How To Settle IRS Tax Debt: All Available Options

JW

Last updated 03/19/2024 by

Jessica WalrackAre you struggling with tax debt and feel like you’ll never get out? You’re not alone. Every year, countless Americans face tax bills that they can’t afford to pay. Fortunately, the IRS has tax settlement programs that can help. Here’s what you need to know.

End Your IRS Tax Problems

Get a free consultation from a leading tax expert.

It's quick, easy and won’t cost you anything.

What is tax settlement and is it available to you?

Tax settlement occurs when you come to an agreement with the IRS which allows you to pay less than your total unpaid tax debt. The federal program for this called an offer in compromise (OIC).

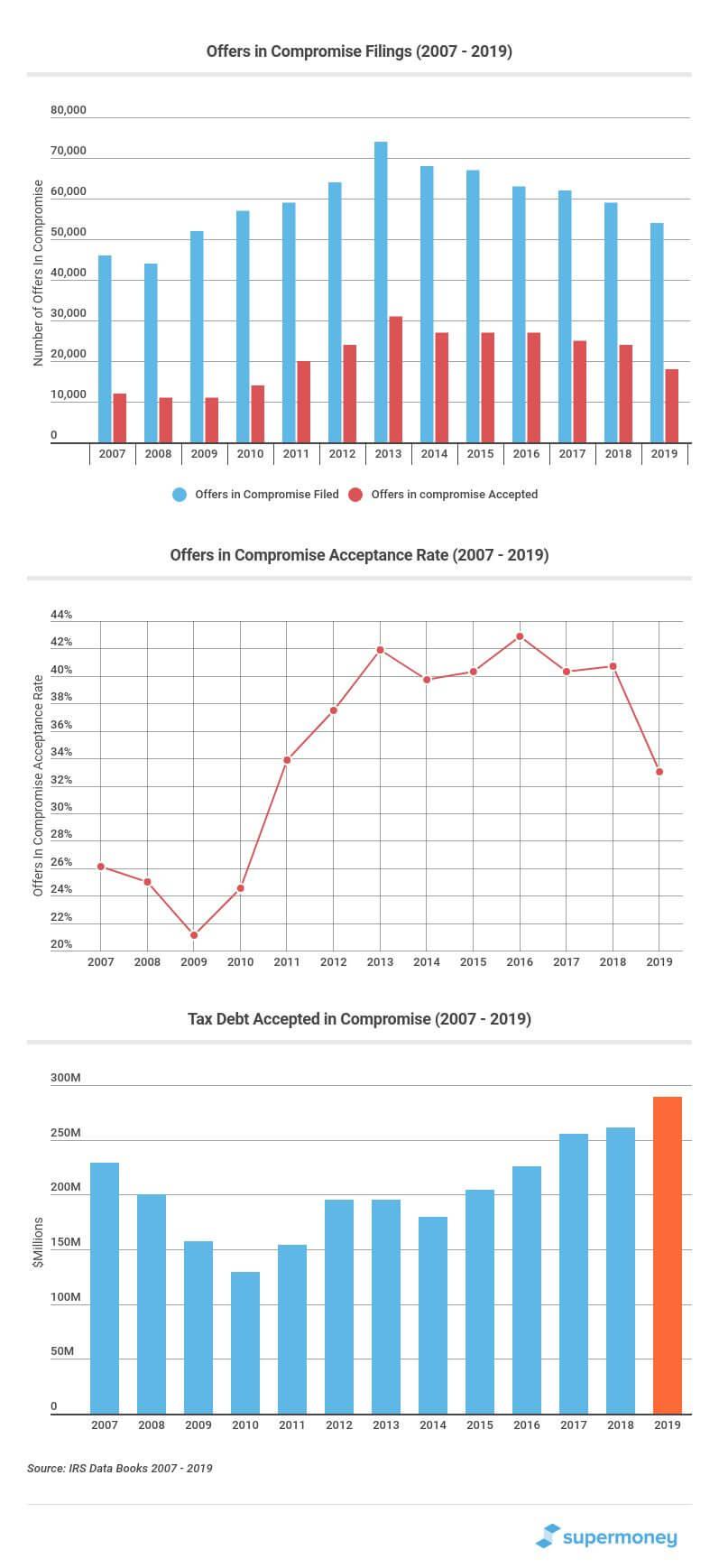

In 2019, the IRS accepted 18,000 offers-in-compromise — a total of $289.4 million — out of 18,000 requests. That is an acceptance rate of 33%.

Who can get an offer in compromise?

Offers in compromise are available for:

- Taxpayers who can’t afford to pay their full tax liability, as well as penalties and interest.

- Taxpayers who would undergo a financial hardship if they attempted to pay their full tax liability.

Of course, the IRS won’t simply take your word for it. When you apply for an offer in compromise, the IRS evaluates your ability to pay, with a focus on your income, expenses, and asset equity.

Additionally, you must meet a few other requirements. To qualify for an offer in compromise, the following must be true:

- You’re up to date on your tax return filings.

- You made all estimated tax payments for this tax year.

- You have a tax bill for at least one IRS debt on your offer.

- You’re not in a current bankruptcy proceeding.

However, an offer in compromise is the IRS’ last resort. The IRS will not turn to tax settlement offers until they’ve explored all other options (e.g. monthly installment plans, etc.).

How are offers in compromise paid?

When making an offer in compromise, you’ll usually need to pay a $186 application fee and submit an initial payment. The size of that payment depends on whether you choose to pay your taxes in a lump sum or a series of periodic payments to achieve tax resolution.

Lump-sum

The lump-sum cash option requires you send an initial payment, equal to 20% of the total amount of your offer, with your application. If accepted, you’ll pay the remaining debt in up to five payments.

Periodic payment plans

The periodic payment option requires an initial payment. Then, you’ll make monthly payments while the offer is considered. If the IRS approves your request, you’ll continue to pay until the full amount of the debt is paid.

Note that if your proposal is rejected, the money you sent will not usually be returned. However, the IRS will make an exception if you meet their Low-Income Certification guidelines. In this case, the application fee, initial payment, and payments during evaluation can be waived.

How much should you offer?

When you apply for an offer in compromise, you’ll propose the tax settlement — the amount that you’d like to pay in lieu of your full debt. But the IRS only accepts about 40% of OIC offers. How can you improve your chances of getting approved? How much should you offer to pay?

In order to decide how much you should pay, the IRS looks at your available assets and income. Then, they subtract the money required for your necessary living expenses. The resulting figure is what the IRS believes you’re able to pay. As long as your offer matches their calculation, you’ve got a great chance of getting approved.

In other words, as long as you use the IRS’ formula to calculate your offer, you’ll almost certainly succeed in your negotiation.

How does the IRS evaluate offers in compromise?

The IRS has its own measure of what living expenses are “necessary,” and it may not match yours. After deciding how much you should spend on basic living expenses, they will calculate your disposable cash flow, which will help them determine what a fair OIC offer will be.

Calculating living expenses

According to the IRS, the current National Standards for living expenses are as follows:

| Expense | One Person | Two Persons | Three Persons | Four Persons |

|---|---|---|---|---|

| Food | $386 | $685 | $786 | $958 |

| Housekeeping supplies | $40 | $72 | $76 | $76 |

| Apparel & services | $88 | $159 | $169 | $243 |

| Personal care products & services | $43 | $70 | $76 | $91 |

| Miscellaneous | $170 | $302 | $339 | $418 |

| Total | $727 | $1,288 | $1,446 | 1,786 |

To calculate costs for households with more than four people, the IRS adds $420 for every additional person.

Calculating cash flow

Then, to calculate your disposable cash flow, the IRS subtracts your living expenses from your income.

If you can pay off your settlement within five months, the IRS will multiply your cash flow by a factor of 12 to get the minimum amount due. If you need more time, they may give you 24 months to pay. However, they’ll also multiply your cash flow by 24 instead of 12, doubling the amount you owe.

Adding assets

Do you have assets? If so, the IRS will determine their settlement value and add about 80% of that to the value of your cash flow to get your tax settlement amount.

For example, say you make $2,000 per month and your necessary living expenses come out to $1,800. You would have $200 in disposable cash flow per month. Now say that you also have $5,000 in assets.

If you opt to pay your offer in compromise in a lump sum, you’ll need to pay the value of your cash flow ($200 x 12 = $2,400) plus the value of our assets ($5,000 x .80 = $4,000) for a total of $6,400 within five months.

With the periodic payment option, you would owe the cash flow value ($200 x 24 = $4,800) plus the asset value ($5,000 x .80 = $4,000) for a total of $8,800. Split into a 24 payment plan, you’re looking at about $370 per payment.

Putting it all together

Put simply, if you’re looking to calculate a viable offer in compromise, simply solve the following formula:

(Monthly Income – Living Expenses) x (12 or 24, depending on how long you’ll take to pay) + (Asset Value x 0.8) = Offer in Compromise

How to submit an offer in compromise

To apply for an offer in compromise, you must submit the following documents:

- Form 656, Offer in Compromise.

- $186 application fee paid to the United States Treasury unless you are considered Low-Income Certified.

- Initial offer payment.

- Form 433-A (OIC), completed and signed.

- Any required supporting documentation.

Be sure to make copies of everything and then mail off the package to the applicable IRS facility.

How do you negotiate a tax settlement with the IRS?

Negotiating a tax settlement with the IRS sounds challenging, but once you understand how the IRS evaluates OIC applications, you can seriously improve your chances. Simply use the IRS’ own formula to calculate your offer in compromise.

The IRS will deny an offer in compromise that doesn’t meet their standards. As long as your offer matches their own evaluation, you’ll succeed in your negotiation.

How else can you deal with tax debt?

If an offer in compromise doesn’t work for your situation, pursue the following alternatives:

- Installment agreement: Split the amount due up into payments over a timeframe of up to six years.

- Not currently collectible: A status for delinquent taxpayers which pauses active collections temporarily.

- File bankruptcy: Income taxes are eligible for discharge in a Chapter 7 Bankruptcy.

If you fall behind on taxes, you still have options. It’s in your best interest to stay in touch with the IRS, whether directly or through a representative. By doing so, you can prevent undesirable collection actions while finding the best tax debt settlement option for your situation.

Hire a tax relief expert

If you need to settle tax debt and get the best possible results, you may want to bring in a tax professional. The best tax relief firms specialize in representing taxpayers and helping them settle their taxes while protecting their best interests. Review and compare firms below to find the best one for you!

What Happens When You Don’t Pay Your Taxes?

Taxes are one of only two certainties in life, as the adage goes, and you can be sure the government is dogged in making sure people pay them. If you fail to pay your taxes, the IRS will eventually sniff you out and present you with a tax bill for the full amount you owe, plus interest and monthly late payment penalties. The longer your delay in making tax payments, the more the problem compounds and the worse the consequences.

Many credit card companies and other lenders hound you for overdue debts, and it is common knowledge that non-payment can affect your credit score. However, the IRS can go a step further and garnish your wages, revoke your passport, reclaim your property, and put a lien on your bank accounts. Simply put, resolving tax debt should be at the top of your priorities.

Don’t avoid filing a tax return, even if you cannot afford to pay your tax debt! The IRS will charge a failure-to-file penalty, absent a reasonable cause for late filing. This fee is equal to 5% of the unpaid balance for each month or part of the month the tax return is late, up to 25% of your unpaid taxes. These penalties and interest can be brutal.

Things to consider

If you’ve already found yourself with overdue tax returns and unpaid back taxes, you must act swiftly, but you should avoid negotiating alone. Don’t try to take on the IRS by yourself. While there are some options to settle your tax debt that don’t involve direct contact with the IRS, it’s usually best to seek professional help, especially if you’re in truly dire straits. The IRS is very good at getting convictions (96% convictions rate), 80% of which result in prison time.

Hire a reputable firm. Tax and debt relief solution companies are plentiful these days, but hiring someone without the right qualifications can compound your problems. When choosing a firm to work with, be sure that they have certified public accountants and certified tax attorneys on staff. Any firm you hire should be accredited by the National Association of Tax Professionals. Also, be sure it can act as a power of attorney in your state.

Options to Settle Your Tax Debt

The only two IRS tax repayment methods that allow you to pay less than you actually owe in federal tax are offers in compromise agreements and Partial Payment Installment Agreements. These strategies can save you a lot of money, but they aren’t easy to achieve. Television ads suggesting you can easily settle tax debt for pennies on the dollar do not paint a complete picture.

Offers in Compromise

The Offer in Compromise program does allow taxpayers without the ability to pay their full tax bill to settle for less–paid in either a lump sum or monthly installments–, but it is considered a last resort by the IRS.

It is worth noting that to qualify for this program; a taxpayer must have so few assets that the IRS would rather settle than spend time seizing what little the taxpayer owns. They will generally accept an offer amount only if they are convinced it’s the most money they can expect to collect from a taxpayer within a “reasonable amount of time,” according to their verbiage– usually, the full 10 years before the statute of limitations runs out.

How an Offer in Compromise Works

An Offer in Compromise (OIC) is a settlement agreement between you and the IRS that allows you to pay an amount that is less than what you owe in taxes. An Offer in Compromise may be accepted or rejected by the IRS. Even if it is accepted, it may not be for the amount you hoped. You must meet very specific criteria to qualify for an Offer in Compromise.

When pursuing an OIC, a taxpayer or taxpayers will complete an offer package, which includes several pages of forms, a non-refundable $205 application fee, and a non-refundable initial payment, in addition to a reasonable offer of what they hope to or, are able to pay, and which the IRS would consider acceptable. Step-by-step instructions, along with all necessary forms, may be found in the Offer in Compromise Booklet, Form 656-B. All Offer applications must be received on Form 656 with a revision date of April 27, 2020, along with the non-refundable application fee of $205, as stated, increased from $186. However, the application fee may be waived if you qualify for Low-Income Certification or submit a Doubt as to Liability offer.

Who is Eligible for an OIC?

To apply for an Offer in Compromise, all tax returns due or past due must first be filed. Additionally, all estimated tax payments for the current year must be paid. There are further criteria that must be met by business owners with employees.

The IRS looks at several factors to determine your OIC eligibility, namely, your income, assets, the equity you may have in investments, and expenses. A Collection Information Statement, Form 433-F for wage-earners or those who are self-employed, is required to help the IRS evaluate your ability to pay.

Your net worth, all available sources of credit–including home equity lines of credit, retirement plans, and cash will all be evaluated as part of your OIC application. Your Collection Information Statement must demonstrate that you cannot pay your tax debt in full or that doing so would cause severe financial hardship. Once a taxpayer’s inability to pay back taxes is established, the IRS applies a formula based on your leftover monthly income after allowed expenses, plus available income from your assets, to assess and accept or reject your offer.

The IRS provides an Offer in Compromise Pre-Qualifier questionnaire you may use to confirm your eligibility and prepare a preliminary proposal. Note that you are ineligible to apply for an Offer in Compromise if you have an open bankruptcy filing.

If you cannot afford to pay the application fee for an Offer in Compromise, the IRS may grant you an exemption if you meet the criteria for a Low-Income Certification. Guidelines and instructions for obtaining Low-Income Certification status are included in the revised Form 656. If you meet those requirements, you will not be required to pay monthly installments for the period your application is under consideration.

Offer in Compromise Payment Plan Options

The initial payment for your Offer in Compromise, which is due with your application, will depend on which payment option you choose. Here, you have two possibilities from which to select:

- Lump-Sum Cash – You may choose to make a lump-sum payment, in which you submit a 20% down payment on the total offer amount along with the application. If you receive written confirmation that your offer has been accepted, the rest of the amount will then have to be paid in five or fewer installments.

- Monthly Installment Payments – Alternatively, you may opt to make monthly payments, spread out over a period of up to 24 months, with the initial payment submitted with your application. You must continue to pay the monthly installments until you notice that the IRS has decided on whether or not to accept your offer.

How much will the IRS settle for?

The average offer in compromise the IRS accepted in 2020 was $16,176. In 2020, the IRS approved 17890 offers in compromise with a total value of $289.4 million. (Source) Divide $289.4 million by 17,890 and, presto, you get an average offer in compromise of $16,176.

Of course, that number is meaningless. The real question is “how much will the IRS settle for in my case?” Not some hypothetical average. Read this article for a deep dive into how the IRS determines eligibility for the Offer in Compromise program and how it calculates the minimum offer it can accept.

Installment Agreement Plans – Partial Payment Installment Agreement

A Partial Payment Installment Agreement (PPIA) is very similar to an Offer in Compromise in many ways, primarily because it allows taxpayers to make a series of payments to eliminate tax debt for an amount that is less than what they actually owe. This is the only other option offered by the IRS that might enable a taxpayer to settle a tax debt for pennies on the dollar– though it is not easily obtained, and the process is hardly a walk in the park. The program’s repayment terms are usually longer and can continue up to the tax debt expiration of 10 years. Any balance that remains at the close of the term of the installment agreement is forgiven.

The overall debt reduction in a Partial Payment Installment Agreement isn’t as generous as the Offer in Compromise, but it is easier to qualify for than an OIC. Eligibility requirements for a PPIA are similar to an OIC, although having equity in assets may give the IRS reason not to grant you one, as they may require you to borrow against said assets to pay off your tax debt. Another drawback to a PPIA is that it gives the IRS the ability to reevaluate your financial situation every two years to determine if your circumstances have changed such that you can afford to pay more. If so, they can demand an increased monthly payment and the sale, or borrowing against equity, of assets.

To be granted a PPIA, your tax liability cannot be less than $10,000 in tax, penalties, and interest; you must not have filed for bankruptcy, and you must not have had an Offer in Compromise accepted. In addition to being easier to qualify for and usually having lower monthly payments, one benefit of pursuing a PPIA is that the IRS tends to make decisions on PPIA applications much faster than on OIC applications.

Other Installment Agreements

If you do not qualify for a reduced tax settlement through either an Offer in Compromise or Partial Payment Installment Agreement, but present financial difficulties prevent you from paying the full amount you owe, you still have the option of enrolling in a Long-term or Short-term Installment Plan. In either case, you determine the monthly installment amount, so long as it’s approved by the IRS and you’re able to pay off the debt within the allotted timeframe.

- A Long-term Installment Plan allows you to pay your taxes within six years. There is a fee to enter this plan, which is based on how you make your payments (check, money order, direct debit, or another online method).

- A Short-term Installment Plan requires you to pay your tax debt within 120 days. There are no fees associated with this plan. However, if you cannot pay all overdue taxes within 120 days, you will have to apply for the long-term plan and pay the requisite fees.

In either installment option, penalties and interest continue to accrue on the unpaid balance. You will be billed for this and responsible for paying the remainder with your final installment.

To be approved for an installment plan, you must not have an outstanding tax return, and you must be up-to-date on your state income tax and late fees. If your tax debt is greater than $50,000, you will not qualify for an installment plan.

Whichever route you choose to pursue, it is strongly advised that you consult a certified tax professional to review all your options and assist in negotiating with the IRS.

Penalty Abatement

One of the biggest problems with tax debt is the interest and penalty fees that add up. If you have a clean history of paying your taxes on time and arrange with the IRS a plan to pay off your debt, you may qualify to have your penalties abated.

Credit Card Debt Consolidation

One way to forgo hiring a tax attorney and set up your own payment plan is to pay off your tax debt with a credit card. Look for a card that has a 0% introductory APR, such as the Citi Simplicity Card. Make sure that you qualify for a large enough limit to cover your tax debt. It’s also imperative to make sure you can pay off the balance before the intro APR period expires. Paying upwards of 20% in interest if you don’t pay off your balance can put you right back into debt trouble. Check out our options for 0% intro APR cards here.

File for Bankruptcy

In extreme circumstances, your best option out of debt may be to file for bankruptcy. Chapter 7 bankruptcy fully discharges allowable debts. Chapter 13 may mean a tax repayment plan after a reduction in your debt owed. Find out if bankruptcy is the right option for you.

Statute of Limitations

The IRS has a statute of limitations of 10 years to collect all payments and penalties from taxpayers. In some cases, a tax attorney or CPA may be able to help you navigate the 10-year period for your debt. This can be tricky and requires a lot of paperwork, so don’t rely on this method to get out from under debt without the right team.

Ponzi Scheme Forgiveness

If you can prove you were the victim of a fraudulent investment operation, known as a Ponzi scheme, that wiped out your savings, you can have your debt reduced by 30% to 40% and set up a payment plan to resolve your tax debt.

Innocent Spouse Relief

If you inherited tax debt from a spouse, your situation might qualify for innocent spouse relief. You must prove your spouse incorrectly reported his or her income or deductions, and you had no knowledge of this to qualify for this program.

Conclusion

Tax debt can seem like a deep hole that you may never escape from but remember you have options to make it easier. As soon as you realize you have tax debt to be settled, you need to act. The longer you wait, the more penalties and interest accrue. The IRS will also become more likely to act, seizing property and wages to collect the debt.

Reducing and eliminating your tax debt is a complicated process with a bevy of options. Instead of sifting through them by yourself, talk to a tax professional to sort out what will work best for you. We have built a tax relief tool to help you understand what options are available to you. You will get a no-obligation, free consultation with a qualified expert to help you explore tax debt consolidation and repayment strategies.

In addition, if you owe a lot of money to the IRS, it can help to have a tax relief company on your side. The best tax relief companies have tax lawyers and enrolled agents on staff, provide a money-back guarantee and charge competitive rates. Check out which tax relief company is the best fit for you.

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: