Certificates of deposit are risk-free, federally insured investment products that pay a fixed interest rate and guarantee the return of your invested funds plus interest. However, like most investment topics, effectively using CDs in your personal financial world can be complex. Before you decide to invest in a CD, you need to determine whether a CD is right for you and decide what type of CD to invest in. You must also consider where you will purchase your CD from, how long the CD term will be, and what investment strategy you will use.

Are you trying to save for a major purchase over the next few years or looking for a safe place to stash your

retirement funds before you stop working? If you are, you may want to take a closer look at certificates of deposit (CDs).

Compare Brokerage Services

Compare multiple vetted providers. Discover your best option.

Certificates of deposit 101

CDs require an initial deposit that earns a fixed interest rate over a defined term until the maturity date. They generally pay a higher interest rate than a savings account or

money market account, although lower rates than what you can find in bonds. Since both the principal and interest are guaranteed, CDs are also a relatively risk-free banking product. They are also either FDIC- or NCUA-insured if issued by a bank or credit union, respectively.

In this article, we help you consider five questions that can help you navigate CDs, understand the different kinds of CDs available, and start planning how to this investment option. These questions are:

- Is a CD right for you?

- What type of CD is best for you?

- Where will you purchase your CD?

- How long should your CD term be?

- What type of CD investment strategy will you use?

1. Is a CD right for you?

The first step in any

investment decision is to define your investment goals and strategy and decide whether a certificate of deposit is right for you. Start by asking yourself a few questions.

- What do you hope to get out of your investment? What is the preferred result?

- What is an acceptable level of risk?

- What are your cash flow needs? Do you need short-term liquidity?

The answers to questions like these will help guide you or an investment advisor through choosing a CD and investment strategy. Since CDs are a low-risk investment, risk-averse investors or investors looking to retire soon may be attracted to CDs. However, those looking to risk more and earn more may want to consider investing in

index funds or the

stock market instead.

If you feel overwhelmed or do not know where to begin, speak to a

financial advisor to guide you through the process.

Related reading: For a deeper look into what certificates of deposit are and how they work, look at our

detailed guide on CDs.

2. What type of CD is best for you?

If you decided that CDs were the right type of investment for you, it’s now time to decide what kind of CD suits your investment strategy best. Here is a breakdown of the many types of CDs that exist on the market.

| CD Type | Characteristics | Example |

|---|

| Traditional | Traditional CDs are the most common type. An investor deposits funds at the beginning, then the CD pays a fixed interest rate over a defined period, after which they can receive the principal or roll it into another CD. | You deposit $1,000 into a six-month CD paying 3% annually. Six months later, you receive your $1,000 plus interest earned. |

| Bump-up | A “bump-up” is a traditional CD that allows you to “bump up” to a higher interest rate if the institution holding the CD raises the rate of a similar term CD. Bumping up to a new rate is typically only allowed once per term. The rates on bump-up CDs are less than that of a similar-length traditional CD. | You buy a three-year $1,000 bump-up CD with an annual rate of 2%. Six months later, the bank raises the three-year rate to 2.75%. You can ask the bank to increase your rate for the next 30 months. |

| Step-up | Like a bump-up, the CD moves to a higher rate over time. However, step-up CDs automatically raise the rate by a predetermined amount at specified times during the term. | You purchase a three-year CD at 1.75%, where the rate goes up by 0.25% every year. |

| Liquid (no-penalty) | A liquid, or no-penalty CD, does not charge early withdrawal fees, allowing you to withdraw your money if needed. These CDs typically earn a lower rate than a traditional CD of the same term. | Compared to the traditional CD example above, a similar $1,000 two-year no-penalty CD will have a rate of less than 3%. |

| Zero-coupon | Similar to a zero-coupon bond, a zero-coupon CD does not pay periodic interest payments. Instead, an investor purchases the CD at a discount to its par value, and upon the end of the term, you will receive the par value. | You purchase a two-year zero-coupon CD with a par value of $1,000, for $985. Upon maturity in two years, you will receive $1,000, earning $15 in interest. |

| Callable | Similar to a traditional CD, this CD pays a fixed interest rate for a set period. However, the financial institution has an option to “call” or buy back the CD before the term ends. An institution would do this if the interest rates have fallen below the level they are paying this callable CD. | You buy a two-year CD paying 3% annually that is callable after one year. The prevailing interest rate drops during the first year so similar CDs pay 1.5%. The institution exercises its call provision, repurchasing your CD. You receive the original principal plus any interest earned. |

| Brokered | A brokered CD is sold through a brokerage firm. This means you don’t have to open an account at multiple banks to shop for the best rates. Instead, you can have one account hold CDs of different types, maturities, and financial institutions. A brokerage firm can also buy or sell CDs on the secondary market. | You open a brokerage account with a firm and buy a CD offered through the brokerage platform. The CDs can take the form of any CD on this list. |

| High-yield | As the name implies, these are typically traditional CDs with a relatively high yield. | You purchase a two-year high-yield CD that pays 3.5%, whereas other CDs are paying 2.75%. |

| Jumbo | Jumbo CDs require a large upfront deposit, typically $100,000 or more. An institution could reward an investor for a large deposit with a higher rate, though that may not be the case. | You buy a $250,000, two-year jumbo CD paying 2.5%. By comparison, a traditional non-jumbo two-year CD pays 2.4% and requires only $1,000. |

| Add-on | Most CDs require you to deposit all of the CD funds upfront and don’t allow further contributions. An add-on CD lets you add more money during the term, though there may be limits on the number of times you can “add on.” | You purchase a two-year add-on CD paying 2% for $1,000. Then, every six months, you deposit an additional $500. At the end of the term, you receive the deposited funds plus any interest earned. |

| Foreign currency | A foreign currency CD allows you to use U.S. dollars to initially purchase a CD. Those funds are then converted to a foreign currency (pound, euro, etc.) and then back to U.S. dollars at maturity. This CD introduces additional risks to your money, such as the risk of a dropping foreign exchange rate. | You buy a two-year euro-denominated CD paying 3% for $10,000. Your money is converted into euros at the current exchange rate and earns interest. Upon expiration, the principal and any interest are converted back to the U.S. dollar at the exchange rate at that time. |

3. Where will you purchase your CD?

Let’s call this the “shopping around phase.” As you can see from the list above, you can find CDs outside of just banks or credit unions. Sometimes certain institutions will only offer specific kinds of CDs (e.g. you can only buy brokered CDs from a brokerage firm), so keep this in mind when you shop around.

There are many different types of CDs sold by many different banks, credit unions, and brokerage firms. We recommend looking at multiple options comparing rates, fees, and any commissions associated with the purchase. For instance, use the comparison tool below to start looking for the best brokerage firm for your needs.

Pro Tip

Not everybody has the time to manage their investments, and you may find you feel similar. If you find you can’t manage your CD investments, consider hiring somebody to handle your CDs for you. If you do so, keep in mind that they may use

brokered CDs, which have different features than a traditional CD.

4. How long should your CD term be?

CDs come in various term lengths (or years until the CD matures) and the principal is returned to the investor. The terms can range anywhere from three months on the short end to five years on the long end. However, some banks offer shorter-term (28 days) or longer-term CDs (up to 20 years).

How you decide your CD’s term depends on why you’re purchasing the CD. If you have a specific goal with a due date in mind, base the length of the CD on that goal. For example, if you plan on buying a house in two years, you should purchase a two-year CD.

However, if you don’t have a specific goal in mind, you may want to decide on a CD based on

interest rates. Since long-term CDs come with higher interest rates, you may find that investing in a five-year CD is worth the wait. To get a better idea of the difference in interest rates, take a look at some of the CD accounts below.

5. What type of CD investment strategy will you use?

You can utilize three main CD investment strategies to help achieve your goals. These are the ladder, the barbell, and the bullet.

Each strategy has its purpose and usefulness depending on your goals. Understanding the details of each and how they affect your personal finance situation will help guide you in a particular direction.

CD ladder

A

CD ladder is a way to layer multiple CD terms of varying term lengths to create a strategy where you receive your principal balance and interest back at regular intervals (monthly, quarterly, annually, etc.).

For example, if you want to receive cash flow annually, you can purchase a one-year, two-year, and three-year CD. At the end of Year 1, you receive the interest payment and have one year left on the original two-year CD, two years on the original three-year CD, and three years on the newly purchased three-year CD. You take the principal and buy another three-year CD each time a CD expires.

This strategy creates a regular and predictable cycle of cash flow. With a larger CD ladder, you can also take advantage of the higher interest rates on longer-term CDs once the process matures past the first few years.

Pro Tip

A CD ladder allows you to play around with interest rates on different CDs. Though you may want to invest equal amounts into each CD (like $10,000 in each), that doesn’t have to be the case.

For instance, you could weigh the shorter-term CDs to make up for the lower interest rate ($15,000 in a one-year, $10,000 in a two-year, and $5,000 in a three-year CD). You could also invest more money into the high-interest rate CD to take advantage of the higher rate.

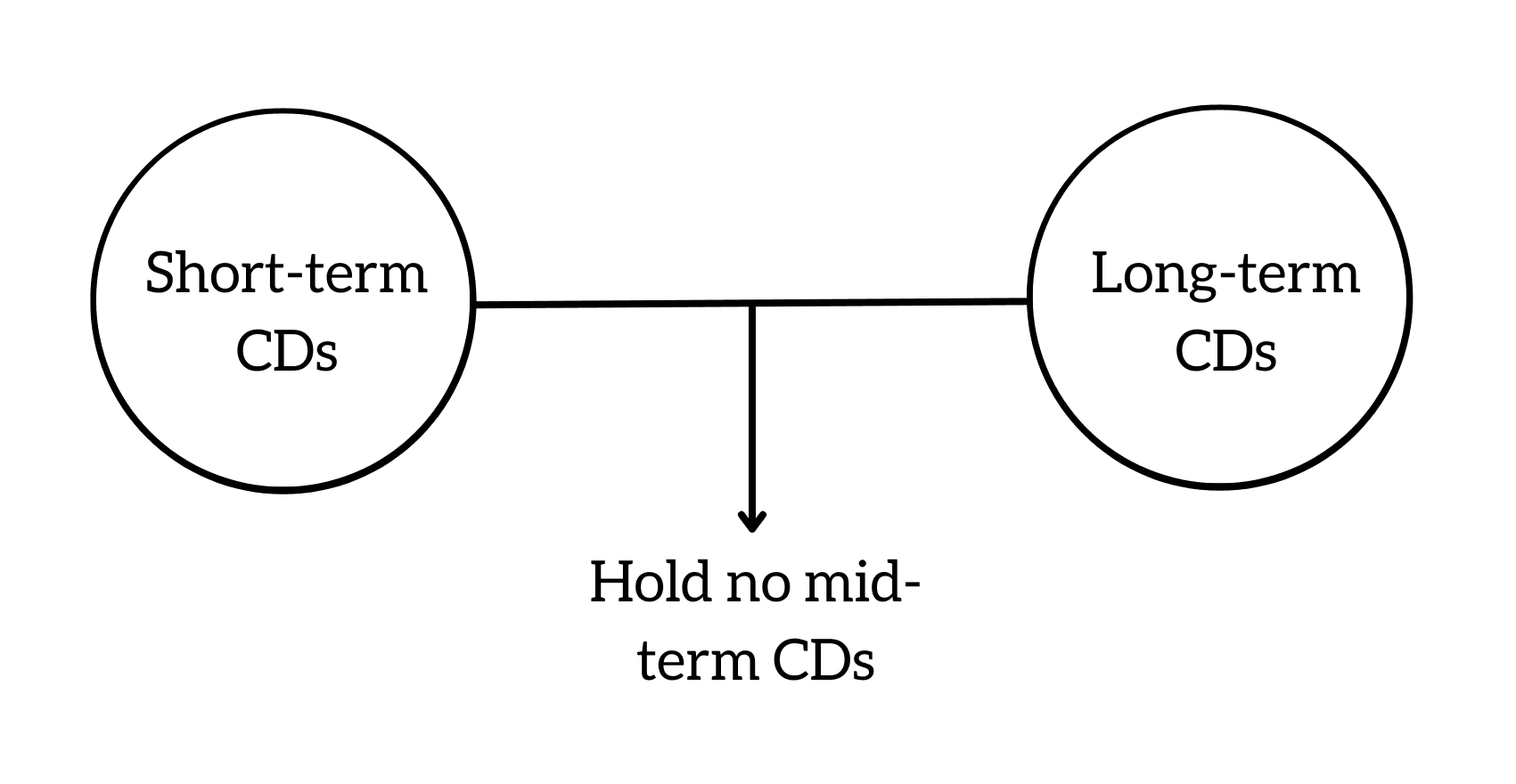

Barbell

The CD barbell strategy focuses on purchasing short- and long-term CDs and ignoring mid-term CDs. Think of it almost as a ladder without the middle rungs, where all your funds instead go towards the top and bottom rungs.

For example, let’s say you purchase a $10,000 five-year CD and a $10,000 one-year CD. Each year you take the proceeds from the one-year CD and buy another one-year CD until there is one year left on your five-year CD.

At this point, you buy another five-year CD and start the cycle again. This strategy could be beneficial in a rising interest rate environment, where the one-year CD rate increases each year.

Bullet

While the strategies above have the investor purchase multiple CDs with different maturity dates, the CD bullet strategy involves purchasing multiple CDs that all mature at the same time. This is great for an investor that has a big purchase or needs money at a specific date in the future.

For instance, if you want to save up for a large purchase five years from now, you could buy a five-year CD today, then one year from now buy a four-year CD, and so on until they all mature in five years. This creates a large cash flow in year five to help with the large purchase.

Pitfalls

Unfortunately, as with all investments, CDs come with their fair share of risks. Before investing in a CD, make sure to carefully review the downsides of this investment opportunity.

Not accounting for inflation

One of the cons of CDs is that they typically pay a low-interest rate that does not keep up with

inflation. However, the average one-year CD interest rate is still under 1%. That would imply a real return of -6%.

A negative real return is particularly troubling for those investors using CDs to create income in

retirement, as they would lose purchasing power. Understanding how inflation will affect your planning and strategy is key to having realistic expectations and deciding if CDs are the correct investment for you. You can also reach out to an investment advisor for specific advice pertaining to your unique situation.

Early withdrawal penalty

Though not found in every CD, most certificates of deposit will charge an early withdrawal penalty if you access your funds before the CD matures. While you can’t always avoid early withdrawals, it’s important to keep this downside in mind when deciding whether to invest in a CD.

That being said, you could also purchase a no-penalty CD with no early withdrawal fee. While these CDs will likely pay a lower interest rate than traditional CDs, it may be worth the lower rate if you think you’ll need to access your funds sooner.

Not aligning the CD or strategy with your goals

One of the biggest mistakes many investors make is purchasing financial products or implementing financial strategies misaligned with their goals and objectives.

Looking back at the example of the investor that wants to buy a house and two years, it would not make sense to purchase a five-year traditional CD with the money they want to use as a down payment, as it could lead to early withdrawal fees. Similarly, the same investor purchasing a three-month CD may lose an opportunity to earn higher interest rates on a longer-term CD that aligns with their time horizon.

FAQs

Is there a minimum deposit amount for CDs?

This depends on the institution you purchase your CD from. Some financial institutions require a minimum deposit for CDs (like $1,000 or $10,000), while others have a $0 minimum.

You may also have to meet different minimum investment requirements depending on the CD you buy. Jumbo CDs, for instance, often have minimum deposit requirements of $100,000 or more.

When is the interest paid on my CD?

The length of the CD determines when interest is paid. Generally, you receive the interest at the maturity date if the term is 12 months or less. The interest will pay annually if the maturity is longer than 12 months. Check with your institution to see when and how interest is paid.

Are CDs federally insured?

Yes, generally, certificates of deposit are federally insured up to $250,000. Depending on whether the CD was sold by an issuing bank or credit union, the CD will have FDIC insurance or NCUA insurance, respectively.

Key Takeaways

- The key to successful investing with CDs lies in how the strategy aligns with the investor’s goals and objectives.

- Not only are CDs FDIC-insured, but they also offer risk-averse investors a chance to earn interest rates greater than a traditional savings account.

- There are many types of CDs to choose from, some of which may align with your goals better than others.

- When comparing CDs, make sure you shop around different banks and institutions to find the best CD for your strategy.

CS

Chip Stapleton

Chip Stapleton is a Series 7 and Series 66 license holder, CFA Level II candidate, and holds a Life, Accident, and Health Insurance License in Indiana. Chip received his Bachelor's in Saxophone and Physics from the Indiana University Jacobs School of Music in 2008. During his time there, he honed his mathematical and analytical skills. He received his Master's in Music Technology from Indiana University Purdue University—Indianapolis in 2010, where he was a Graduate Assistant. He is a financial advisor who enjoys the opportunity to train, develop, and support new advisors to build their own practices and help their clients achieve their goals. This included helping with case design, product knowledge, investment analysis, investment recommendation, portfolio construction, asset management, financial statement analysis, business planning, and business exit strategies.

Share this post: