Industry Study

2024 Average Personal Loan Interest Rate Study

ML

Last updated 03/26/2024 by

Miron LulicEdited by

Our analysis of personal loan interest rates shows a wide price dispersion. This means consumers are paying more than they should for credit. The good news is financial technology tools can help reduce the search frictions behind this variation in prices across lenders.

You would think that personal loans would be a classic example of a commodity, like corn, steel, or gold. The interest rates are based on a market index. So, lenders could just work on perfecting their credit risk modeling to find as many eligible and creditworthy borrowers as possible.

After all, money is money. Borrowers have little incentive to pay one lender more than the other for the same cash.

In a free market, you might predict that frictionless competition will cause identical items, such as cash, to be sold at the same — or at least a very similar — price. You may also expect that the more lenders there are in a market, the less price dispersion you will find.

However, that is not what the consumer lending market looks like. If you have ever shopped for personal loan interest rates, you know that choosing the right lender matters—a lot.

There are several reasons why personal loans interest rates vary so much among lenders. These include differences in risk tolerance, cost of capital, underwriting models, and business goals — think of a lender offering low rates to gain market share versus a lender maximizing profitability.

In 2020, Americans held a balance of $323.5 billion in personal loans (source). Even a modest variation in interest rates could have a significant impact on the debt of American consumers. To illustrate, let’s assume that $323.5 billion balance has an average term of 36 months and a 13.5% APR. Dropping the average APR by only 3.5 percentage points to 10% would save Americans more than $19 billion in interest payments.

One of the services SuperMoney provides is a multi-lender marketplace that includes leading lenders, such as SoFi, LendingClub, Avant, Prosper, and many more. These lenders compete for customers by returning prequalified offers in response to loan inquiries made on SuperMoney. Borrowers can then compare the offers and choose the one that best fits their needs.

We knew the loan offer engine was providing borrowers with a wide range of APRs. But we wanted to have a better understanding of how much borrowers can save by comparing several lenders. So, we analyzed nearly 160,000 loan offers to over 15,000 borrowers who recently applied for a loan via SuperMoney’s loan offer engine. The results surprised us.

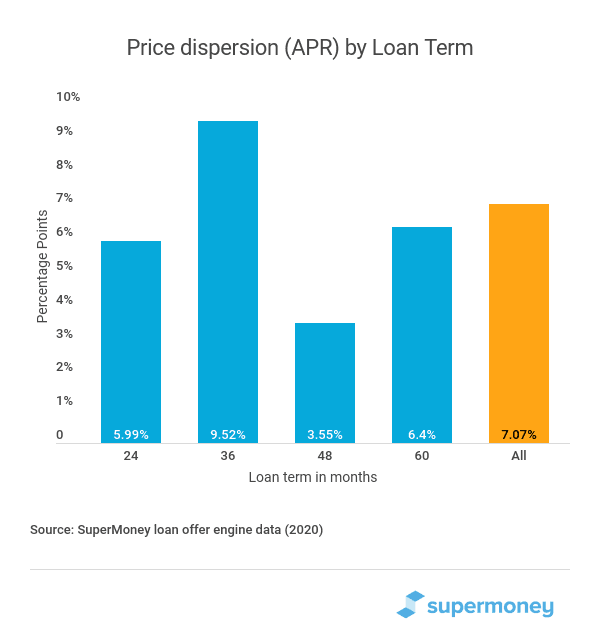

We found that the average difference between the highest and lowest APR offer (for the same borrower and loan term) was 7.1 percentage points.

Personal loans with a 36-month term had the broadest range of APR offers, 9.5 percentage points. While 48-month loans had the narrowest range, 3.6 percentage points.

Consider one borrower in our dataset with a credit score of 720 applied for a $30K loan with a 36-month term. The best offer had a 5.99% APR. Compare that to the offer with the highest APR, which was 15.87%. That is a 9.88 price dispersion, which is close to the average for a personal loan with this term.

This price dispersion on a $30K loan translates into savings of up to $5,050 — or 17% of the loan balance.

It is worth emphasizing again that this price dispersion is for loan offers to the same consumer.

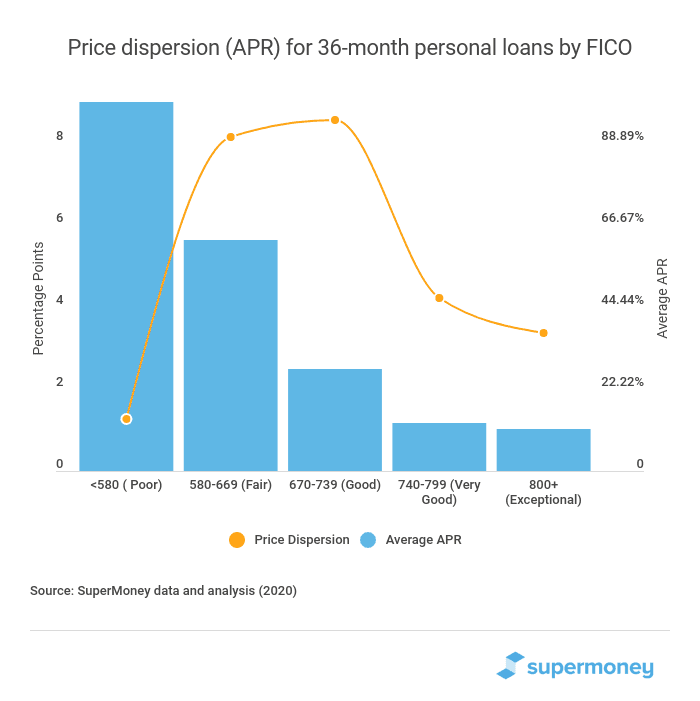

Comparing multiple lenders when shopping for a personal loan is a smart idea no matter what your credit score is. However, according to our analysis, borrowers with fair (580-669) and good credit (670-739) had the most to gain from comparing multiple lenders. Both credit score brackets had a price dispersion of 8 percentage points.

What is even more surprising is how important comparison shopping is for borrowers with excellent credit (800+). Not comparing multiple lenders could increase their APR by as much as dropping an entire credit score bracket.

In other words, the difference between the average APR available to borrowers with excellent credit (800+) and those in the lower credit score bracket (740-799) was smaller than the range of APRs lenders offered them. The data suggests that comparison shopping can — in some cases — save you more money than increasing your credit score by 100 points.

Unfortunately, many borrowers only check one or maybe two lenders. There are several reasons for this. Some borrowers may think all lenders have similar rates for people with their credit score. Others don’t have the time or know-how to compare several loan offers. Borrowers also worry that applying for multiple loans will hurt their credit score. They have a point. Every hard pull on your credit report can ding your credit score by a few points.

The good news is that many lenders allow you to prequalify and check your rates with a soft credit pull. SuperMoney’s loan offer engine helps you save time and money by showing you what prequalified offers you can get with leading online lenders. Invest a few minutes of your time, and you could know what rates and terms you qualify with your credit score. There are no strings attached, and it won’t hurt your credit score.

ML

Miron Lulic is founder and CEO at SuperMoney, a service that helps millions of people transparently compare financial services such as loans, investments, and more.

Share this post: