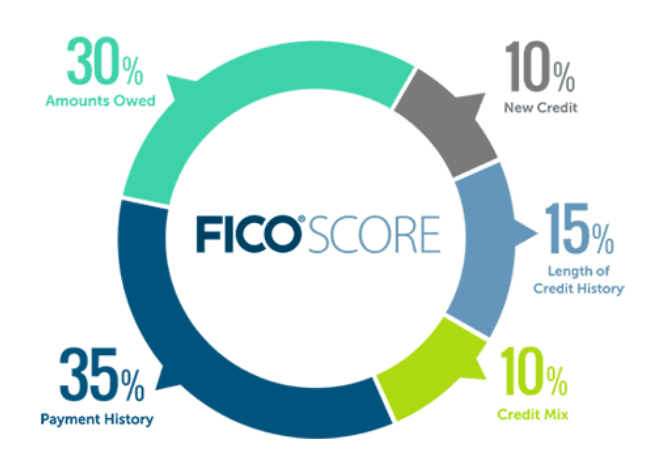

How late payments affect your creditworthiness

According to Experian, one of the three major consumer credit bureaus, your payment history accounts for 35% of your credit score. In other words, lenders care the most about your record of paying back debts, as you can see from the chart below.

If you’ve missed several payments in the past, lenders may see you as a risky borrower and may be reluctant to extend new credit to you. On the other hand, if you have a long history of timely payments, lenders may view you as a low-risk borrower and may be more willing to offer you favorable terms.

Ways to rebuild your credit scores

Having a poor credit score isn’t all doom and gloom. You still have a chance to rebuild your credit score and improve your financial future. Here are some ways to do so:

- Make all of your payments on time. Your payment history is the most important factor in determining your credit score. So the simplest and most effective way to improve your credit score is by paying your bills on time. Sign up for automatic bill payments if you struggle to remember due dates.

- Keep your credit utilization low. Even if you’re making all of your payments on time, carrying a high balance on your credit cards can hurt your score. Try to keep your balances below 30% of your credit limit.

- Use a mix of different types of credit. Your credit mix accounts for 10% of your credit score. Different types of credit, such as personal installment loans and revolving lines of credit, can positively impact your score since it shows lenders that you can manage different types of debt responsibly.

- Check for errors on your credit report. Sometimes mistakes happen, and incorrect information can appear on your report. So make sure to routinely check your credit report. If you spot an error, dispute it with the credit bureau to correct it.

IMPORTANT! Keep in mind that fixing your credit score is not an overnight process. It takes time and effort to make lasting changes to your credit history.

FAQs

How long does it take for a late payment to be removed from a credit report?

Most late payments will remain on your credit report for up to seven years and damage your credit score. If you have several late payments, it may take a few years for your score to recover. However, by staying on top of your payments and maintaining good financial habits, you can eventually reestablish yourself as a low-risk borrower.

Can you have a 700 credit score with late payments?

Yes, it’s possible to have a good credit score even if you’ve made some late payments in the past. That’s because your credit score is based on your credit history, which includes information on both your positive and negative payment habits.

So, even if you’ve had a few late payments, as long as you’ve also been consistent with making on-time payments, you can still have a good credit score.

Can credit repair remove late payments?

Credit repair companies can’t magically erase accurate late payments. However, they can help dispute inaccurate negative items on your behalf.

This process involves sending a request to the credit bureau asking them to investigate the late payment in question. If the bureau finds that the late payment is inaccurate, they will remove it from your report.

Is it true that after seven years your credit is clear?

According to the Fair Credit Reporting Act (FCRA), negative information generally falls off your credit report after seven years. This includes things like late payments and charge-offs. However, there are some exceptions. Certain types of negative information, such as bankruptcies, can stay on your credit report for up to 10 years.

So while it is true that most negative information will fall off your credit report after seven years, there are some exceptions you should be aware of.

How far back do lenders look at late payments?

Depending on the lender, they may only consider your late payments within the last 12 months. However, others may go all the way back to two years ago.

Remember, most lenders will also assess the number of missed payments you’ve had in total. This means that even if your late payments are from a while ago, if you’ve had a lot of them, it could still impact your chances of getting a loan.

How long does it take to build credit from 500 to 700?

The time it takes to build your credit from 500 to 700 can range from a few months to a few years. This timeline will largely depend on factors such as how many accounts you open, how much you use your credit, and whether you make your payments on time.

Keep in mind that if you have serious negative account information on your credit report, such as bankruptcy, you’ll have a much more difficult time building your credit back up.

How long does a 120-day late payment stay on credit report?

The short answer is up to seven years. When you miss a payment on your credit card, mortgage, or any other type of loan, it can have a major impact on your credit score. Your creditor will report the late payment to the credit bureaus, and this negative mark will stay on your credit report for up to seven years.

The longer the payment is overdue, the more damage it will do to your score. So if you’re falling behind on your payments, it’s important to get caught up as soon as possible.

Key Takeaways

- If you have an accurately reported late payment, you can try removing it from your credit report by writing a goodwill letter to your creditor.

- If you find inaccurate late payment information on your credit report, file a dispute with the credit bureau or hire a credit repair company to do so on your behalf.

- Late payments can stay on your credit report for up to seven years and damage your score.

- You can improve your credit score by making all of your payments on time, keeping credit utilization low, using different types of credit responsibly, and routinely checking for errors on your credit report.

Keep an eye out for credit score changes

Even though late payments can hurt your credit score, there are ways to mitigate the damage. But once you repair your credit score, it’s important to maintain that score as best as you can. So how can you keep an eye on your score while improving your credit?

One of the best ways to maintain your score, in addition to the steps we discussed above, is to use a credit monitoring company. With their help, you’ll receive alerts to movements in your credit score. On the other hand, if you need help knowing where to start fixing your credit, reach out to a credit counseling company as well.

Share this post: