How Is Your Credit Score Calculated?

GY

Last updated 03/21/2024 by

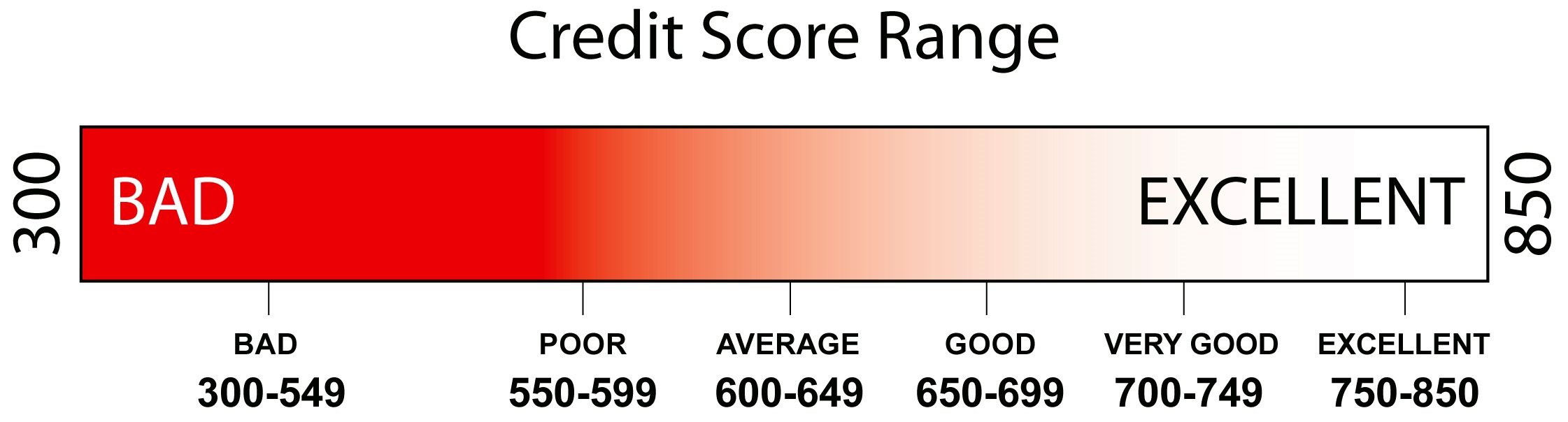

Gina YoungA credit score is a number ranging from 300-850, which creditors use to evaluate how well you will potentially be able to repay your bills.

There are three credit bureaus: Transunion, Experian, and Equifax. These agencies receive information about you from creditors and compile that information into a credit risk score. Some creditors send information to only one credit bureau, some to all three. Each credit bureau only uses the information that is supplied to it in order to calculate your score, so it is entirely possible to have different scores from each bureau. Your credit score reflects everything that is reported to the credit bureaus about you — good or not-so-good.

There are three credit bureaus: Transunion, Experian, and Equifax. These agencies receive information about you from creditors and compile that information into a credit risk score. Some creditors send information to only one credit bureau, some to all three. Each credit bureau only uses the information that is supplied to it in order to calculate your score, so it is entirely possible to have different scores from each bureau. Your credit score reflects everything that is reported to the credit bureaus about you — good or not-so-good. Your credit score is decided by several factors, including:

Your credit score is decided by several factors, including:- The Number of Accounts — the number of creditors that send information to the credit bureau regarding your account. If you only have one or two creditors reporting about you, it will take longer to build a good score.

- The Types of Accounts — do you have major creditors, such as a mortgage loan or auto loan, or just creditors of revolving debt (credit cards)? Obviously, an on-time payment history is important for any type of account, but some accounts, such as mortgage loans carry a bit more weight when it comes to your credit score, and even approval for loans from future lenders.

- Debt Level as Compared to Available Credit — when calculating your credit score, they also take into account where you have available credit on the accounts that you have open. Alternatively, they will also be looking to see if you have maxed out all of your available credit. You should aim to try to keep each account level at or below the 50% level of debt to available credit.

- Length of Credit History — how long have creditors been reporting to the credit bureaus on you? If you don’t have a very lengthy credit history, this can be a negative when calculating your score because there is just not enough information available to calculate your score. However, time is on your side—the longer creditors report on your account payment, the more information there is to base your score on. Just make sure you are making on-time payments and that will build a solid, higher score.

- Payment History — do you make your payments on-time each month? Keep in mind, an on-time payment per the credit report is anything less than 30 days late. So that means that even if you forget to pay your credit card bill that is due on the 1st of the month until the 10th of that month, it will not hurt your credit—it will, however cost you late fees, so try to avoid being late.

- Credit Inquiries — how many creditors have pulled your credit recently? Too many inquiries within a short period of time can actually lower your credit score. Make sure that when you apply for a new credit card, auto loan, or mortgage that you shop around for the right lender BEFORE you start letting potential financiers pull your credit. Get an idea of which lender you want to go with and then allow your credit report to be pulled.

It is important to regularly review your credit report to make sure that the information reporting on you is accurate and up-to-date. If old accounts are showing up or negative items have not been cleared, they may be damaging your score. It is also critical to review your credit to make sure that no fraudulent activity is taking place.

GY

Gina Young is an accomplished finance writer who has written for publications including Examiner.com, Lexington Law, Talk Markets, CreditRepair.com as well as her own blog (Money Savvy Living), giving budgeting and frugal living advice. With a bachelor’s degree in Accounting and Finance from Ashland University and a MBA from Indiana Wesleyan University, Young has impressive credentials in many aspects of investing, retirement planning, and personal finance.

Share this post: