Mortgage Rates: A Guide On How They Are Calculated

AL

Last updated 04/08/2024 by

Andrew LathamFact checked by

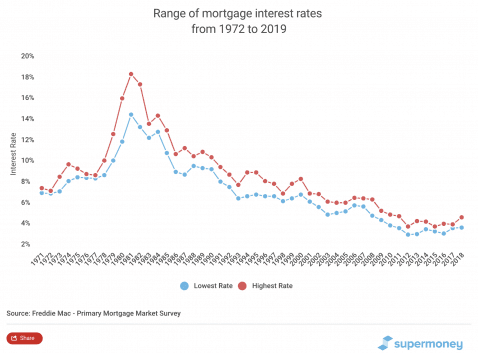

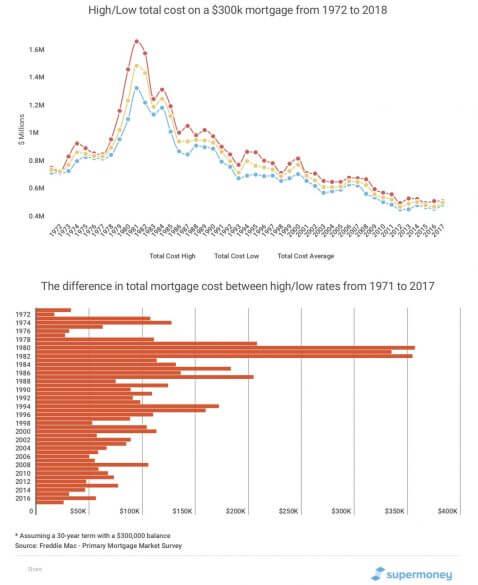

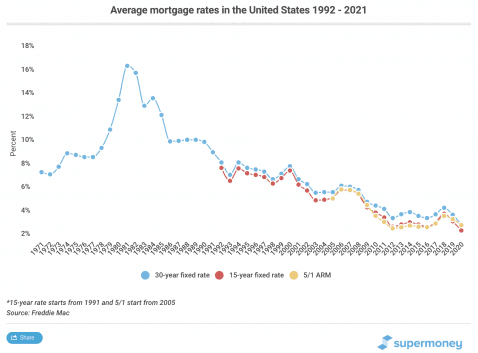

Shopping around and comparing mortgage rates from multiple lenders can save you a lot of money over the life of a loan. Last year’s range of interest rates, according to Freddie Mac’s Primary Mortgage Market Survey, went from 3.89% to 4.30%. That is a particularly narrow spread when compared to other years. However, it represents a $25,678 difference over the life of a $300,000 mortgage with a 30-year term.

The year with the most dramatic spread was 1980, which had a 4.17% difference between the low and high mortgage rates. Using that spread and the same $300,000 mortgage, the difference in total cost over the life of the loan would exceed the principal of the mortgage: $356,968.

The graph below shows the difference in total cost between the high and low rates and the average total cost.

Mortgage rates, monthly payments, and the importance of applying with several lenders

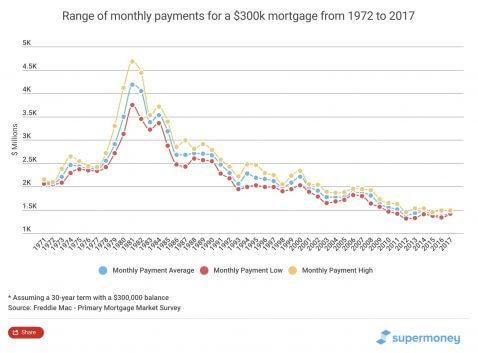

The interest rates on your mortgage will determine whether the monthly payments of a mortgage are affordable. For example, in 2008, monthly payments varied by nearly $300 depending on whether your mortgage rates were on the high or low end of the spectrum.

It’s clear that shopping around for the lender with the best possible rate is a good investment of your time. However, most people only check their rates with one lender.

A recent study published by the Consumer Finance Protection Bureau found that half of the people who got a mortgage considered more than one lender or mortgage broker before they applied. But 77% stopped shopping after they applied with one lender.

Going with the first lender you happen to apply with is not a good idea. Rates and fees vary significantly from one lender to another. Comparing rates and terms from several lenders could save you hundreds of thousands of dollars. The savings are even more dramatic if you bought your mortgage when interest rates were high and you can refinance it at lower rates. SuperMoney’s mortgage comparison tools make it easy to compare the rates and terms of leading mortgage lenders.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

The importance of understanding how mortgage rates work

Mortgage rates can vary dramatically based on the type of mortgage you choose, how much you borrow, your credit score, and the points you decide to pay. It is important to understand how mortgage rates work if you want to get the best deal possible.

Home mortgage rates come in two basic forms: fixed-rate and adjustable-rate. Understanding the difference is the best way homeowners can make an informed decision about which type of mortgage is right for them.

For first time homebuyers (and those who need a refresher), our first-time home buyer guide is a valuable resource.

Fixed-rate mortgages

The greatest benefit of a fixed-rate loan is that the interest rate and the monthly payment remains the same throughout the life of the loan. The amount of interest and principal will vary from month to month due to amortization. Because the mortgage interest rate is fixed, changes in the market have no effect on your loan.

How long are fixed-rate mortgages?

Typical fixed-rate loans traditionally have a repayment term of 30 years. Borrowers who refinance or want to accelerate their loan payoff often choose terms of 10-, 15-, or 20-years. Some lenders allow 40- and 50-year terms for borrowers who are stretching their budget to afford a home.

How does loan amortization work?

The most common fixed-rate home mortgage is a 30-year loan. This loan will amortize over thirty years. Amortization is simply the act of paying off your debt in regular installments over a set period. With any amortizing loan, in the beginning, a big portion of your loan payment will be interest on the balance. A small portion pays down the balance each month. As the loan balance decreases, there is less interest charged and more of your payment goes towards paying down the loan balance. Towards the end of the loan term, your monthly payments primarily pay off the principal.

Because fixed-rate loans interest rates are locked for the term of the loan, the interest rates are generally higher than adjustable-rate mortgages. Borrowers pay extra for peace of mind in case interest rates rise in the future.

Adjustable-rate mortgage (ARM)

Adjustable-rate loans typically offer a lower initial interest rate for a set number of months or years. These loans are often referred to as variable-rate loans.

In addition to a lower initial interest rate, ARMs are generally easier to obtain than fixed-rate loans because the payment starts out lower. Due to changes in Federal laws, mortgage lenders are now required to underwrite applicants based on their “ability to repay.”

Will my mortgage payment change?

Unlike fixed-rate mortgages, the interest rate fluctuates with the market. The change in interest rates will cause your monthly payment to change as well. Depending on the direction of interest rates, your mortgage payment may go up or down.

Because the initial interest rates reset after a specific timeframe, they are often called “teaser rates.” Common initial teaser rate periods are 2-, 5-, 7-, and 10-years.

After the teaser rate expires, the rate will reset on a pre-determined schedule. Some interest rates reset every month, while others reset on a quarterly, semi-annual, or annual basis.

Your lender is responsible for providing you with this information. Margins usually differ from lender to lender, so you’ll want to shop around.

How are ARM mortgage rates calculated?

Your mortgage interest rate is comprised of two pieces – the rate index and the margin. The rate index is most of the Prime Rate or a variation of LIBOR. As these indexes go up and down based on the market, your mortgage rate will change. Your margin is the rate added to the index. The margin will not change throughout the life of your loan. For example, if you have a 6-month LIBOR with a 3.25% margin and the 6-month LIBOR is at 1.25%, then your mortgage rate will be 4.50%.

Is there a cap of how high my mortgage rate can increase?

Yes. Adjustable-rate loans have two caps. The first limits how much your rate can change at any one time, up or down. The second cap is a lifetime cap that limits how high your interest can go.

If your index rate went to zero, then the lowest your mortgage rate can go is the margin.

Know this before you sign up for an ARM mortgage loan

Due to the uncertainty of an adjustable-rate loan, be sure you know:

- How long the current interest rate applies.

- What the new interest rate will be.

- How often the interest rate adjusts.

- The maximum amount your monthly payment could increase.

- The payment cap.

- If there are any penalties for paying the loan off early.

What are points on a mortgage?

If you are shopping for a mortgage and you’re comparing interest rates, you have probably heard about points. Points are a percentage of a loan amount. For example, a point on a $300,000 mortgage is $3,000 ($300,000 x 0.01). Two points would be $6,000.

The trade-off between points and origination fees

Lenders will change the interest rates they offer on a mortgage depending on how much you are willing to pay in points. Pay a point at closing and your lender may drop your rate by 0.25%. Of course, this will increase your upfront costs when closing on a mortgage. To illustrate, let’s say you pay a point (1% of the loan amount) on a $300,000 mortgage. In turn, the lender agrees to drop the mortgage rate from 5% to 4.75%. This will cost you $3,000 more at closing, but you will save $45 every month in interest payments. Over the life of a 30-year mortgage, you would save $16,388.

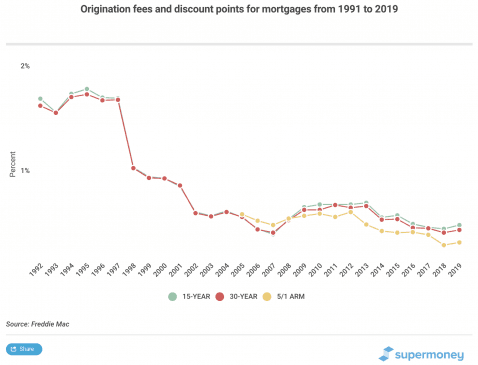

Paying points on a mortgage can make good financial sense if you plan to keep your mortgage for a long time and you have the cash to spare at closing. The cost of mortgage points and origination fees has changed significantly over the years.

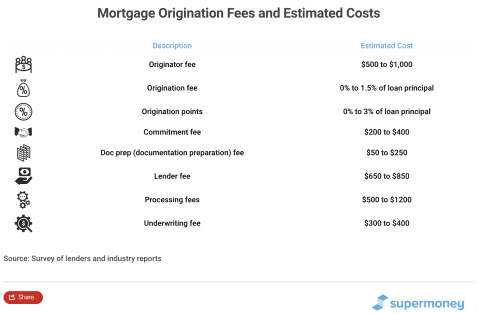

What is an origination fee?

Origination fees are costs a lender charges to cover the expense of processing a loan. As well as covering the overhead of the lender, some of the fees are paid to third-party providers, such as home inspectors and property assessors.

Other types of home mortgages

There are other types of mortgages available, but they are less commonly used. These include:

- Interest-only mortgage: Unlike traditional mortgages where you pay both interest and principal, with an interest-only mortgage you pay only the interest for a certain number of years. Then at a specified point, you start paying both.

- Graduated-payment mortgage: A fixed-mortgage with a gradually increasing payment.

- Option-ARM mortgage: borrowers are presented with options each month. They can pay based on a 30-year amortization, 15-year amortization, interest only, or an amount less than the interest charged. When borrowers choose the 4th option, the unpaid interest is capitalized (i.e. added to the loan balance). When this happens, it is called a negative amortization mortgage because the loan balance is increasing each month.

- Balloon-payment mortgage: Because the loan amount is not fully amortized, a large balance – known as a balloon-payment – is due at the end of the loan.

- 203K mortgage: Related to the Section 203(k) program run by the federal government for single-family properties that require repair and rehabilitation.

For more information about the types of mortgages available, read our in-depth mortgage guide.

What is the best mortgage loan for you?

Choosing the best mortgage loan for you will depend on many factors, such as the current housing market, the direction of interest rates, and your personal situation.

Start by answering these questions:

- How long do you plan to keep the home?

- What is the current market for interest rates and home loans?

- Does your income allow for fluctuating interest rates?

- How much can you afford to borrow?

A mortgage professional will help you answer these questions. Before picking a lender, shop around and compare rates and terms. Do your research. Read user reviews on your top choices to see what their customer service is like. Then consider all your options before you make a commitment.

If you’re still having trouble selecting a mortgage lender, our comprehensive guide to choosing a mortgage lender will help.

AL

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post: