What Can You Expect in the IRS Collection Process?

AL

Last updated 04/08/2024 by

Andrew LathamFact checked by

The IRS collections machine seizes $54 billion every year from delinquent taxpayers through its enforcement activities. That sounds like a lot until you realize taxpayers underpay the IRS $458 billion in taxes every year. That leaves a tax gap of $406 billion in the United States annually. When you look at it that way, it’s no surprise the IRS is such an aggressive debt collector.

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What is the IRS collection process?

The IRS collections process includes every measure the IRS can use to collect back taxes. These measures range from allocating future tax year refunds to repay your tax debt all the way to seizing everything you own. If you ever end up facing the IRS for tax collection, you’ll need to understand what the IRS can and cannot do.

There are two reasons you could find yourself on the business end of the IRS collections process:

- Not paying your taxes in full when you file a tax return

- An IRS audit reveals errors or issues in your tax return that increase your tax liability

What happens next?

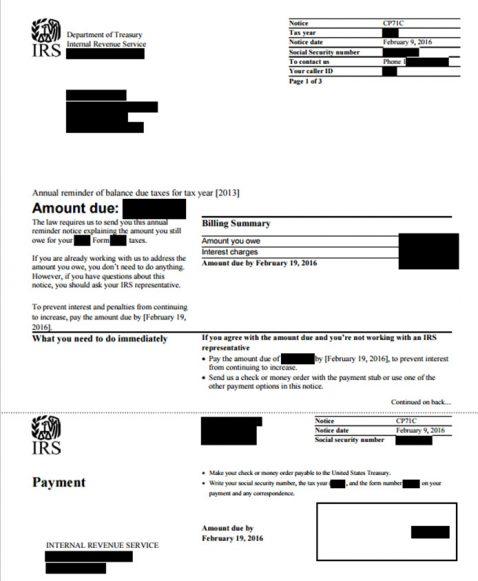

In either case, the IRS sends you a tax bill. This bill is the first step in the IRS collections process. The first notice you receive will explain how much you owe the IRS and will demand full payment. The letter will also include any interest or penalties added to your initial tax bill. If you pay the bill in full, the IRS will close your case. Problem solved.

The IRS collections process timeline begins

After sending a final demand for payment, both through the mail and by telephone, the IRS will start enforcing their legal right to take from you what is owed. The IRS has unparalleled authority when it comes to collecting debts and the collection actions that they can take. The actions used by the IRS during the collection process include a federal tax lien, tax levies, asset seizure, bank levies, wage garnishment, and civil tax penalties. These actions can continue until all tax debt is paid, which may take many years depending on how much you owe.

Tax liens

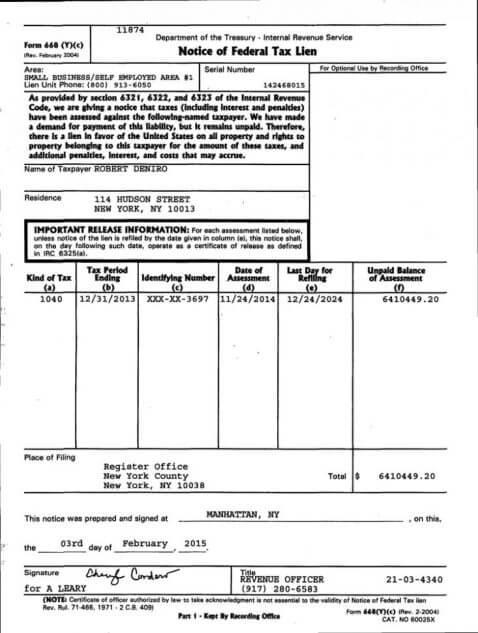

A federal tax lien is typically the first of several actions used in the IRS collection process. As soon as the deadline for payment passes and the case enters a collection status, a statutory tax lien goes into effect.

What is a statutory tax lien?

A lien is a legal claim against your property, with property defined as anything and everything that you own or will own. This includes your home, car, business, bank accounts, and retirement accounts, among other items.

The legal claim of a tax lien stops short of giving the IRS ownership and control of your assets. The IRS cannot use a tax lien to tow away your car or take possession of your house.

However, a tax lien does give the IRS ownership of any proceeds that you might get from selling your assets. Sell any property, and the money from that sale will go to the IRS. You will not receive any of the proceeds until your debt is fully covered.

The tax lien is statutory because it is written into the legal code and occurs automatically when the payment deadline passes. There is no judge involved and no court hearing where you can challenge the lien. There isn’t even any paperwork to be filed, and the taxpayer does not need to be notified that the lien is in effect. The statutory tax lien simply exists when the IRS has past due taxes to collect.

What is a Notice of Federal Tax Lien (NFTL)?

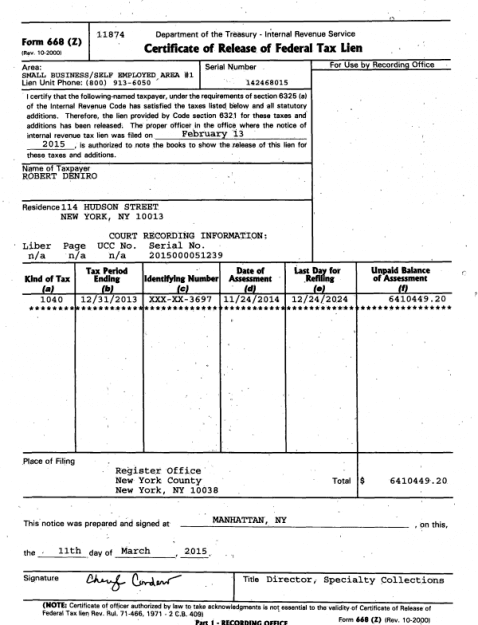

A Notice of Federal Tax Lien, or NFTL, occurs when the IRS makes the tax lien official by filing a notice with your local court or your state’s Secretary of State Office. Until then, the tax lien was an issue between you and the IRS. However, when a tax lien is a matter of public record, all of your creditors (both current and future) will know the IRS has priority over all your assets. This could lower your credit score by up to 100 points and make it much harder to get a loan or refinance an existing one.

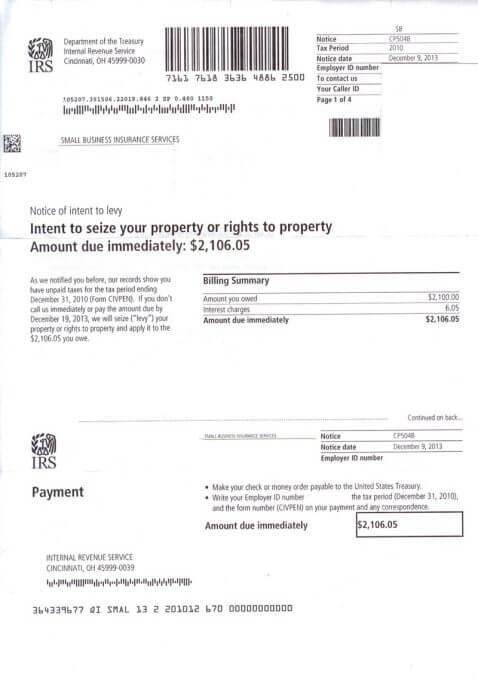

Tax levies

With a tax lien, the IRS does not actually take ownership or possession of your property. Instead, it lays claim to all of your assets. With a tax levy, on the other hand, the IRS actually takes ownership of your property. It can legally take almost anything you own and sell your belongings to pay off the tax debt.

IRS Collections Levy Notice

Though the term levy does apply to the actual acquisition of assets, the IRS places a levy by simply serving notice that it intends to take your assets at a future time. The Fifth Amendment of the U.S. Constitution states, “No person shall be … deprived of life, liberty or property without due process of law.” In the case of tax levies, due process requires the IRS to notify the taxpayer at least 30 days in advance. It must also give the option to request a hearing during that time frame to challenge the levy. If no hearing is requested or if the challenge fails, then the IRS has fulfilled its due process requirement and can seize the assets at the end of the 30-day period.

Asset seizure

Personal property that the IRS can seize and sell to pay off your debt includes but is not limited to:

- Cars

- Boats

- Luxury items

- Homes

- Businesses

- Vacation properties

- Other types of real estate

Possessions protected from seizure

There are only a few personal belongings that the IRS is not allowed to seize. The only personal property that taxpayers are guaranteed to keep regardless of the situation include:

- Necessary clothing

- Necessary school books

- Up to $6,250 worth of food, fuel, furniture, and personal effects

- Up to $3,125 worth of tools and books that are necessary for earning a living

- Undelivered mail

The good news is that asset seizures are a last resort method that is rarely used.

Bank levies

Because of the potential difficulties in seizing physical assets, the Internal Revenue Service prefers to seize financial assets. Besides being easier and safer to take, they provide instant cash without the hassle of finding a buyer. The seizure of a financial asset is often referred to as a bank levy. However, bank levies are not limited to the money you keep in a traditional bank. There are many types of financial assets the IRS can seize including your bank accounts, social security benefits, and more:

- Checking accounts

- Savings accounts

- Pensions

- 401(k) accounts

- Stocks and bonds

- Cash value of life insurance policies

- Social security benefits and retirement income

Wage garnishment

The ability of the IRS to take your assets is not limited to what you currently own. The agency can also place a levy on your future assets via wage garnishment if you owe tax debt and cannot pay in full.

Wage garnishment is when the IRS takes money out of your paycheck to pay off the debt over a period of time. With this collection tool, your employer is required to pay the IRS each pay period and deduct the amount from your take-home pay. The garnishment continues until the entire debt is paid. The amount that the government takes out of each paycheck can be significant and depends on how much you owe. The IRS will leave you enough income to pay for basic living expenses.

How much can the IRS take from paychecks?

In the most extreme cases, wage garnishment allows the IRS to leave the taxpayer with little more than $180 per week. The agency does not take into account what your living expenses actually amount to and may leave you without enough income to pay your other bills.

Wage garnishment can continue for years

Unlike other levies, the wage garnishment is not a one-time event. Though they only have to provide due process once, the IRS can seize money from dozens or even hundreds of your paychecks. The wage garnishment continues for as long as is necessary until the IRS is satisfied that you have paid in full. Often that requires the wage garnishment to continue for years.

Tax penalties

Tax penalties and interest are mostly financial in nature and require individuals to pay more to the IRS than what they actually owe in taxes. However, there are also instances where the IRS may go beyond simple interest and fines and pursue criminal prosecution and jail time. There are several actions (or inactions) that the IRS may penalize you for including:

- Failing to file a tax return

- Failing to pay taxes or paying less than what is owed

- Filing inaccurate tax returns

- Negligence or a lack of effort in complying with tax rules

- Tax fraud or intentionally underpaying taxes

- Failing to pay penalties and interest on unpaid taxes

How to avoid being a target of an IRS audit

If you don’t want to become a target of the IRS, keep in mind a few of the factors that can trigger an IRS audit and start the IRS collection process:

- Filing a late tax return

- Lacking the ability to pay the entire balance due

- Not paying IRS tax penalties

- Not reporting all sources of income

- Claiming deductions for which you have no proof or receipts

- Leaving a tax issue from a previous year unresolved

- Not responding to a prior notice from the IRS

What should you do if you are contacted by the IRS?

If you receive phone calls or letters from one of the IRS collections departments, take them seriously. The IRS can literally take everything you own and destroy your credit score and credit report. Even if you can’t afford to pay your taxes, continue filing your tax returns and maintain good communication with the IRS. Contact the IRS if you have any questions or concerns about your tax debt.

How to stop the tax collection process

The good news is that no matter how bad you think your situation is, it can help to have a tax relief company on your side. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee, and charge competitive rates. They can help you do all of the following and more:

- Find payment options

- File an installment agreement request

- Help restore your credit rating by making payments on time

- Offer other helpful tax payment information

- Reduce or eliminate future collection action

Check out which tax relief company is the best fit for you.

Can I get help even if I owe a significant amount of money?

If you owe $10,000 or more in back taxes and cannot pay in full or you are facing a tax audit, it is probably in your best interest to hire a tax attorney. They may be able to reduce the amount that you owe, set up alternative payment options, or negotiate an installment agreement for you. Even if you decide to deal with the IRS by yourself, it’s a good idea to consult with a tax professional to gain more information. SuperMoney’s tax relief comparison tools make it easy to see which attorneys offer the best terms.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: