Roth IRA vs. 529 Plan: Which Should You Use to Save for College?

BL

Last updated 03/19/2024 by

Ben LuthiCollege tuition and fees alone cost $32,088 for four years at a public university, according to the U.S. Department of Education. Go to a private university instead, and it could cost you upwards of $100,000, and that’s not even including room and board, supplies, or textbooks.

And if your child is still in diapers, you can expect to pay a whole lot more than that by the time they’re ready for school, with tuition inflation regularly outpacing general inflation.

As you consider how to save for your child’s education, you’ve probably come across 529 plans. These college savings plans make it possible for you to save for future college costs with tax-free growth.

But depending on your situation, you might also want to consider using a Roth IRA.

Compare Investment Advisors

Compare the services, fees, and features of the leading investment advisors. Find the best firm for your portfolio.

Roth IRA vs. 529 plan: Learn the pros and cons of each

If you want to know which of these options you should use to save for the future, it’s important to know both the benefits and drawbacks of using each. Here’s a break down to help you.

Pros and cons of Roth IRAs

Pros of Roth IRAs

A Roth IRA is a retirement account that allows you to grow your investments on a tax-free basis. But with the way the account is designed, you could also use it to pay for college costs.

Flexibility

With this account, you can set aside cash for your child’s education. If they get a scholarship or decide not to go to school, you can keep the funds there for retirement.

This is possible because of the way these accounts are designed. For starters, you can make tax-free and penalty-free withdrawals up to the amount you’ve contributed to the account.

And if you need to withdraw some of the earnings beyond your principal amount for education expenses, you won’t pay the 10% penalty you’d typically incur for early withdrawal before age 59 and a half.

Investment options

Depending on where you get a Roth IRA, you could have a large number of funds in which you can invest your money. It’s also easy to choose a Roth IRA provider with low fees. This is important if you anticipate also using your Roth IRA to save for retirement.

Won’t hurt financial aid eligibility

When your child applies for financial aid in college, the U.S. Department of Education will consider your assets when determining whether he or she needs aid. The good news is that all the money in your Roth IRA is excluded from this calculation so that it won’t work against you.

Cons of Roth IRAs

While the benefits of a Roth IRA sound appealing, it’s important also to know what’s on the other side of the coin.

Contribution limits

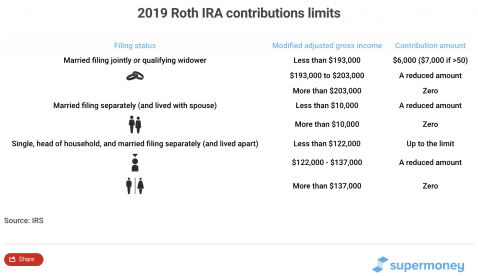

A Roth IRA only allows you to contribute up to $6,000 per year (2019) — or $7,000 if you’re 50 years old or older. The limit was $5,500 and $6,500 from 2015 to 2018. While that may be enough for some colleges, it might leave a shortfall if you have your eyes set on a costly college.

Also, it may not be enough if you want to use the account to save for both education and retirement. What’s more, your contributions may be limited if you make over a certain amount.

Here’s a quick summary of these limits for the 2019 tax year.

| Filing Status | 2019 Modified adjusted gross income (MAGI) | 2018 | Deduction Limit |

|---|---|---|---|

| Single Filers | $64,000 or less | $63,000 or less | 100% deduction |

| $64,001 to $74.000 | $63,001 to $72,999 | Partial deduction | |

| $74,000 | $73,000 or more | No deduction | |

| Married Filing Jointly | $103,000 or less | $101,000 or less | 100% deduction |

| $103,001 to $123,000 | $101,001 to $120,999 | Partial deduction | |

| $123,000 or more | $121,000 or more | No deduction | |

| Married Filing Separately | Not eligible | Not eligible | 100% deduction |

| $9,999 or less | $9,999 or less | Partial deduction | |

| $10,000 or more | $10,000 or more | No deduction | |

| Those with spouses who earn no income | $193,000 or less | $189,000 or less | 100% deduction |

| $193,000 to $203,000 | $189,001 to $198,999 | Partial deduction | |

| $203,000 or more | $199,000 or more | No deduction |

How to calculate your reduced Roth IRA contribution

If the amount you can contribute must be reduced, figure your reduced contribution limit as follows.

- Start with your modified AGI.

- Subtract from your modified AGI:

- $193,000 if filing a joint return or qualifying widow(er).

- $-0- if married filing a separate return, and you lived with your spouse at any time during the year, or

- $122,000 for all other individuals.

- Divide the result by $15,000 ($10,000 if filing a joint return, qualifying widow(er), or married filing a separate return and you lived with your spouse at any time during the year).

- Multiply the result by the maximum contribution limit (before reduction by this adjustment and before reduction for any contributions to traditional IRAs).

- Subtract the result in (4) from the maximum contribution limit before this reduction. The result is your reduced contribution limit.

If your modified AGI is $200,000 and you are filing a joint return your reduced contribution limit would be: $200,000 – $193,000 = $7,000 / $15,000 = 0.4667

No tax-free withdrawals of earnings

Once you’ve withdrawn the amount that you’ve contributed to your account, you’ll avoid the 10% early-withdrawal penalty. But any earnings you withdraw will be subject to income tax and will count toward your income for the year.

Depending on your income and tax rate, you could be in for a large tax bill.

Conflict of interest

By using a Roth IRA with limited annual contributions, you’re sacrificing that option for retirement savings if you use it to save for college. If you’re eligible, the Roth IRA is one of the best ways to save for retirement, so it’s a good idea to make that your top priority with one.

Pros and cons of 529 plans

Pros of 529 plans

A 529 plan is specifically designed for college savings. Each state offers its own 529 plan, but you’re not restricted to using your state’s.

State tax savings

More than 30 states offer tax deductions or credits to taxpayers who contribute to a 529 plan account. These tax breaks vary by state and, in most cases, you have to contribute to your state’s plan to get the benefit.

High contribution limit

You can contribute up to $14,000 per year to a 529 plan without running into issues of the gift tax. And if you’re married, you can each contribute that amount for a total of $28,000. That’s more than five times higher the annual contribution limit of a Roth IRA.

Flexibility with beneficiaries and scholarships

As long as you withdraw money from your 529 plan for eligible education expenses, both your contributions and earnings in the account are tax-free.But if your child chooses not to go to college or gets scholarships, you’re not stuck with a tax problem.

Instead, you can change the beneficiary on the account to another child. And if your child got a scholarship, you can withdraw up to the amount of the scholarship without paying the penalty (although you’ll still pay taxes on your earnings).

Cons of 529 plans

Overall, 529 plans are a great option for saving for college. But there are some important things to keep in mind before getting one.

Penalties and taxes

If you don’t use your 529 plan funds for eligible college expenses, you’ll pay a 10% penalty and income taxes on any amount you withdraw for other purposes.

Limited investment options

Unlike a Roth IRA, a 529 plan is limited in its investment options. While some states offer more fund options than others, they still don’t offer as many as you might get with the retirement option.

What’s more, some 529 plans charge high fees on its funds, which can even wipe out any state tax benefits you might receive from your contributions.

Can hurt financial aid eligibility

A 529 plan is considered a parental asset for financial aid eligibility. The Department of Education can consider up to 5.64% of your 529 plan balance toward your expected family contribution, which can hurt your child’s chance of getting financial aid in the form of grants and subsidized federal loans.

Roth IRA vs. 529 plan: Which is better for you?

Neither option is a one-size-fits-all solution for everyone, so it’s important to know your goals and current financial situation before you choose one. Specifically, think about where you are with your retirement savings.

Remember, unlike college, there are no scholarships or unsecured loans for retirement

If you’re not on track for retirement, for instance, you might want to start with a Roth IRA to make sure that’s taken care of first.

“Remember, unlike college, there are no scholarships or unsecured loans for retirement”College Ave Student Loans.”And while college lasts for about four years, retirement could be 30 years or more.”

The same goes if you’re not sure you want to help your kids or not with their college savings. Find a good brokerage and open a Roth IRA account to get started.

Student loans are also available to help your child get through college.

However, if you are sure that you want to save specifically for college, opt for a 529 plan. The tax benefits and higher contribution limits will make it easier to achieve your goal of helping your child.

Check with your state to determine what kind of tax benefits you’ll get through its 529 plan.

In all of this, make sure you still prioritize your retirement over college savings. A good rule of thumb is to make sure you’re not paying more for your child’s college education per month than you are saving for your retirement,” says DePaulo.

BL

Ben Luthi is a personal finance writer and a credit cards expert who loves helping consumers and business owners make better financial decisions. His work has been featured in Time, MarketWatch, Yahoo! Finance, U.S. News & World Report, CNBC, Success Magazine, USA Today, The Huffington Post and many more.

Share this post: