How Soon Can You Refinance a Student Loan After Graduating? 3 Reasons to Wait

Last updated 03/19/2024 by

Ben Luthi

If you’re about to leave college or you just graduated, you might already be thinking about what you’re going to do with your student loans. Refinancing is one option to help you pay them down more quickly. But how soon can you refinance a student loan after graduation? There’s no waiting period, so you can technically refinance them the minute you’re officially done.

But is it smart to refinance your student loans right after you graduate? The fact is that you might not qualify. Here’s what you need to know.

Get Competing Student Loan Refinancing Offers

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What does it mean when you refinance a student loan?

Refinancing is the process of paying off one or more loans with a new loan. With student loan refinancing, you effectively transfer your original student loan debt to a new lender.

Depending on your interest rate and repayment period on your original loans, you may save money by refinancing them, especially if you can get a lower interest rate. But refinancing does come with some drawbacks.

You should check to see if you qualify for Public Service Loan Forgiveness, or income-based repayment before looking into refinancing

For starters, you’ll lose certain benefits if you refinance federal student loans, such as access to income-driven repayment plans and student loan forgiveness programs.

You should check to see if you qualify for Public Service Loan Forgiveness, or income-based repayment before looking into refinancing. If you’re eligible for these programs, they may help you save money on your loans.

Also, you may need to get a cosigner to qualify for the lowest rates student loan refinancing companies offer.

If refinancing makes sense, though, it’s important to make sure you can qualify before you apply.

Why you might want to wait to refinance your student loans

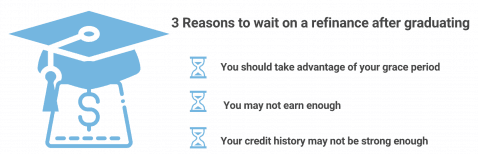

While it’s possible to refinance your student loans right after graduating, it may not be the best time to do it for three reasons:

1. You should take advantage of your grace period

Both federal and private student loans typically provide you with a six-month grace period after you graduate before you need to start making payments. This period gives you enough time to get your finances together. Typically you will want to find a job and then figure out a good repayment plan.

If you have a high federal student loan balance, it also gives you time to decide whether you should get on an income-driven repayment plan or try for the Public Service Loan Forgiveness program. In other words, don’t rush into a decision you may regret later.

2. You may not earn enough

When any lender is deciding whether or not to approve a credit application, one of the factors it considers is your debt-to-income ratio (DTI). This ratio is calculated by dividing your monthly debt payments by your monthly gross income.

If you’ve just started at a low-paying, entry-level job and you have tens of thousands of dollars in student loan debt, your DTI might be too high to qualify to refinance your student loans. So you may need to wait until you get a raise before you apply.

3. Your credit history may not be strong enough

Federal student loans typically don’t require a credit check but refinancing those loans does. Some student loan refinancing companies have minimum credit score requirements, and others just look at your overall credit and financial profiles.

You’ll have a hard time getting approved if the only credit you used in college was your student loans. As such, it’s important to start building your credit history right away.

Once you start making payments on your student loans, that will help you establish your credit history. But it’s also a good idea to get a secured credit card to diversify your credit mix and show more positive payment history.

Over time, your credit will improve, and you’ll have a better chance of refinancing.

Whether you aim to lower your monthly payments, lower your overall payments, or both, you should make sure that you choose a lender that enables you to meet at least one of these objectives

How soon should you refinance a student loan after graduating?

If refinancing can save you time and money, the sooner you do it, the better. Start comparing student loan refinancing companies and consider asking a trusted family member to cosign your application.

Whether you aim to lower your monthly payments, lower your overall payments, or both, you should make sure that you choose a lender that enables you to meet at least one of these objectives. If you can’t manage to get a lower interest rate right now, work on increasing your income and improving your credit score and try again later.

Whether you qualify for refinancing or not, make sure you have a good student loan repayment plan in place. The more intentional you are about paying off your student loans, the easier it will be to achieve your goal.

Ben Luthi is a personal finance writer and a credit cards expert who loves helping consumers and business owners make better financial decisions. His work has been featured in Time, MarketWatch, Yahoo! Finance, U.S. News & World Report, CNBC, Success Magazine, USA Today, The Huffington Post and many more.

Share this post:

Table of Contents