How to Build Credit at 18

BL

Summary:

You can build up your credit score even at a young age by becoming an authorized user or getting a secured credit card or credit builder loan. However, you can’t get a great score just by opening accounts. You’ll have to continue building your credit by making timely payments and maintaining a balanced credit utilization ratio.

According to Experian, the average credit score in the U.S. has increased from 693 in 2012 to 714 in 2021. That’s around a 3% increase in a 10-year period. Americans are becoming more credit-worthy. There is no reason you can’t stay on this trend, even if you’re just starting out.

There are a few ways you can start to build credit, even if you are young. Getting a credit card of your very own or becoming an authorized user of another credit card are two very simple ways to do this. Taking out a credit builder loan is another option.

However, opening accounts is just one part of the credit-building process. Understanding how credit works, how to maintain your balances, when to pay them off, and how to review your score are all steps you can take to begin building credit as an 18-year-old.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How credit works

To understand how to build your credit, you must first understand how credit works. At the top of all credit-related topics is your credit score. You can always find your credit score by requesting a credit report from one of the various agencies.

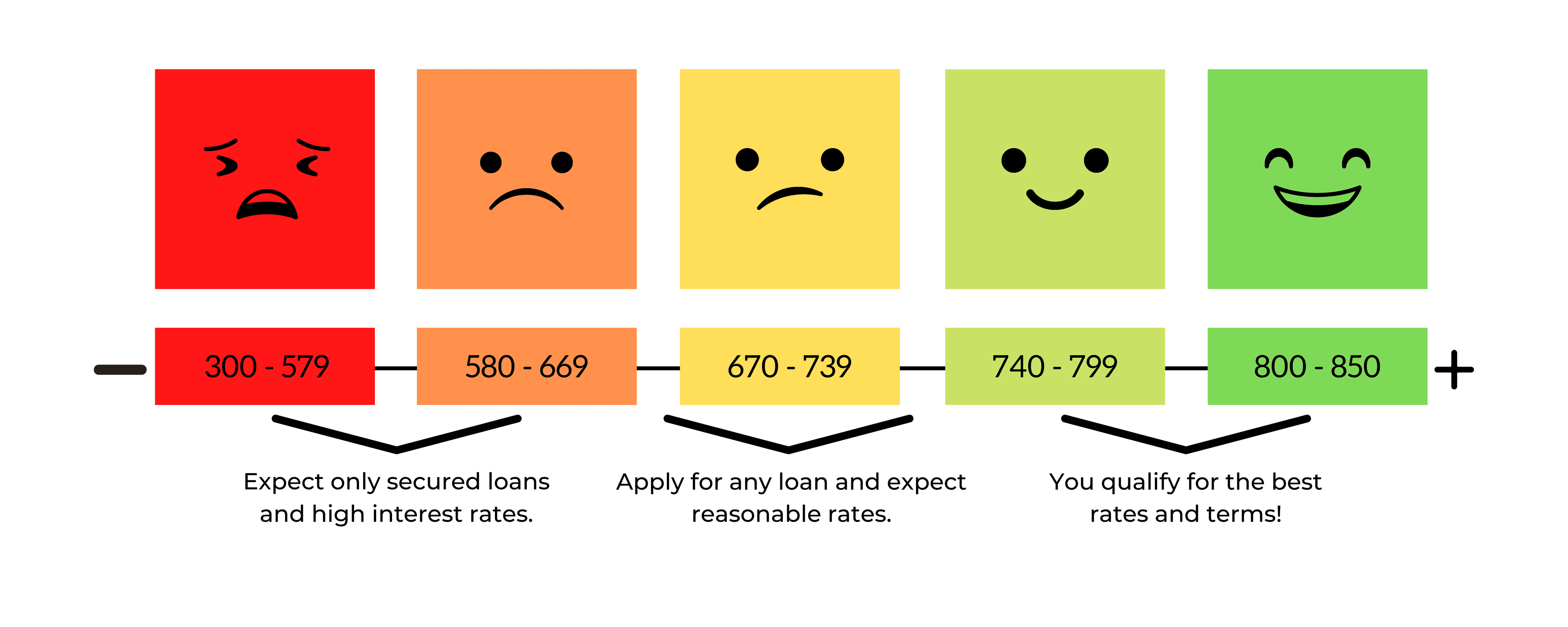

A credit score is a numerical expression that deems how creditworthy you are. You may also hear your credit score called a FICO score. Credit scores typically range between 300 and 850. A 300 credit score is considered the worst possible credit, which will make it difficult to open any credit line. With a number of 850, you effectively have the best credit possible. With a good credit score, you can easily obtain loans or open a new bank account.

What’s in a credit score?

Though it may seem like it at first, your credit score isn’t a random assortment of numbers. The three major credit bureaus — Experian, Equifax, and Transunion — consider five factors to determine your credit score:

- Payment history. As the name might suggest, your payment history is determined by how timely you are at making your bill payments.

- Amounts owed. To determine “amounts owed,” credit bureaus compare how much debt you currently owe to your available credit, or what credit you can still spend. According to CNBC, for a general rule of thumb, you never want to exceed 30% of available credit.

- Length of credit history. The length of your credit history is measured by how many current accounts you have open and how long these accounts have been open.

- Credit mix. Different types of credit are considered better as you are more diversified. Getting a mortgage and a credit card account are two different types of loans that will better diversify your credit.

- New credit. “New credit” refers to how many credit accounts you recently opened. This factor also considers any credit inquiries in your file, which you receive each time you apply for a new account or loan.

Some will have different scores for the same person, so it’s important to know which credit bureaus have what scores to understand your total FICO average.

How to build credit at 18 years old

Now that you understand what constitutes a credit score, you can start to establish your own. Here are some ways for 18-year-olds to start building their credit, so their FICO scores are the envy of everyone when they hit the ripe age of 21.

Starter and secured credit cards

It’s difficult for 18-year-olds to obtain credit cards like older adults because they have no credit experience. However, there is a simple hack for this. Shop around for a secured or starter credit card.

A secured credit card is a card that needs a security deposit before you can start using credit. Since you’re putting “skin in the game” with the deposit, it’s easier for you to get credit. Discover and Capital One are two well-known credit card companies that offer secured credit cards.

Looking for the right credit card for you to help build your credit? Here are some great secured cards that you might be interested in.

Get an unsecured credit card

It’s not as easy to get an unsecured credit card for an 18-year-old as it was in the past; however, there are methods to do it.

The number one thing is to have a job. If you have a stable job that provides income, it makes it much easier to get a credit card. Furthermore, if you have a co-signer on your credit card, then it’s also an option to obtain your own credit card under your own name.

Pro Tip

The income from your job is very important. So if you just turned 18 but have a stable job, you might want to wait until you are able to collect pay stubs for a few months from your employer. If you walk into a bank or credit card company with six months of strong pay after you turn 18, this can be instrumental in getting your very own credit card.

Be an authorized user

As an authorized user, you’re attaching yourself to someone else’s credit card. This way, even without using the card, you can benefit from the primary user’s credit, particularly if it’s an older credit account. This is usually a parent, but it could be a cousin, godfather, or friend of the family who is willing to do a favor.

However, keep in mind that being an authorized user can have an adverse effect on your credit as well. If the primary user pays their bills late or runs up their balance to the credit limit, this can negatively affect the credit of the authorized user. Because of this, make sure the primary user of the card is financially secure and organized.

Get a credit builder loan

A credit builder loan is a savings plan disguised as a loan that is designed to help you improve your credit by framing your monthly deposits as “loan payments.” Here’s how it works.

In this type of loan, you actually pay the lender before you receive the loan, similar to a secured credit card. Say you want a loan of $2,000. By using a credit builder loan, you first split the $2,000 into monthly payments, which you make until you pay all $2,000. At the end of the term, you receive the loan. Credit builder loans are a great way to work with a financial institution to build credit and establish a credit utilization rate.

Get a traditional loan

There aren’t many loans available to 18-year-olds, but there are some. A car loan is a perfect example of a loan that some 18-year-olds can get. This is because the loan has collateral, the car, that a lender can repossess if the borrower doesn’t pay.

However, it’s difficult for 18-year-olds to get full car loans. This means you might need some type of money down along with the car loan or a co-signer to get approved.

Keep tabs on your credit

It’s important to understand that your credit can fluctuate depending on the data that’s available to the credit bureaus.

For example, if you had a hospital bill that you paid off 100%, but your account shows as unpaid, it could really hurt your credit even if it’s not true. Therefore, it’s a good idea to regularly check all three of your credit reports (Experian, TransUnion, and Equifax) to make sure the information is accurate. The three credit bureaus all have online portals where you can get a free credit score and see what’s affecting your credit. You can also use AnnualCreditReport to check all three credit reports once a year for free.

Stay organized

Make sure that any bills or open credit you have are organized properly. You can use an Excel file or an online spreadsheet template to track your spending and bill payments. It’s important to keep track of everything at the beginning so that you pay your credit card bill on time, do not use too much credit, keep track of your credit reports, and maintain a healthy balance.

FAQs

What is the fastest way to build credit at 18?

The fastest way to build credit at age 18 is to get a credit card, either secured or normal. If you can take out an auto loan, you can also build credit this way.

What credit score do you start with at 18?

Unfortunately, you don’t magically receive a credit score once you turn 18. After a few months of establishing your credit (whether that’s right when you turn 18 or later), you’ll probably have a score within the 500 to 700 range. If you were an authorized user before you turned 18, you’ll likely have a higher score as long as the primary user made prompt bill payments.

Does credit build before 18?

You can only start building credit before you are 18 if you are the authorized user of an account. This is because people below 18 do not have access to normal financial products like adults would.

Key Takeaways

- Building credit is essential to access most modern financial products, such as mortgages, credit cards, and loans.

- If you’re 18 years old, it’s important to understand some of the things that go into a credit report, such as payment history and credit usage.

- There are several ways to build credit at the age of 18. You can get a secured credit card, an auto loan, or become an authorized user on someone else’s card.

- Understanding where to find your FICO score, and tracking it in an organized way, is fundamental to tracking and building your credit over time.

Share this post: