The 5 Most Common Private Student Loans Requirements

Summary:

Most private student loan lenders have five basic requirements that a borrower must meet. These include requirements based on the borrower’s desired school, age and citizenship status, credit history, potential cosigner, and use of loan funds. However, private student loans should only be considered after exhausting your federal student loan options.

With college expenses rising every year, many future students find the overwhelming costs daunting. To help with this expense, many first look towards federal funding. But even though federal loans offer more favorable rates than private lenders, most students need more than federal student loans offer.

Therefore, many students turn to private loans to cover the remaining costs. But who qualifies for private student loans?

Because private loans are not regulated in the same way federal loans are, requirements for private student loans differ among lenders. In this article, we’ll review the five most common private student loan requirements, how the search for private loans may affect your credit score, and how to apply for the right loan for you.

Get Competing Student Loan Refinancing Offers

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

Who is eligible for a private student loan?

Unlike federal student loans, private student loans are not guaranteed. This is because private student loan requirements differ from the requirements of federal student loans. In addition to the requirements, federal student loans provide funding based on a student’s financial need. Private loans, on the other hand, rely more on a borrower’s credit history.

Private student loans are lent by private parties, including include banks, credit unions, state-based or state-affiliated organizations, and online lenders. Since private loans are not regulated by the federal agencies monitoring federal loans, each private lender has different terms and conditions set in place.

Before receiving a private loan, you’ll need to meet a specific lender’s criteria for credit and income. If not, you’ll need to apply with a cosigner who can.

Pro Tip

Beyond comparing online lenders, contact your school’s financial aid office to find out what loans they offer. Some institutions have a list of lenders who work with them directly.

What are the requirements for most private student loans?

Many lenders require that student loan borrowers must qualify under five common loan terms to be approved for a private student loan. However, loan term eligibility differs among many lenders.

1.) Eligible school

Many lenders need you to be at least a half-time student enrolled at your school. Your school must also be on the lender’s list of eligible schools. While most four-year colleges qualify, you’ll have to look carefully at two-year community colleges and trade schools, as these institutions don’t always meet some lenders’ eligibility criteria.

That being said, multiple lenders offer private student loans specifically designed for students attending community college and trade schools.

Pro Tip

When determining if your school qualifies, speak to the private lender about your options. Additionally, reach out to your school’s financial aid office for more information.

2.) Age, education, and citizenship

In addition to being enrolled at a specific school, applications must also meet specific age, education, and citizenship requirements.

- Age and education. You’ll have to be 18 years or older with a high school diploma or equivalent, such as a GED or home school certificate.

- Citizenship. Typically, lenders require you to have a Social Security number. If not, you must be a U.S. citizen or a permanent resident.

- International students. With some lenders, you might be eligible to borrow a private student loan with a U.S. citizen or legal resident cosigner.

3.) Credit and income criteria

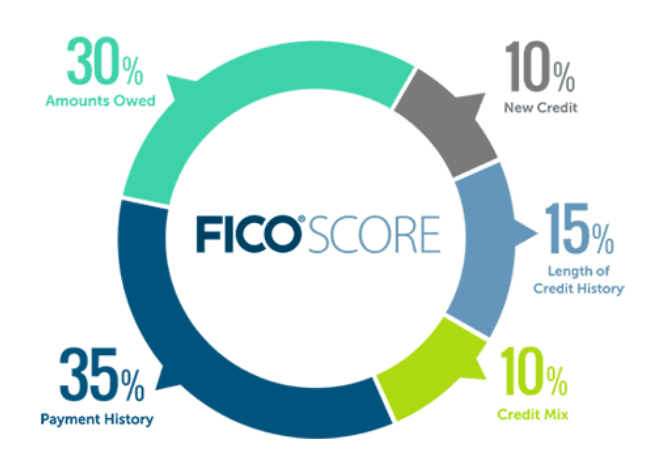

Unlike a federal student loan, where credit scores aren’t assessed in determining eligibility, private lenders look at your credit history, income, and your debt-to-income ratio.

A lender who offers private student loans may disqualify you if your credit score is below the mid-600s. Higher credit scores in the 700s and 800s will qualify you for the best rates and terms.

Many lenders ask for proof of a steady employment and a low debt-to-income ratio. If you don’t have a salary, which many college students don’t, then you’ll need a cosigner with an appropriate salary to agree to the loan terms.

4.) Creditworthy cosigner

Undergraduate students with only a high school diploma may not have much credit history or established income. A creditworthy cosigner can be an advantage when you submit a private student loan application.

A cosigner is often a parent or guardian who will share responsibility for your college debt, so you’ll want to be on the same terms about your loan repayment schedule. Some private lenders offer a cosigner release after a certain number of on-time monthly payments.

5.) Educational expenses

It’s in the name. Private student loans are meant to cover a student’s educational expenses.

Private lenders will communicate with your school’s financial aid office to verify your information about the student loan. This is done after submitting your private student loan application. Your school’s financial aid office will certify the amount you’re asking to borrow, the cost of tuition, and inform the private lender about any other financial aid that you’ve received.

The loan amount will be sent directly to your college, with any extra funds given back to you. The leftover loan amount can be used for textbooks or other education-related expenses. However, remember that any loan money you receive must be repaid-with interest.

How private student loans affect your credit

When you apply for a private loan, the lender will first run a credit check, which often results in a hard inquiry. Because a hard inquiry check indicates you are shopping for a loan, your credit score will show a slight and temporary dip.

Student loan debt will impact your credit reports and scores down the line. Be sure not to miss a monthly payment, as late loan payments will stay on your report for seven years. However, being on time for each monthly payment can help you build good credit.

Pro Tip

If the thought of getting a hard inquiry check worries you, try to get prequalified for a loan before applying. A lender will give an estimate of the loan terms you’re likely to qualify for, as well as the loan amount you’re able to borrow.

Does paying off a student loan help your credit score?

A student loan can help or hurt your credit score. This depends not only on whether you make consistent payments in full and on time but also on how long you hold the loan and what other debts you already have.

If you’re worried about making your loan payments on time, consider a consolidation loan or refinancing your student loans.

Is it better to get a private or federal student loan?

Even if you are eligible for private student loans, it’s usually a good idea to exhaust your federal student aid options first. In addition to offering forbearance and deferment options, federal student loans are generally more cost-effective than private loans. Between additional fees and higher interest rates, private loans are often the more expensive choice.

Here is a summary of the requirements of private and federal student loans.

| Requirements | Private student loans | Federal Direct Student Loans |

|---|---|---|

| FAFSA required to apply | no | yes |

| Requires applying directly with a lender | yes | no |

| Considers credit history | yes | no |

| Borrowing limit determined by FAFSA | no | yes |

| Sometimes allows borrowing up to cost of attendance (COA) less financial aid received | yes | no |

| Cosigners can help increase chances of approval | yes | no |

| Made to students based on financial need | no | (Direct Subsidized Loans only) |

| Allows change in repayment plan after borrowing without refinancing | no | yes |

Before choosing a private loan, explore the best interest rates among private lenders. A lower interest rate means lower payments, thus saving you more money in the long term.

Pro Tip

When considering your options among private lenders, look at repayment options as well as customer reviews. Not only will this provide you with comparisons for the best deal, but you’ll also see which lenders are the easiest to work with.

How do I apply for a private student loan?

You can apply for a private loan through most lenders’ websites. Before doing so, gather the personal information you’ll need. This includes information about:

- Your desired program or degree

- The school you’ll be attending

- Desired loan amount

- Standard personal and financial information

- Cosigner’s information (if applicable)

When applying, be sure to choose the appropriate private student loan as prices may differ depending on what level of education you are entering. You also must carefully review interest rates and repayment plans to find the plan that best suits your needs and repayment abilities.

Key Takeaways

- Private student loans may be offered through various financial institutions, including banks, credit unions, and nonbank lenders.

- Given the numerous sources for these loans, each lender may have different requirements in place.

- Before applying for a private student loan, exhaust your federal loan, scholarship, and grant options first.

- In addition to multiple forgiveness options, federal student loans are often more affordable than private loans.

- Unlike federal loans that grant aid based on financial need, private loan lenders provide funds based on the borrower’s credit score and history.

- Be sure to check that your school qualifies for the private loan you are considering. Your institution’s financial aid office may also have additional resources for you to review.

Share this post:

Table of Contents