Lease a Car With No Credit or Bad Credit

HA

Summary:

It’s not easy, but it is possible to lease a car with poor or no credit. For instance, you could get a cosigner or even take over an existing lease. However, there are other options that are also worth considering if your credit is not where it needs to be to qualify for a lease.

For business owners, people who don’t want the hassle of car maintenance, or if you can’t afford to buy the car you want outright, leasing a car may be a good option. This way, you can make regular payments to an auto dealer and start driving immediately. Some people lease used cars to save even more money. But what if you have the money but not the credit score to lease a car?

Unfortunately, it can be difficult to lease a car if you have a bad credit score. You don’t need a perfect credit score, but most companies require it to be relatively high. In the first quarter of 2021, the average credit score among people with leased cars was 710. Since the benchmark for a good credit rating is 670, leasing is a struggle for many people after a credit check. Is there a way to lease a car even with a poor credit score?

Get Competing Auto Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

How credit affects car leasing

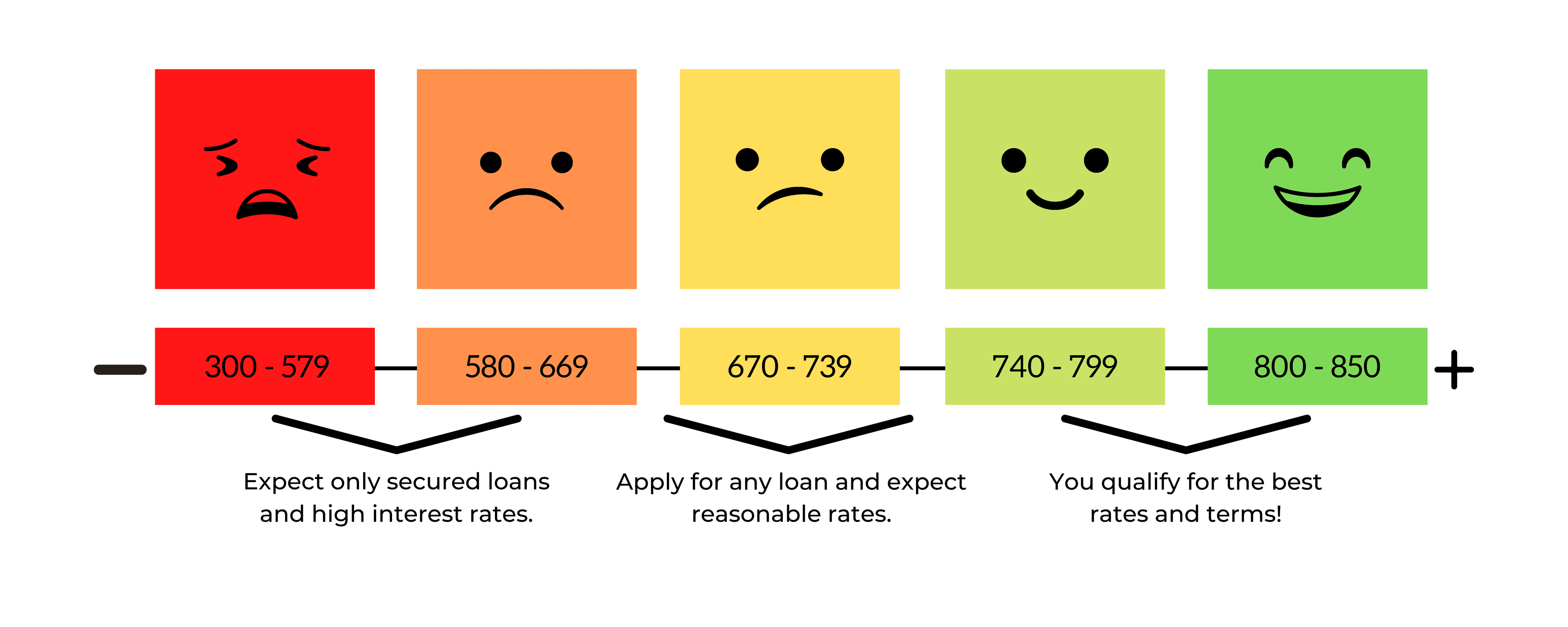

Credit scores in the U.S. range from 300 to 850. An ideal credit score is above 670, while the most exceptional scores are from 800 upwards. Unfortunately, not everyone can achieve that easily. According to recent credit data, only a little over 20% of Americans have credit scores above 800.

People with good credit scores typically pay low interest rates on their car loans. In some cases, these people qualify for 0% financing. On the flip side, people with bad credit scores pay higher rates and may have to put down a larger down payment. Lenders tend to see people with low credit scores as high-risk candidates, so they try to recoup their money as quickly as possible.

What is a credit check?

A credit check is when lenders check a potential leaseholder’s credit report to determine how much of a potential risk they are. In vehicle financing, the car dealership checks your credit history with any of the major credit bureaus. Oftentimes, a lender will perform a hard credit check, which slightly damages your credit score temporarily.

There are three major credit bureaus in the U.S. — Experian, TransUnion, and Equifax. These companies get monthly loan updates for millions of people, which show a snapshot of how people pay back their loans. When you apply with a dealership, they get a copy of your credit report and review it.

What is a credit history?

Simply put, a credit history measures a person’s debt record and contains information like:

- The number of open or closed accounts tied to a person

- The account types — revolving credit or installment credit

- The amount of money owed on each account

- A repayment history

Keep in mind that your credit history is a major component of your credit report and score. Early repayments help your credit history, while breaking a lease tends to be more damaging.

How car dealerships group people by credit rating

Dealerships typically group people into the following categories based on credit score:

- Ideal vehicle financing. These are people with excellent credit scores above 720. They are in a great position to negotiate the terms of their leases because they’re the types of clients that most lenders want.

- Prime vehicle financing. These people have a credit rating between 670 and 719. They might have as much negotiating power as the ideal leases, but they’ll most likely have their lease requests approved and get a sweet deal.

- Near-prime financing. This applies to people with credit scores between 620 and 669. If you fall within this bracket, you’ll probably get your lease request approved at higher-than-average interest rates.

- Subprime auto financing. People who fall below the minimum credit score of 620 qualify for subprime auto financing. You might find a dealer who’s willing to give you a lease, but you’d also pay much more than the average lease rates. You might also have to put down a security deposit.

No credit check auto loans

If you were denied an auto loan because of your poor or lack of credit, you may consider looking for lenders that accept borrowers with poor credit. Instead of relying on your credit history, these loans use other information to determine your trustworthiness in paying back the loan. For instance, you may have to provide employment paperwork, pay stubs, utility bills, bank statements, and your driver’s license.

You may hear no credit check auto loans referred to as “guaranteed auto loans.” Unfortunately, just like “no denial” payday loans, this name is misleading, as each lender will have different lending requirements you must meet, and they all will check your credit unless you are providing a deposit or security that is worth more than the loan.

How to lease a car with bad credit or no credit history

The good news is that no credit check auto loans aren’t the only option if you don’t have the best credit. There are ways to lease a car even with bad credit.

1. Improve your credit

The first and most obvious option is to wait on leasing a car until you’ve improved your credit. You can do this by:

- Paying down your debt

- Making consistent timely payments on your current loans

- Ensure your credit report is accurate

Though it may take some time, building good credit habits and ensuring your credit report does not contain any false information can significantly help build your credit.

If you believe your credit report contains errors, try speaking with a credit repair company. They can do the hard work of communicating with the credit bureaus and ensure your score reflects your proper spending habits.

2. Make a higher down payment

Another great way to get auto loans with poor credit is by making a high down payment. This also saves you some money in the long run. Also known as capitalized cost reduction, this option is especially attractive for people with no credit history.

By making a huge down payment, you can reduce your car lease amount and by extension, your monthly payments. The challenge with this option is that down payments come with restrictions depending on the loan company or dealership.

3. Take over an existing lease

Instead of going through the leasing company, you could take over someone else’s lease. This option usually comes when the existing leaseholder is at risk of defaulting. People in this position would most likely transfer their lease since the delayed monthly payments could hurt their credit score.

Car dealerships are usually more open to working with you when they know that you’re taking over a car lease and willing to pay them. So while lenders may be more lenient, you’ll probably still be subject to credit checks.

4. Get a cosigner on the lease agreement

The cosigner option is another viable route for people who have poor credit. If you have a family member or a friend who has strong credit, you could get them to cosign your car lease. This convinces the dealership that your auto loan or lease will be paid off even without a perfect credit history.

The only challenge here is that your cosigner becomes financially responsible for your monthly lease payments if you’re unable to meet up. So, before you saddle them with this responsibility, ensure that they know what they’re getting into.

Pro Tip

It’s important to get a cosigner with a credit score of at least 670. This increases your chances of securing the lease.

5. Qualify for discount programs

Another interesting option is to find a discount program that helps you save money on a car rental, loan, or lease. Some car manufacturers and leasing companies offer incentives, bonuses, and discount initiatives. These incentives encourage qualified customers to enjoy some payment discounts. If you fit the bill, you could save hundreds of dollars.

A great example is AAA. Apart from offering car repairs, they’ve also partnered with several car rental providers to offer discounts on rentals and leases. Look for offers like these and find out how to qualify, and you could enjoy savings on your next auto lease.

Alternatives to leasing

Although leasing can be an option for people with bad or no credit, it’s not for everyone. Here are some alternatives to consider.

Buy a car and shop around for your best rate

Regardless of your credit score, it’s important to shop around and compare auto loan options. Several lenders offer auto loans specifically for car leases, which means you could save even more money by ensuring you get the best deal.

Keep in mind that some lenders may be more willing to work with lower credit scores than others. The tool below currently shows lease financing options for users with a credit score of 669 and under, but you can modify searches by adding your own credit score.

Trade in your car

This involves selling your car to the dealership and offsetting part of the cost of the new car. You may hear this practice called “part-exchange.”

Think of part-exchange as selling your car directly to a dealer. The only difference is that instead of getting hard cash for the car, you get to pay less money for the new one.

But, it has its risks. Generally, the amount you save on a part exchange will depend on what the car dealership believes both cars are worth. So, you have to be careful to ensure that you get a good deal.

Buy a car with a subprime loan

There are many subprime lenders that offer bad credit auto loans for people with bad or no credit history. Unfortunately, this financing option has several downsides.

Not only will these lenders require a higher down payment, but you’ll also be subjected to much higher interest rates, sometimes up to 20% higher. Your lender may also include adjustable interest rates, which means your interest rates may increase depending on the current market. All of that is in addition to a longer repayment period, meaning you’ll pay considerably more in interest.

IMPORTANT! If you already have a car and you want to lease a car with no credit check, this is one alternative to no credit check loans.

FAQs

Can I lease a car with a 500 credit score?

Yes, leasing a vehicle with a 500 credit score is possible. That being said, you’ll most likely pay higher interest rates.

What credit score do I need to get a lease car?

Ideally, you need a credit score above 670 for decent financing options with good interest rates.

Is it difficult to lease a car with bad credit?

You’ll likely have a difficult time leasing a car with poor credit. However, that doesn’t mean it’s impossible. Instead, you may have to pay a larger down payment or have a higher interest rate.

Does leasing build credit?

As long as your payments are on time and your leasing company reports it to the three credit bureaus, leasing a car can build your credit score.

Key Takeaways

- You can lease a car with bad credit or no credit history.

- Credit reports help financers check your risk level and determine your creditworthiness.

- The higher your credit score, the better your chances of getting great lease terms for a new car.

- If you have bad credit, you’ll most likely pay higher interest rates on your auto loan.

- Even if you have poor or no credit, there are several options available to you. You can get a cosigner, take over someone else’s lease, or make a larger down payment.

Share this post: