Pay Off Your Debt or Save? What Should You Do First?

EC

Last updated 03/19/2024 by

Eliana CarmonaSummary:

Should you pay off debt or save? You should do both. Prioritize building a small emergency fund. Then switch to paying off your high-interest loans. If practical in your case, consolidate your debts into one loan with lower rates. Once you are only left with low-interest loans, start saving and investing. After building a nest egg, pay off your low-interest loans.

Choosing between saving for an emergency and paying off debt is not easy. If you are struggling with debt, you are definitely not alone. According to the latest data, household debt is at $14.56 trillion, and two out of every three credit card accounts carry a balance from month to month.

Between student loans, credit card debt, student loans, home loans, auto loans, and more, 80.9% of baby boomers and 81.5% of millennials are in debt. If you’re carrying debt, it may be tempting to prioritize paying it off above all else. But it’s also imperative to start saving for your future. So how do you know where to start? What should you do first: pay off debt or save for your future? Here is a roadmap that works for most people.

Roadmap to paying off debt and saving

- Build a modest emergency fund. Even just $500, $1,000, or one month of living expenses is a good start.

- Create a budget. Make sure every dollar is pulling its weight.

- Pay off all your debts using the blizzard method. Don’t include your mortgage and other low-interest loans at this stage.

- Pay off your smallest loan first and give yourself a quick win.

- Rank your debts by interest rate (larger to smaller) and pay them in that order.

- Consolidate your debt if you qualify for a low-interest consolidation loan.

- Increase your savings and build a more substantial emergency fund. Aim for three to six months of living expenses.

- Start investing. Aim to save 15% to 20% of your income and invest it in your retirement accounts.

- Pay off all your debts. Now it’s time to tackle your mortgage.

Let’s take a closer look at each step of the roadmap.

Build a small emergency fund

Before you focus on your credit card debt, student loans, or business loans, open a savings bank account and start an emergency fund. Emergency funds are cash reserves that are designed to cover unplanned expenses or financial emergencies. You can use them to pay for a car repair, medical bills, or deal with a job loss.

You need to put money aside into an emergency savings fund first because without one, any financial shock—even a small one—could set you back into a spiral of debt.

People who don’t have an emergency fund rely on credit cards or loans for even minor expenses, which can lead to debt that is harder to pay off.

Create a budget

A budget is a written plan that helps you decide how you will spend your money every month. It ensures you have enough money every month and that you are maximizing the use of your income. Without a budget, you could run out of money before your next paycheck and get further into debt. Make sure your budget allocates as much as possible aside from paying your debt.

Pay all your high-interest debts first

Once you have a small emergency fund and budget under your belt, it is time to make a dent in your debt. Start with high-interest loans, such as credit card accounts and personal loans. One rule of thumb is to pay off all debts with an interest rate above 7% APR.

Here is a good method to prioritize debt payments.

- The first step is to make sure you are making minimum payments on all your accounts. You want to avoid penalty fees at all costs.

- Then, pay off your smallest loan first. Paying off an account will give you a nice morale boost and the confidence to get serious with your debt.

- Organize them from the highest to the lowest interest rate and pay them off in that order. This will minimize your interest payments and help you get out of debt faster.

If you have good credit (or a cosigner with good credit), it can be a good idea to consolidate all your debt into one loan with a smaller interest rate.

These lenders provide competitive rates and terms.

Create a financial safety net

Once you have paid all your high-interest loans, paying off debt can wait. It is now time to save. The first step is to make sure you have a fully-funded emergency fund as a safety net. Aim to have enough savings to pay for three to six months of living expenses. This will protect you from falling back into debt if you lose your job or have to face an unexpected expense.

Start investing

Now you have a fully-funded safety net, focus on saving for retirement. A good goal is to save 15% to 20% of your income and invest it in your retirement accounts.

Take advantage of 401(k) employer match opportunities

If your employer offers 401(k) contribution matching, you should take full advantage of the situation. That’s because 401(k) contribution matching is a great way to maximize your retirement savings at little cost to yourself. Contribute at least as much as your employer match option will allow — typically 3%. If you’re self-employed, consider a solo-401(k) or SEP IRA. If there is anything left, invest it in a Roth IRA (or a traditional IRA).

Pay off your low-interest debts

Once you have a substantial sum of money invested for retirement, it is time to get back to paying off your low-interest debts. For most people, this means their mortgages. You can pay your mortgage years earlier and save thousands of dollars in interest by making extra payments every month. Even just switching to biweekly payments (instead of monthly payments) can make a big difference.

End Your Credit Card Debt Problems

Get a free consultation from a leading credit card debt expert.

It's quick, easy and won’t cost you anything.

Frequently asked questions about paying off debt and saving

Is paying off debt worth it?

Yes, it definitely is. The longer you carry your debt, the more interest you’ll pay. And if you’re carrying high-interest consumer debt, that interest can add up fast.

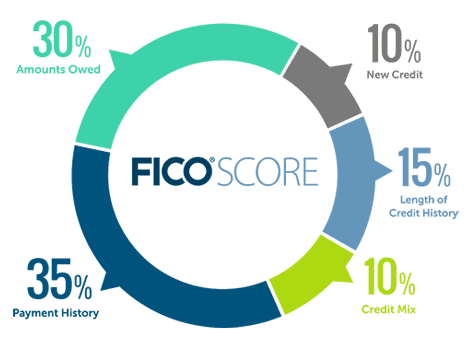

Paying off debt can also improve your credit score. Your credit utilization ratio, also known as your debt-to-credit ratio, has a massive impact on your credit score. That means that if you’re deeply in credit card debt, it’s hurting your credit score.

Having a low credit score can make it harder to get a loan, get an apartment, and even get a job. If you’re struggling with a low credit score, paying off your debts sooner might make your life much easier.

What are the best strategies for debt payments?

Several proven strategies can help you pay off the debt in a manageable and sustainable way.

A common problem area when it comes to personal debt involves credit cards. If you have several cards that are close to their limit, you may want to employ what is known as the avalanche method. This is where you pay the minimum on all your credit cards and as much as you can on the one with the highest interest rate. Continue this process each month until you have succeeded in your goal of paying off your entire credit card balance.

Another approach to effectively pay down debt is to acquire a 0% APR credit card. These cards usually have an introductory period of anywhere from 9 to 18 months, where the rate is zero. Afterward, it can balloon up to around 20%. If you can pay off a significant portion of your balance during this introductory period, this may be your best option to pay off debt.

If you have good credit, you may qualify for a low-interest debt consolidation loan. This can be an appealing option but can present a temptation to overspend if you are not careful about managing money. So you really have to question whether this is the best approach for you. Often the best guide in this situation is the advice from a credit counseling agency.

However, a debt settlement may be the best option if you have bad credit or your debt has snowballed out of control. These services are often the best source of information on debt repayment topics.

What are the benefits of saving before paying off debts?

Using all of your disposable income to get out of debt is a noble endeavor, but what happens when disaster strikes? If you have to pay off an emergency medical expense and don’t have any emergency savings, you might have to finance the procedure with a personal loan. And that brings you right back to where you began.

If you do not have an emergency savings account, you’re not alone. According to CNBC, more than 25% of Americans do not have savings set aside for retirement or emergencies in their budget. It is easy to see understand why creating an emergency savings account can be difficult. In the run of the month, most of us are just trying to take care of things like car loans, mortgages, student loans, paying off debt, investing in a retirement plan, servicing credit cards, building home equity, and everything else we have to do to keep our credit report favorable.

Interestingly, millennials appear to be the generation that is least likely to walk this fine balance between saving and debt repayment. A recent study by Wells Fargo found that even though 80% of millennials recognize the need to build savings, only 55% have actually acted on it. One possible reason for this is that Millennials begin their adult lives carrying more debt than any generation before them.

Savings and compound interest

Bear in mind that creating savings isn’t just about the present day. It’s crucial to start saving for your retirement as early as possible. That’s because saving money in a tax-deferred or tax-free retirement account lets you accrue a ton of interest over 50+ years. In other words, the sooner you can get some cash into a retirement account, the better.

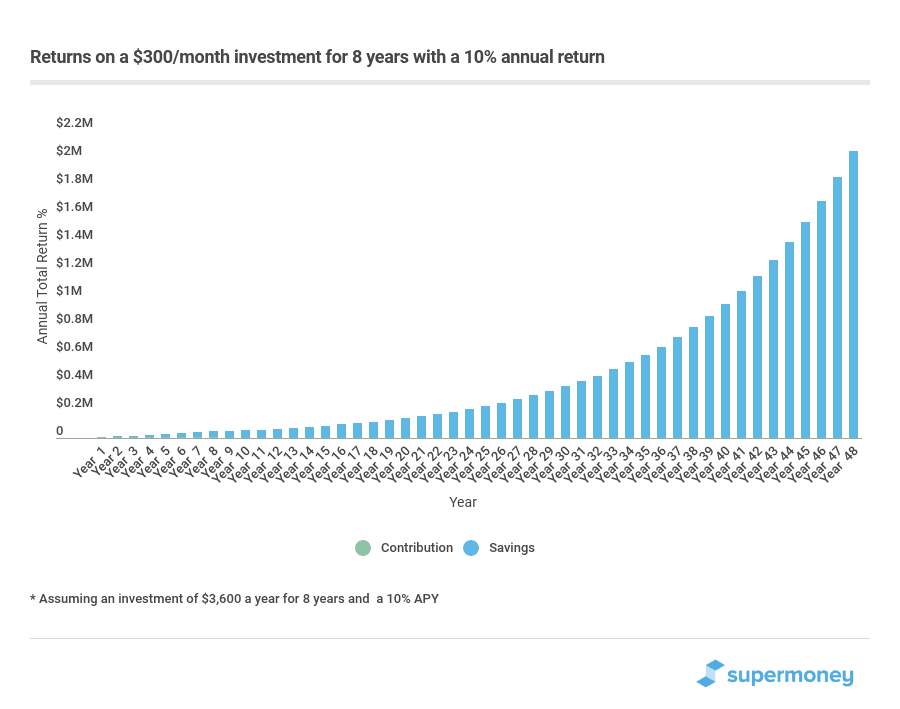

To illustrate, let’s say an 18-year-old invests $300 a month for just eight years (a total of $28,800). She could retire with more than $1 million in savings at age 58 even if she never invests another dime. If she waits till 65, the total would exceed $2 million.

That impressive return on investment assumes a 10% annual return. Investors typically use the S&P as a benchmark for the overall stock market, and the average return since its inception is around 12%.

What is the 7% rule?

If you need to decide whether some extra cash is better spent on retirement savings or early loan payments, consider the 7% rule.

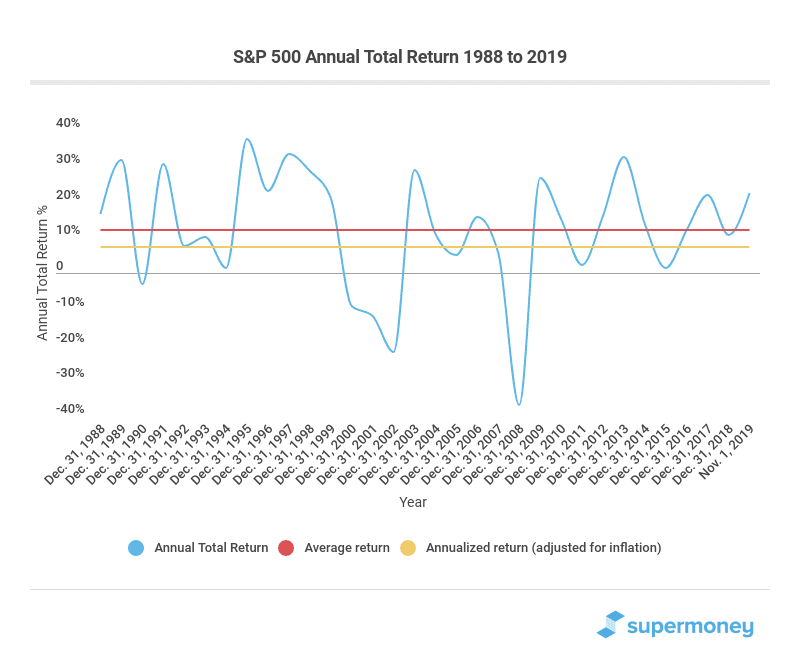

The average return on the S&P 500 is 7% if you adjust for inflation (around 12% if you don’t adjust for inflation). That means that if your interest rate on your loan is lower than 7%, you could, in theory, make more money on the stock market than you would save by paying off the loan early. Accordingly, if you’re paying more than 7% in interest, you should pay off debt first.

Note that this is just a rule of thumb. You can often lose money by investing your money instead of saving. However, it is a good principle to first pay off high-interest debt before you start saving.

How to decide if you should save or pay off debt

In general, it will benefit you to save and make early loan payments. If you have any high-interest consumer debt, you should pay this off as early as you can. But you should also allocate some of your savings to kickstart your retirement fund. It’s also a good idea to invest early and often in moderate-risk, long-term investment funds, such as an S&P 500 low-cost index fund. Like most other things in life, a balanced, well-planned approach is the best way to go.

Getting started

Not sure where to start? A good first step is to determine whether you qualify for a debt consolidation loan with good rates. Lowering the interest rate of all your loans can create huge savings. Once you have lowered your interest rates as much as possible, create a budget, open a savings account for your emergency fund. If you are ready to invest, these investment advisors offer low-cost options to get your investment portfolio started.

Share this post: