Going Back To College Later In Life: Is It Worth It?

TG

Last updated 03/21/2024 by

Tania GallowayHave you hit a career slump? If so, it may be time for a major change. Maybe this means becoming more qualified or specialized in your current field, but you may even be considering going back to college to earn a new degree. But is it too late? Is there a point in life where the investment of time and money into college just doesn’t pay off?

How much does a college degree cost?

How much does a college degree cost?

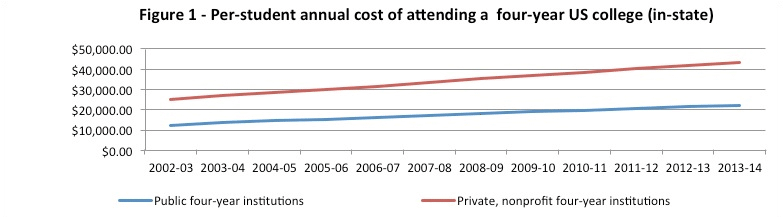

In order to begin assessing if returning to college is a worthwhile exercise, you have to be able to calculate the real cost of that college education, beginning, of course, with the obvious expenses such as tuition, books, transportation, etc. Assuming you’ll be attending a college in your home state, so no move will be necessary and you’ll benefit from the “in-state resident” tuition cost, the latest statistics suggest that the average cost of a four year college degree in the United States will be about $45,000 per year at a private college and $20,000 per year at a public college.

Now, if you’re getting this education at a later point in life, you also have to account for the loss of income you’ll suffer in order to drop what you’re doing to return to full-time studies. Obviously, I can’t begin to know what that number is, so suffice it to say that you’ll have to consider not only the loss of your current salary, but also whether or not you have the money put aside to pay for that education up front, including supplementing the household cash flow for the four years that you’ll be in school.

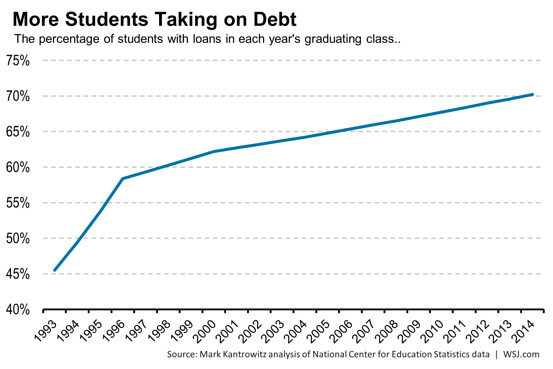

Now, if you’re getting this education at a later point in life, you also have to account for the loss of income you’ll suffer in order to drop what you’re doing to return to full-time studies. Obviously, I can’t begin to know what that number is, so suffice it to say that you’ll have to consider not only the loss of your current salary, but also whether or not you have the money put aside to pay for that education up front, including supplementing the household cash flow for the four years that you’ll be in school. In a perfect world, you would have seen this change coming and saved up to have all your bases covered, but let’s get real…more likely that you’ll either have to make some major lifestyle changes for the next four years, or accept that you’ll be accumulating some debt to make this new career happen. It’s very likely in this scenario, you’ll have to account for the cost of a student loan.

In a perfect world, you would have seen this change coming and saved up to have all your bases covered, but let’s get real…more likely that you’ll either have to make some major lifestyle changes for the next four years, or accept that you’ll be accumulating some debt to make this new career happen. It’s very likely in this scenario, you’ll have to account for the cost of a student loan.How long will it take to pay off your student loans?

Assuming you’re getting an average four year education at a cost of approximately $20,000 per year, the initial amount of your student loan would be about $80,000. Usually, you can defer making any payments until after graduation and student loans are usually charged an interest rate of about 5 to 6%. This means that the amount you’ll end up paying back on that loan will be more than $100,000, including the interest. So, once you’ve graduated, you’ll have a monthly payment to make for the next 10, 15, 20, or 25 years, depending on the loan you’ve taken out. You can use this awesome student loan calculator to see not only what your monthly payments would be, but what salary you would have to be making in order to comfortably make those payments.

Assuming you’re getting an average four year education at a cost of approximately $20,000 per year, the initial amount of your student loan would be about $80,000. Usually, you can defer making any payments until after graduation and student loans are usually charged an interest rate of about 5 to 6%. This means that the amount you’ll end up paying back on that loan will be more than $100,000, including the interest. So, once you’ve graduated, you’ll have a monthly payment to make for the next 10, 15, 20, or 25 years, depending on the loan you’ve taken out. You can use this awesome student loan calculator to see not only what your monthly payments would be, but what salary you would have to be making in order to comfortably make those payments.As an example, the monthly payment on an $80,000 loan at 5% interest, amortized over 10 years, would be $848 and you would have to be earning $101,000 a year in order to comfortably allot 10% of your salary to your loan repayment efforts. Stretching that loan out to a 20 year amortization gives you a bit more wiggle room, with a monthly payment of $527, requiring a salary of $63,000.

How much money will you make?

So far, this all seems very daunting, but keep in mind that the whole point of the exercise is to have a higher earning potential once you’ve graduated. So, what’s the reality on how much money you’ll earn with that degree?

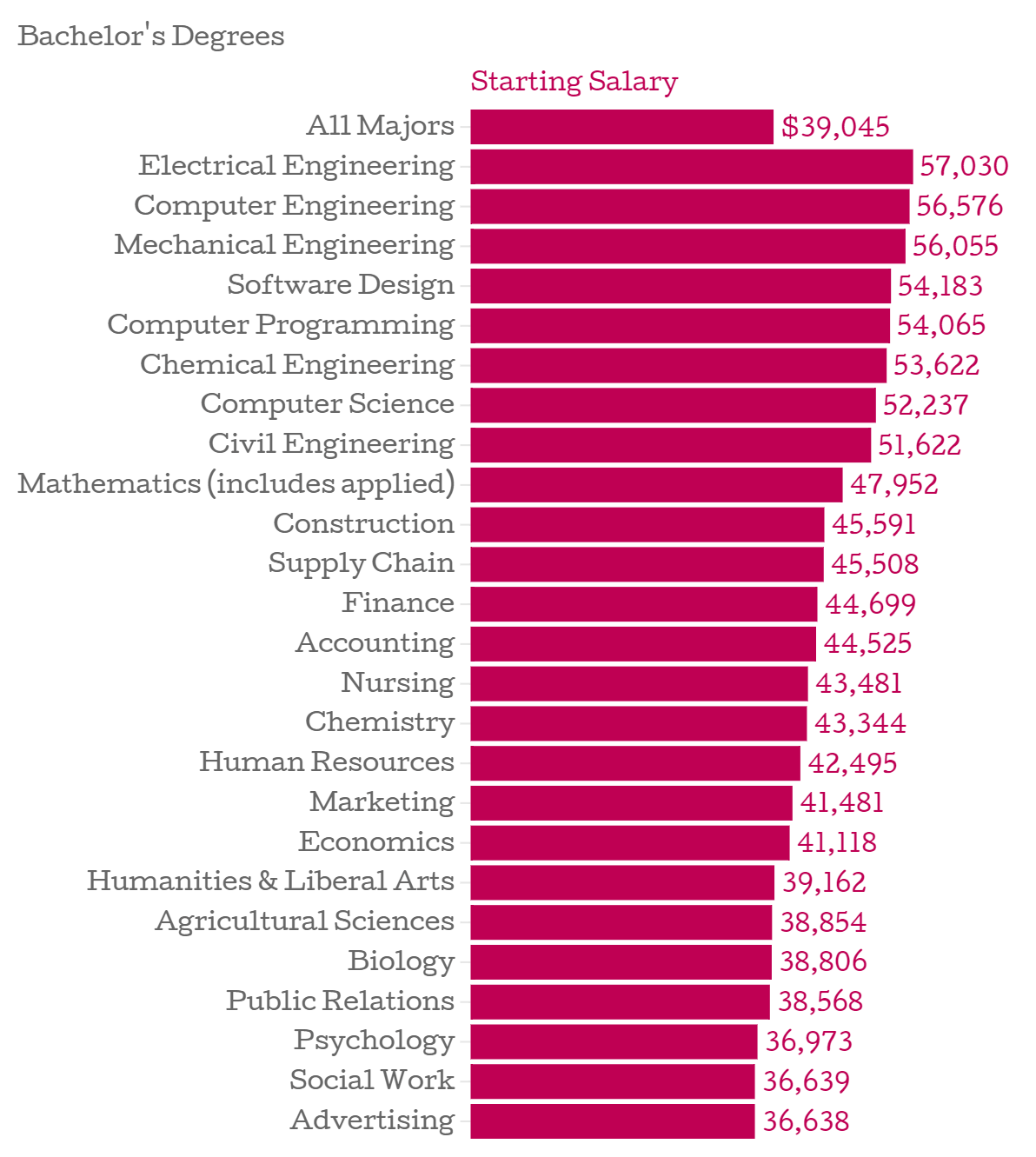

According to a study done by the Collegiate Employment Research Institute (CERI) in Michigan, the degrees which yield the highest starting salaries in 2015 are electrical engineering, at $57,000, and computer engineering and mechanical engineering, both at $56,000.

Alternatively, the www.payscale.com website has a much longer listing and indicates that the starting salary for someone with a degree in petroleum engineering can be as high as $103,000, followed by chemical engineering at $68,000, and nuclear engineering at $67,000.

Alternatively, the www.payscale.com website has a much longer listing and indicates that the starting salary for someone with a degree in petroleum engineering can be as high as $103,000, followed by chemical engineering at $68,000, and nuclear engineering at $67,000.One thing is for sure, the more specialized your new-found skills are, the more in-demand you will be and the higher the potential starting salary you’ll have.

Will you see a return on your college investment?

So, all things considered, the big question is, will it be worth it? Obviously math is a big part of it; what kind of a dent will you be making in your household cash flow for four years, will you have to repay a loan for 10 years+ after graduation, what is your earning potential once you’ve earned the degree, etc? But if you’re considering taking this plunge, then obviously you’ve got an emotional burden you’re trying to lift as well. And only you know what the cause of that burden is, what the cost of it is on you and your family, and what kind of relief you can expect from having it lifted.

Basically, if you’ve got the financial ability to weather the college storm for four years and you’ve got the support of your loved ones behind you, then only you can decide if a new college degree is what’s needed to get you to that next level in your career.

Basically, if you’ve got the financial ability to weather the college storm for four years and you’ve got the support of your loved ones behind you, then only you can decide if a new college degree is what’s needed to get you to that next level in your career.Only you can assess whether it will be the best thing you ever did for yourself or whether your college degree will end up being the most expensive piece of art hanging on your wall.

Share this post: