How to Avoid Gift Tax

BL

Summary:

A gift tax is a tax levied on the transfer of assets from one party to another as a gift. It exists to prevent people from circumventing the estate tax. However, there are several exemptions and structuring methods to mitigate gift tax, or to avoid it altogether.

Assets transferred from one party to another will incur a “gift tax,” as deemed by the Internal Revenue Service (IRS). A gift tax is implemented by the IRS to prevent people from circumventing the estate tax, which requires that wealth passed down after death is taxed.

However, anyone who is familiar with the American tax system is aware that it is full of exceptions, loopholes, and structures that allow people to mitigate their tax burden. If you give gifts for medical, education, or tuition purposes, your gift can be excluded from gift taxes. Lastly, if you properly structure your gifting over time, you can end up paying very little gift tax at all.

Compare Tax Preparation Services

Compare multiple vetted providers. Discover your best option.

What is considered a gift?

According to the IRS, a gift is “any transfer by gift or real or personal property, whether tangible or intangible, that you made directly or indirectly, in trust, or by any other means.” If you give something to someone for free, which is what most people consider a gift, then this will incur taxes. Likewise, if you sell something to someone for substantially below its intrinsic value, then this is also considered a gift.

Let’s say that you have a small cottage worth $500,000 in the mountains of Idaho that you never use. Your nephew goes skiing in Idaho all the time. Since you never use the home, you decide that you want to sell it to him for $200. Although you are not giving it to him for free, you are transferring the asset for $499,800 below fair market value. In the eyes of the IRS, this is a gift.

IMPORTANT! Keep in mind that trying to sell someone something far below fair market value to avoid gift tax has a special name. That name is tax evasion and is a dangerous game that we highly recommend you don’t attempt to play.

Specific gift tax exclusions

The IRS offers across-the-board exclusions for certain types of gifts, as well as the recipient of those gifts. Here are the basic IRS gift tax exclusions that you should consider if you’re trying to avoid as much gift tax as possible.

Educational exclusions

Gifting money related to tuition and educational expenses can be excluded by the IRS. This is particularly pertinent for those looking to contribute to 529 plans that their younger families might have.

If you are a grandparent and want to gift some money before you pass, contributing to a grandchild’s 529, or directly paying for their current private school K-12 tuition is a great way to avoid gift tax.

Medical exclusions

Luckily, the IRS recognizes that good Samaritans who contribute to others’ medical bills are not liable for gift tax.

Suppose your favorite cousin has a brutal motorcycle crash and must spend a significant amount of time in intensive care learning how to walk again. In that case, your contributions to his potentially enormous medical bills will be excluded from the gift tax.

Spousal gifts

When two people are married, and one passes away, the money is automatically passed to the wife or husband free of any tax. The same goes for gift tax. As you share the same estate as a couple, any gift you give to your spouse will not be liable for gift tax.

Gifts to charities and political organizations

Gifts to charities and political organizations are excluded from gift taxes, as they incur other forms of taxes. If you give $20,000 to your favorite dog rescue, this will not have a gift tax. However, be careful with this one as it only works for qualified charities and political organizations.

If you are thinking to yourself that you can have your uncle set up a shell company in Delaware that has the title “Puppy Rescue LLC,” but nothing else so that you can sneak some money to your nephew, stop thinking about it. This would also be considered tax evasion. Remember, the IRS is like the Eye of Sauron — it’s always watching.

Annual and lifetime exclusions

In addition to the exclusions for specific items related to things like medical bills and tuition, the IRS also offers exclusions based on time. These are defined by annual exclusions and lifetime exclusions representing a gift tax limit.

Annual exclusion

As of 2022, the annual gift tax exclusion for individuals is $16,000. For a married couple filing jointly, it is double that figure at $32,000. This means that in 2022, you and your wife will have an annual exclusion amount of $32,000 per year without having to pay any tax as an annual gift limit.

If you exceed that amount, or have significantly more money that you want to give, it’s absolutely imperative to know about the other time-related exclusion: the lifetime exclusion.

Lifetime exclusion

Lifetime exclusions are exclusions from gift tax that are based on a lifetime rather than a finite number of years, or annual limit. The lifetime exclusion in 2022 is $12.06 million. You can give a gift of up to $12.06 million per individual or $24.12 million for a married couple.

Any overage that occurs on your annual exclusion will get absorbed by your lifetime exclusions, and you most likely won’t need to pay any gift tax.

Examples of using time-related exclusions

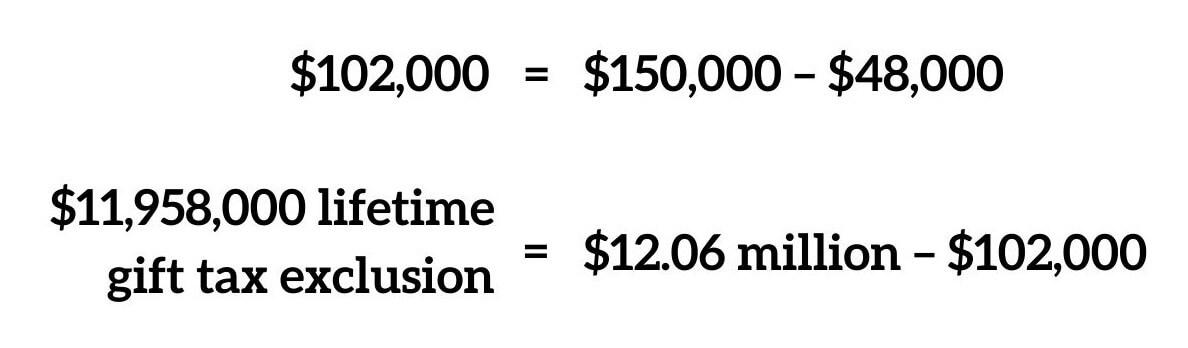

Let’s say that in 2022, 2023, and 2024, you gave your nephew $50,000 each year for a total of $150,00. Over a three-year period, based on today’s information, your total annual exemption for the three years would be $48,000.

This $102,000 will then be applied to your lifetime exclusion of $12.06 million. So you pay no gift tax on the money, but your lifetime exclusion will take a dent. The formula will look like this.

You will need to submit a 709 form to the IRS when requesting exemptions on an annual or lifetime basis. Remember that the lifetime exemption is on a per donor basis, and not a per receiver basis. This means you are capped at $12.06 million no matter who you give the gift to. If you have significantly more money than this that you wish to give, it might be wise to look at trust structures.

Looking for tax software or a tax preparation firm that can help you with either mitigating your gift tax or even income tax? Here are some that can help you.

Pro Tip

The IRS sets its lifetime and annual exemptions in conjunction with inflation. This means that although the lifetime exemption in 2022 might be $12.06 million, it could be considerably different than that ten or even 30 years from now.

Estate taxes and trusts

The purpose of the IRS implementing the gift tax was to prevent people from attempting to circumvent the estate tax. The estate tax is a tax levied on wealth and assets passed down from one generation to another.

In most cases, it involves one or two parties dying and their beneficiaries receiving the assets. It must be emphasized, however, that the amount of people in the United States that are liable for estate tax is minimal. The 2017 Tax Cuts and Jobs Act doubled the estate exemption for tax years from 2018 through 2025.

The 2022 rate is $12.06 million but will revert to the pre-2018 level of $5 million in 2026. According to the Congressional Budget Office, of the 2.7 million Americans who died in 2016, only 5,500 estates were required to pay any estate tax.

However, for those lucky few who have a considerable amount of assets that they hope to pass on to their next of kin, and want to avoid both estate and gift taxes, they should consider setting up a trust.

How does a trust work?

The typical structure of a trust involves three parties: the grantor, the beneficiary, and the trustee. The grantor grants the money to the beneficiary, but the third party (trustee), administers and protects the trust.

Let’s say that you have $50 million that you want to transfer to your only son. That $50 million is obviously way above the lifetime exclusion. If you were to give that directly to your son in 2022, it would trigger a large tax on everything above the $12.06 million lifetime exclusion (it could be higher in the future).

Rather than giving those $50 million to your son, you give it to a trustee, who then keeps and or invests the money on behalf of your son (the beneficiary). In many cases, people will use a Crummey trust, particularly when giving to their children. But keep in mind that a Crummey trust can have specific rules, regulations, and limitations on how and when the beneficiary can access the money.

FAQs

How does the IRS know if you give a gift?

Typically, the IRS knows if you give a gift because you will fill out a gift tax return. They might know either way though, so be diligent and aware.

How do you gift a large sum of money to family?

As long as you are within the annual or lifetime exclusion amount under federal gift tax law, you should be able to gift. You can also contribute to educational expenses or file a trust.

What gifts are not subject to gift tax?

Medical expenses, educational expenses, and gifts to a spouse are all monetary gifts that are not subject to gift tax under 2022 tax laws.

What happens if I don’t file gift tax?

If you give a substantial gift and don’t file for gift tax, you could be liable for tax avoidance, tax evasion, or another crime. Make sure you always fill out your gift tax returns to avoid these penalties.

Do cash gifts count as income?

No, for the beneficiary of the gift, cash gifts do not count as income.

Key Takeaways

- Gift tax is a tax levied on the transfer of assets from one party to another for free or substantially below fair market value.

- The IRS gives exclusions on gift tax for medical expenses, educational expenses, transferring to a spouse, or donating to a political committee or charity.

- The IRS also offers an annual gift tax exclusion and a lifetime exclusion to help you avoid the gift tax.

- Trusts are a great way to avoid gift tax and estate tax limits.

Share this post: