How Student Credit Cards Work

Last updated 03/19/2024 by

Allison Martin

Have you considered applying for a student credit card? If you can keep your spending under control, it may not be such a bad idea. However, a lot of students might not know how student credit cards work and end up putting themselves in a poor financial position. Student credit cards are a safe and convenient way to make purchases while earning rewards. And in some instances, you can take advantage of interest-free financing.

You can also start building credit, so you’ll be able to qualify for the best rates on loan products, insurance premiums or get approved for your next apartment.

SuperMoney guide on how student credit cards work breaks down all the different types of cards and options to help you make smart decisions before applying for one.

Compare Student Credit Cards

Compare rates of multiple card issuers. Discover your lowest eligible rate.

Types of college student credit cards

There are two types of student credit cards to choose from: secured and unsecured. Both cards function in the same manner, but a secured card is backed by collateral or a minimum cash deposit. Some key differences on how student credit cards work:

Secured vs. unsecured credit cards

| Secured Credit Cards | Unsecured Credit Cards |

|

|

How student credit cards work

Let’s take a closer look at what you’ll need to qualify for a student credit card, how interest works along with a few tips to use your card responsibly.

What credit score do I need to qualify?

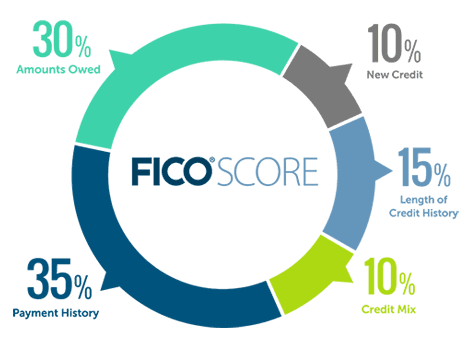

Approximately 90% of creditors consider your FICO score when determining the credit limit (if any) that you qualify for. (Source)

Below is a diagram of what’s in your FICO score:

How much money do I need to make?

Creditors will also factor your income into the equation. But why? Well, the Credit Card Act of 2009 requires mandates that students, ages 18-21, provide proof of income or get a cosigner to be considered for a credit card. If you fail to meet one of the two criteria, the application will be denied, and a secured card may be your only option.

Using a Cosigner

By signing on the dotted line, the co-signer agrees to assume equal liability for any transactions that take place on our student credit card. This means that they will be held liable for any charges incurred in the event you default.

To increase your chances of getting approved with a co-signer, inquire about their credit history. If they have bad credit, you may still have a hard time qualifying for a student credit card.

Qualifying without a cosigner

If you meet the income criteria under the CARD Act of 2009, you may not have to worry about a cosigner.

But what if you don’t, but can’t find anyone to sign on your behalf? It’s not uncommon as your parents, relatives or friends may not be willing to assume the risk. The good news is you have a few options:

- Get a part-time job so you can provide proof of income to the creditor. If you still can’t get approved, try a secured card. They’re much easier to qualify for, but you’ll need the minimum deposit to access the credit line.

- Ask your parents to be an authorized user on their card so you can start building a credit history. Apply again once your score has increased a bit, and you can provide proof of income.

Interest Rates

The lower the credit score, the higher the APR. However, credit card issuers disclose a range in their terms, so you’ll have an idea of what you’re getting into when applying. You should also be mindful of penalty APRs, which are higher and may apply when you’re late on a credit card payment.

Using your student credit card responsibly

Some tips to keep in mind when considering college student credit cards:

- Don’t go for the first credit card offer that catches your eye. Instead, shop around to explore your best options. Use SuperMoney’s student credit card review and comparison tool to help you with your search.

- Understand the qualification criteria before you apply. If you don’t have a steady source of income or a co-signer, don’t waste your time applying for an unsecured credit card.

- Read the fine print to make sure the card is a good fit. Pay attention to the fees, sign up bonuses, rewards programs, and APRs.

- It’s never a good idea to use the card excessively when out with college friends just for the sake of earning points unless you can afford to pay back what you spend right away.

- Avoid cash advances as they come with a hefty fee and higher APR.

- Always make timely payments, or your credit score could take a hit.

- Pay more than the minimum each month since it only covers a small portion of the principal, and the remainder of the funds are allocated to interest and fees (if applicable). To illustrate, if you have a credit card with a 19.99% APR, $500 balance and $25 minimum payment, it will take you 39 months to pay off. That means you’ll pay $167.87 in interest, alone.

Most importantly, only spend what you can comfortably afford to pay back each month before interest kicks in. Otherwise, you could get stuck in the minimum payment trap that keeps you in debt for years to come.

How to find the best college student credit cards?

If you’re ready to begin your search, visit our student credit cards page to start your search. You can compare your options, read user reviews, and use the filters to narrow down credit cards that will best suit your needs.

Allison Martin is an accomplished finance writer who has written for publications including The Wall Street Journal, MoneyTalksNews, The Simple Dollar, and Credit.com. Her work has been featured on Fox Business, Yahoo! Finance, MSN Money, and ABC News. She enjoys writing about personal development, entrepreneurship, personal finance and is a Certified Financial Education Instructor (CFEI).

Share this post:

AddTable of Contents