How Does a Mortgage Affect Your Credit Score?

Last updated 12/10/2025 by

Camilla Smoot

Summary:

Overall, a mortgage will have a positive impact on your credit score. Although it may lower in the beginning, your credit score will rise again and help you accumulate wealth as long as you make your monthly payments on time. Missing a payment can negatively impact your credit score, and repeatedly missing payments could lead to foreclosure. This can greatly damage your credit report and could be hard to recover from.

Taking out a mortgage can be intimidating, and you might have a lot of questions. Will it harm my credit score? Is it worth the pricey down payment and monthly payments? What type of mortgage loan should I get? Though a mortgage sounds complicated, it’s ultimately worth the money as long as you make your payments on time. If you are a responsible borrower and make timely payments, you will stay in good standing with mortgage lenders, credit card companies, and others in the mortgage industry.

Keep reading to learn more about what you need to earn a mortgage loan, what loan options there are, and what impact a mortgage can have on your credit.

Compare Home Loans

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

How can I get a mortgage loan?

A mortgage lender can lay out the requirements more in-depth, but here are a few quick facts on earning a home loan.

To earn a loan, you must have a good debt to income ratio, credit score, and credit report. On average, the minimum credit score required for a home loan is around 500 – 600. Bad credit or a low credit score can make it difficult to obtain a loan, but it’s not impossible.

When looking at mortgage loans, there are different options you can choose from.

Conventional loans

A conventional loan is great for those with good credit scores. As opposed to other loans, government agencies do not insure conventional loans, so they generally require higher credit scores. Most mortgage lenders require a minimum credit score of at least 620 to earn a conventional loan.

FHA loans

An FHA loan is insured by the Federal Housing Administration, which makes it a great option for those with lower credit scores. You’ll need a minimum credit score of 580 to qualify for this loan, and you don’t need a minimum FICO score.

VA loans

VA loans are insured by the U.S. Department of Veterans Affairs. Since this loan doesn’t require a down payment, VA loans are another great option for those with low credit scores.

To qualify for a VA loan, you must be a member or veteran of the U.S. Military, Military Reserves, or National Guard, or be a spouse of a military member who passed while on duty. You can finance the full purchase price without paying for private mortgage insurance with a VA loan.

How does a mortgage affect my credit score?

Getting a mortgage doesn’t doom your credit score forever. In fact, with timely payments, your credit score will improve with a mortgage.

A new mortgage may lower your credit score at first

When you first get a mortgage, your credit score will lower. This decrease often occurs when you first apply for a loan because the lender conducts a hard credit inquiry, which can temporarily lower your score.

What is a hard inquiry?

A hard inquiry refers to the credit check a lender performs to determine your risk as a borrower. Because this is a review of your previous performance, a hard inquiry can show up on your credit report and negatively impact your credit score.

Over time, however, your credit score will rise again as you make timely payments on your mortgage. Be sure to pay them on time, as missed payments can lead to a lower credit score.

A mortgage diversifies your credit

Not only does a prompt mortgage payment help your credit score, but it also diversifies your credit. Different types of credit include auto loans, credit cards, and mortgages. More diversity in your credit demonstrates your ability to handle multiple loans and payments at the same time. This shows the lender you are responsible and low risk for future loans, such as a mortgage loan.

How can a mortgage benefit my credit score?

Even though a mortgage loan will lower your credit score at first, this shouldn’t last too long. Because a mortgage lasts for years, making repeated punctual payments results in long-lasting benefits to your credit history.

How can a mortgage hurt my credit?

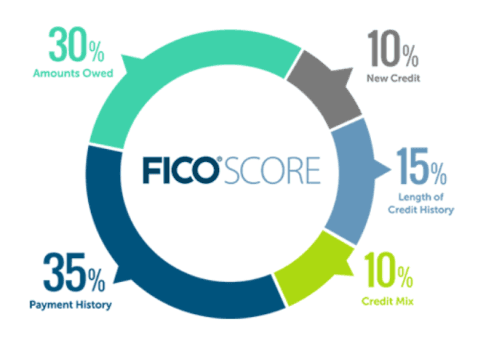

Credit scores suffer greatly if you fail to make monthly payments on time. Monthly payments account for 35% of your credit report. Late payments will stay on your credit history for seven years, so it is important to make sure these payments are made on time. Multiple late payments can lead to a foreclosure and cause serious damage to your credit.

What can I do to raise my credit score quickly after taking out a mortgage?

A credit scoring model takes several factors into account. Your payment history is the most influential factor in a credit scoring model, followed by amounts owed, credit history, new credit, and credit mix. Below are a few ideas on utilizing these factors and improving your credit report.

- Make regular timely mortgage payments. This is the most important step for you to remember. Payment history greatly influences credit scores, so making on-time payments will help you achieve a good credit score.

- Keep old credit accounts open, even if they’re not used. Credit history accounts for 15% of your credit score. Having a long-term account can help build your credit report.

- Have a good credit mix or diversity in your credit report. This accounts for 10% of your credit score. A diverse credit report shows mortgage lenders that you can manage different loans and maintain a reasonable budget. Auto loans, student loans, mortgage loans, and opening a credit card account are some ways you can add diversity to your credit.

Rent vs. Mortgage Payment

While both rent and a mortgage require you to make a monthly payment, mortgage payments influence your credit score while rent usually doesn’t. Though credit calculations automatically factor mortgage payments into credit scores, most scoring models do not take rent payments into account. So, if you’re hoping to build your credit by paying rent, you might have more success doing so with a mortgage.

Continue Learning

- Conventional Mortgage — Learn how conventional loans work, who qualifies, and when they’re a strong fit for homebuyers.

- First-Time Home Buyer Guide — A step-by-step overview of the buying process, from budgeting to closing.

- FHA Loans — Explore low–down payment options and more flexible credit requirements for first-time and repeat buyers.

- VA Loans — See how eligible veterans and service members can buy with 0% down and competitive rates.

- USDA Loans — Understand rural and suburban 0% down loan options and income eligibility rules.

- Bridge Loans — Find out how bridge financing can help you buy a new home before selling your current one.

- Jumbo Loans — Learn what makes a loan “jumbo,” how limits work, and what lenders look for.

- Piggyback Mortgages — Discover how 80-10-10 structures can help you avoid PMI or finance a higher-priced home.

- Assumable Mortgages — See when you can take over a seller’s existing loan and why it can be a big advantage.

- Down Payment Assistance — Explore grant and program options that can reduce your upfront costs.

FAQs

Does a mortgage negatively affect your credit score?

In the long run, no. When you first take out a mortgage, your credit score may lose a few points. Over the years, however, your credit score will experience a significant boost with timely mortgage payments.

Can I buy a car after buying a house?

Provided you have a good credit score and money to pay for it, receiving an auto loan soon after a mortgage loan should not be difficult. However, remember that many lenders use a hard inquiry to check your credit, which briefly decreases your credit score.

Can I use my credit card while buying a house?

As long as you have enough available credit, you can buy your house with a credit card, but we don’t recommend it. If you can pay with a credit card, you likely qualify for a loan, which will accumulate less interest than a credit card.

Key Takeaways

- Your credit score may drop when you initially take out a home loan.

- Overall, a mortgage loan will greatly benefit your credit score.

- A mortgage adds diversity to your credit report and helps raise your credit score.

- Be sure to make your monthly mortgage payment on time. Late payments negatively impact your credit score.

Find Your Perfect Offer

One of the first steps to obtaining a mortgage is finding the right mortgage lender. Compare and review mortgage lenders here, especially if you’re a first-time homebuyer.

Camilla has a background in journalism and business communications. She specializes in writing complex information in understandable ways. She has written on a variety of topics including money, science, personal finance, politics, and more. Her work has been published in the HuffPost, KSL.com, Deseret News, and more.

Share this post:

AddTable of Contents