How to Pay Medical Bills Without Going Broke: 3 Steps to Cutting Costs

TP

Last updated 04/09/2024 by

TJ PorterYou recently had an important medical procedure done, but now you’re stuck with a hefty bill that you can’t afford. If that sounds familiar, you’re not alone.

A recent survey conducted by Kaiser Family Foundation and New York Times revealed that 26% of working-age Americans struggle to pay medical bills. Even worse, 63% of respondents who had health insurance (and 51% who were uninsured) exhausted their savings accounts to cover medical costs.

So, should you wipe out your savings account or ignore the bill altogether? Neither is the best option.

Follow these three steps instead.

End Your Credit Card Debt Problems

Get a free consultation from a leading credit card debt expert.

It's quick, easy and won’t cost you anything.

What to do when you get a medical bill

Medical billing is very confusing for many people. This is often by design. If you don’t understand the details behind the cost of services and other expenses, you are less likely to complain and ask for explanations. Here are three steps you can take to handle your medical debt account and protect your credit

1) Review your medical bill and look for errors

Medical providers process tons of claims, so mistakes are bound to happen. “Billing errors are common, and the most expensive error for patients is when [they] are billed an “out-of-network” charge,” says Dave Matli, Vice President of Marketing and Product UX for Parasail Health.

Billing errors are common, and the most expensive error for patients is when [they] are billed an “out-of-network” charge”

But there’s a number of other errors to look out for as well. If these mistakes go undetected, your hospital bills could be much higher than they should be.

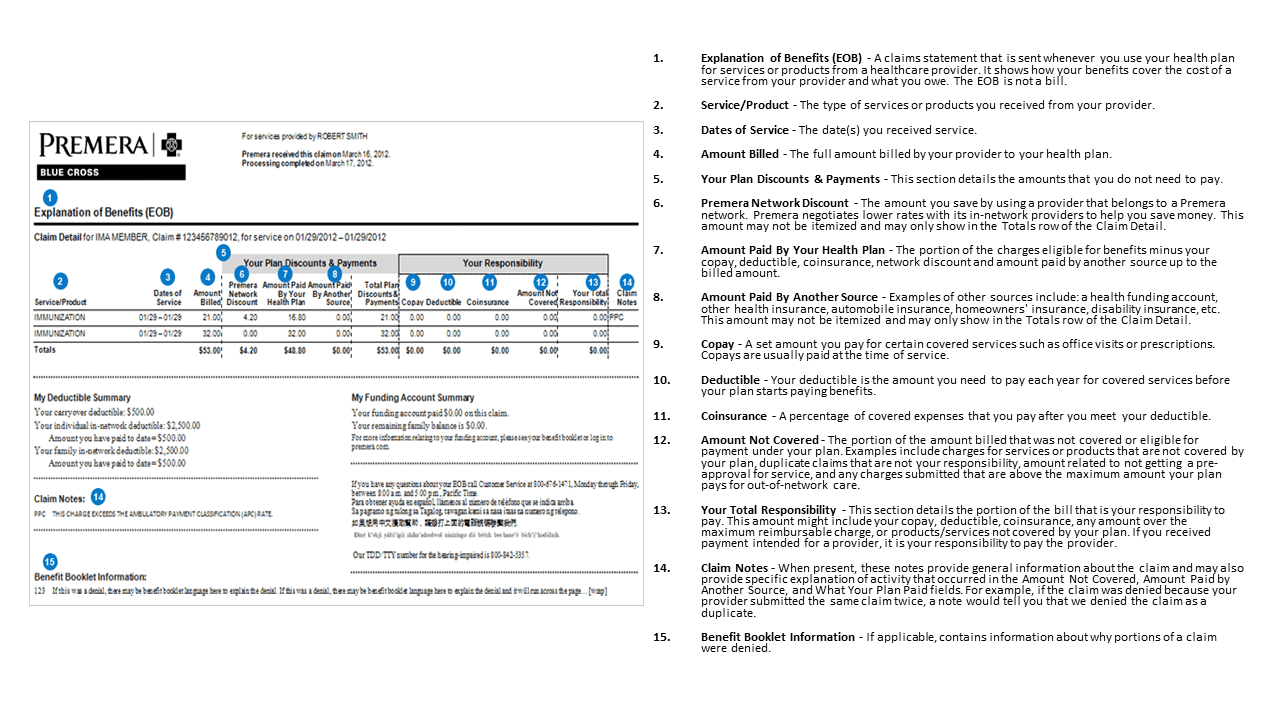

To identify possible billing mistakes, review the explanation of benefits (EOB) document and call the hospital’s billing department.

The billing department can conduct a detailed review of your statement. In doing so, you may find that you owe less than what the bill states due to a coding issue. There’s also a chance that your insurance company made an error when processing the claim.

Explanation of Benefits (EOB) document

Your insurance company will send you an Explanation of Benefits (EOB) after you’ve received a service for which they’ve paid. This document will detail the cost of services rendered, the amount paid by your insurance, and the remaining balance you’ll need to cover.

You’ll want to carefully review the EOB to ensure there are no mistakes, such as:

- Additional services that you did not receive.

- Being billed twice for the same service, resulting in your insurance rejecting one of those claims.

- Getting billed for the wrong diagnosis and

- Paying an incorrect coinsurance amount due to miscalculations made by the doctor’s billing company.

- Falling victim to insurance fraud and medical identity theft.

- Health care products you’ve been billed for but did not receive

Contact your provider immediately if you spot errors. It’s also a good idea to compare the EOB to the bill to ensure the amounts listed are the same.

If you don’t receive an EOB within eight weeks after a doctor’s visit (for any reason), make sure you call and request it.

2) Don’t ignore your medical bill

Most medical providers aren’t looking to throw you to the collection wolves if you can’t pay the bill all at once. But that doesn’t mean you should sit on the bill until the collection agencies start calling.

Ignoring your bill does NOT mean collection agencies will ignore you. In fact, the opposite is true.

You’ll have to pay your bill one way or another. If you don’t, or if you consistently make late payments, your credit will drop. Dealing with collection agents can be very stressful, but you can often lower your debt or even get canceled if you negotiate with your service provider before you default on your medical bill.

3) Negotiate for a reduced price

Many medical providers will consider giving a discount under certain circumstances. You can negotiate your way to a reduced bill if you prove that you fully intend on paying it but that it’s going to be difficult for you to pay the entire amount.

Don’t wait to contact your medical provider, though. The longer you wait, the less willing they will be to help you.

The sooner you contact them and prove your willingness to settle your debt, the more open they will be to working with you and negotiating a lower price.

Negotiate a settlement

You can request a settlement if you have cash on hand. According to Gross, “This can often be completed by negotiating the allowed, usual, reasonable, and customary amounts per procedure codes with the medical provider.”

If you offer to pay the balance right away, the provider may be more willing to give you a reduced price. If they deny your request, don’t give up. Plead your case to management to see if you can get better results.

Request a payment plan or financial assistance

If you find it impossible to afford the bill, the best thing to do is immediately contact the billing department to request a payment plan or financial help. You can ask them to stretch the payments over a longer period to make it more affordable.

If you need financial assistance, prepare to provide supporting documentation.

“The medical provider may request financial information, such as bank statements and prior year tax returns, to prove [your] inability to pay [your] medical charges,” notes Adria Gross, founder of MedWise Insurance Advocacy.

What is Medical Debt?

If you go to the hospital but can’t pay the bill, those health care bills turn into medical debt. Medical debt is especially tough to deal with because, unlike credit card debt or other forms of debt, medical debt is something you can’t avoid. Your health is most important, so you shouldn’t put it off because of healthcare costs.

The American medical system is complex, and health care can get very expensive quickly if you don’t have health insurance. If you don’t make your bill payments, you’ll wind up with medical debt to the hospital or health care facility. The hospital may eventually sell that debt to a collections agency.

How to Pay Off Medical Debt

If you’ve found yourself in medical debt,

Focus on your health

When your medical bills are piling up, it can lead to a lot of stress. If you already have medical debt and don’t have health insurance, you might be tempted to put off a visit to the doctor or the hospital because you feel like you don’t have the money to pay for health care.

Even if you have medical debt, it’s important to stay focused on your health. If you ignore small aches and pains, those could be symptoms of larger problems. By waiting to get them checked out by a health care provider, you might be turning a small problem into an even more expensive health issue, like emergency surgery, down the road.

Design a repayment plan

If you’re in a position where you can afford to pay your medical debt, you should do your best to make those payments. Ignoring the debt will damage caused those missed payments to show up on your credit report and damage your credit score.

Design a repayment plan that will help you pay the debt off as quickly as possible. If you can afford to pay more than the minimum amount required each month, you should do that, especially if the interest rate is high. If you’re already paying more than the minimum on other debts, like student loans or credit cards, check which of your debts charges the highest interest rate and prioritize that one. This will help reduce interest charges.

Build a budget and stick to it

If you don’t already have a monthly budget, building a budget and sticking to it is a great way to make it easier to deal with your bills. You may have enough money coming in to pay all of your bills but not know it because you don’t know where your money is going.

When you first build your budget, spend a month tracking every dollar that you spend. This will give you a baseline idea of how you spend your income. You may find that you’re spending more than you expected on things that aren’t necessary, like buying lunch at work.

Once you know where your money is going and how much you have leftover at the end of each month, you can make more conscious decisions about using your money in the future. For example, you might decide to bring lunch to work instead of buying it, putting that money toward paying your bills.

One popular way to budget is using the envelope method. Take cash out of your bank and place it in envelopes for each category of spending in your budget. For example, you might put $250 in the grocery envelope and $100 in the gas envelope each month. When the envelope is empty, you’re out of money for that type of spending.

You can easily see the envelope growing empty as you use the money, giving you a clear indication of how well you’re sticking to your budget.

Those who prefer digital methods can use online budgeting tools. With these, you provide your bank account information and link your debit card to a website. The site automatically tracks your spending for you.

Keeping asking for help

When you’re dealing with medical debt, it can feel like everyone is out to get you. In truth, most doctors, hospitals, and health care professionals aren’t looking to trap you in a spiral of debt. If you don’t get help when you first ask for it, be persistent and keep asking.

You can continue working with the medical billing office at the hospital where you received care to ask about repayment plans or other options for dealing with your medical bills. Your health insurance may also be able to assist you if you’re having trouble paying a deductible.

You can also enlist the help of a patient advocate. These people are experienced in dealing with the health care system and can serve as partners, giving you tips about handling medical bills. They also help advocate for you to get the care you need or to reduce the cost of your care.

How to Deal With Medical Debt Collectors

If you ignore your medical debt, it might wind up in the hands of a debt collector. These collectors can be relentless with their calls and demands for payment. If you start getting calls from a collection agency, here’s what you should do.

Know the law

The most important thing to do when you start getting calls from debt collections is to make sure you know your rights and know the law. Federal and state law places a lot of restrictions on debt collectors and how they can contact you.

For example, in Massachusetts, a collector can’t call you more than twice in a seven-day period for any single debt, before 8 AM or after 9 PM.

Depending on where you live, you may be able to stop the calls by demanding they only speak to a lawyer or demanding that the collector send you proof of that debt.

Understand what you owe

Collections agencies will often use whatever tactics they think will get you to pay your debt. They may also inflate the amount that you owe with additional interest charges and fees.

Make sure you know exactly what you owe, and before agreeing to pay anything, demand that the debt collector prove that they own the right to collect your debt, that you truly owe the debt and the amount that you owe.

If the amount you owe doesn’t match your hospital bill or most recent billing statement, find out why. You might be able to save some money that way.

Don’t be afraid to negotiate

When a hospital billing department sells debt to a collection agency, it usually sells that debt for pennies on the dollar. If you owe $10,000, the hospital might have solid it for $500 or $1,000, so to the debt collectors, you making any payment above that amount is a win.

Even if you weren’t able to negotiate with the medical billing department at the hospital, try to negotiate with the debt collectors. You might be able to save a lot of money. Make sure to get any agreement in writing before you pay to ensure that the collectors don’t come after you for more money.

Frequently asked questions about medical debt

These are some frequently asked questions about how to deal with medical bills and medical debt.

How can I get my medical bills forgiven?

The best strategy for getting a medical bill forgiven is to work with the hospital billing department. Federal law requires that non-profit hospitals have some type of financial assistance program for patients who can’t afford their health care expenses. According to the National Consumer Law Center, about half of all states have similar programs and written requirements as to which patients should have access to discounted care.

How long do I have to pay medical bills?

When you get a medical bill, it should come with a due date listed. If it doesn’t, you should call the hospital to find out when the bill is due. Typically, you’ll have about thirty days from the time that you get the bill to the time you have to make your first payment.

If you expect that you’ll have trouble paying your medical bills, you shouldn’t delay. Reach out to the billing department as soon as possible to let them know your situation. They may be able to set up a payment plan or work with your insurance, such as by changing how they billed you based on your insurance policy to reduce the amount that you owe.

Does medical debt qualify for bankruptcy?

Yes, if your health care costs put you deep into debt and you aren’t able to repay your debts, you do have the option of declaring bankruptcy.

Bankruptcy allows you to get out of your debts and to get a fresh slate financially. However, bankruptcy can be a long and painful process. At a minimum, your credit score will take a major ding. It can take years to improve your credit health to the point where you can qualify for a loan.

What happens to medical debt when I die?

Few adults like to think about it, but if you’re dealing with expensive medical care, you may have to deal with tough topics like facing the idea of your own mortality.

When you die, you leave an estate that holds all of the money, property, and stuff you owned. The executor of your estate is responsible for managing the estate and using its resources to pay off all of the debts you owed, including any outstanding medical bills.

If the estate has enough money to pay the debts, your heirs can inherit the remainder of the estate.

Depending on the circumstances and where you live, your spouse may be responsible for paying your medical bills after you pass away. For example, if your spouse cosigned on a loan or credit card, they are fully responsible for paying that loan or card. If you live in a community property state, your spouse may also be liable and have to pay the medical bills you incurred.

It’s a good idea to work with a legal expert to determine who will be responsible for what debts if you pass away.

Can you use a credit card to pay medical bills?

Yes, in many cases, it is possible to use a credit card to pay your medical bills. However, that doesn’t mean it’s a good idea. Credit cards have much higher interest rates than many other types of debts, making credit cards a costly way to borrow money.

With medical debt, there are other options for dealing with the costs of health care. You’ll be better off working with the health care provider to design a payment plan that fits your budget.

Conclusion

If you need emergency health care, the last things you’re probably thinking about are the medical bills you’ll receive, but those medical bills can quickly turn into medical debt if you don’t have the money to pay them. These tips can help you understand the situation you’re in and get help with dealing with health care costs.

Share this post: