What Is a Mortgage Statement?

Last updated 04/09/2024 by

Camilla Smoot

Summary:

A mortgage statement is a document that provides you with the latest details of your loan that is sent each billing cycle. Your mortgage statement will show you what you owe, what has been paid for, and how you can pay your monthly bill. It’s a good idea to hang onto these statements for documentation and tax purposes.

Mortgage statements are important documents that provide valuable information. It’s tempting to let statements and invoices pile up or just throw them out without a second thought. However, there is a lot to gain from understanding what’s in your mortgage statement. For example, you may need the data in your mortgage statements if you are audited by the IRS or to calculate your capital gains tax. Regularly checking your mortgage statements is also a great way to ensure your payments are accurate. Let’s take a deep dive into everything you should know about your mortgage statement.

What is a mortgage statement?

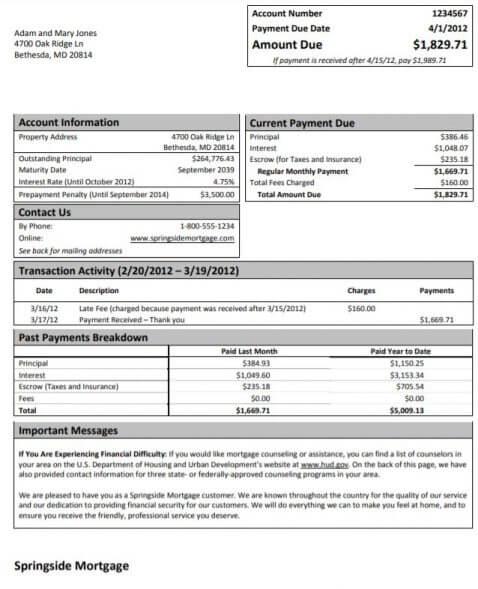

A mortgage statement is a document that lays out up-to-date information on the details of your loan. Mortgage statements will be issued to you each billing cycle, which is generally every 30 days. Mortgage statements are not always sent by your lenders. Lenders often use loan servicer to handle payment and issue mortgage statements.

A mortgage statement generally includes the principal, interest, insurance, and property taxes balance.

Interest is a charge for borrowing money and will be listed on your mortgage statements. The interest rate shows either how much money the lender or institution is receiving for lending out money, or how much ownership a stockholder has in the company. Interest rate is usually stated as an annual percentage rate (APR). After taking out a mortgage loan, you will probably have a mortgage interest added to your statement.

When purchasing a home, you will likely have the opportunity to purchase homeowners insurance. Homeowners insurance is usually built into your mortgage. If you chose to have your homeowner’s insurance included in your mortgage, you will now have an escrow account. An escrow account is a separate account managed by your loan servicer. They will use your escrow account to manage payments for your homeowner’s insurance and sometimes property taxes. Escrow payments are usually made monthly.

You might also see a schedule of payments that lists a payment, principal, interest, and balance. The principal balance shows the amount borrowed and what you need to pay back. The interest balance shows what the loan servicer is charging you for lending their money. The principal interest payment will be part of your monthly statement.

What is listed on a mortgage statement?

The exact information and formatting of a mortgage statement will vary depending on the lender or loan servicer. However, most will include the following:

- The current balance of the mortgage statement.

- Interest paid on the mortgage.

- Current interest rate.

- The amount remaining on the mortgage term.

- Total amount paid.

- Payment amount owed.

- Your payment history.

- Any late payments (also known as a delinquency notice).

- Account information. including your mortgage loan account number.

- Contact information, such as a phone number, for the lender.

- Property taxes.

- Principal balance.

How to use your mortgage statement

1. Review your mortgage statement

Be sure to go over your mortgage statement in a timely matter. Choose a moment when you have enough time to read over all the important details. Check for changes, new information, or inconsistencies in the document. Bring up any problems you see with your lender.

2. Make your mortgage payments

Although a mortgage statement provides you with a lot of important and relevant information, its main purpose is to remind you to make your payments on time. So, after reviewing and making sure everything is correct, be sure to make the total payment before the grace period is up to prevent late fees or a delinquency notice.

There are a few ways to pay your loan. Most lenders provide you with the following options.

Online mortgage payment

Paying online is generally fast and very convenient. You can usually pay your mortgage payments using your bank account, but your debit or credit card account are usually options, too. You will likely need your mortgage loan account number to pay online.

Payments by mail

Fulfilling your mortgage payment by mail is easily done. All that needs to be done is to attach a check to the payment stub of the statement and send it to the appropriate address.

Payment by phone

Mortgage payments by phone are usually done by an automated system, but you can often opt in to speak to a customer service representative.

In-person mortgage payment

If you chose make your mortgage payment in person, just travel to the local office or branch of your mortgage lender to do so.

Automatic withdrawal

Lenders give you the option to pay each monthly payment automatically every billing cycle. This is an easy way to ensure your mortgage payments are made in time.

3. Account for interest paid

The IRS requires lenders to send out a year-end statement to customers who have paid more than $600 in a calendar year. This is also called an annual mortgage statement, and you will need this document if you are planning to claim tax deductions on mortgage interests.

4. Save and store your monthly mortgage statement for documentation

Hang onto your mortgage statement for documentation. If you are planning on selling your home or refinancing your mortgage, it is important to be able to provide others with the latest mortgage statement as it helps determine the total value of your outstanding balance. These documents may also be needed for a tax return.

Thinking of refinancing your mortgage? Before you do so, be sure to compare rates to make sure you save the most money. Click here to start comparing.

Frequently Asked Questions

How often do you receive a mortgage statement?

You receive a mortgage statement from your loan servicer every billing cycle, which is generally once a month.

Can you get a mortgage without showing bank statements?

It’s very unlikely. Lenders usually require borrowers to have a checking account and provide evidence of sufficient cash flow to cover mortgage payments. Federal regulations actually require lenders to document evidence of the borrowers ability to pay.

How does a bank statement mortgage work?

A bank statement mortgage refers to when a lender uses bank statements to help verify income instead of tax returns. A lender will use these bank statements to prove the ability to repay a loan. These mortgages are useful for self-employed because their bank statements can provide a better understanding of their income than tax returns. .

What will my mortgage statements look like?

A monthly mortgage statement looks like any other general bill you receive from a financial organization. It shows charges paid, charges owed, overdue payments, account information, and more. In some cases, a loan servicer will send the statement on behalf of your lender. Mortgage statements also provide you with contact information if you have any questions. You can probably ask your lender to show you an example of what mortgage statements looks like so you know what to expect.

Key takeaways

- A mortgage statement is a document detailing the information of your loan.

- You will receive a mortgage statement every billing cycle.

- Mortgage statements usually include loan information such as your interest rate, amount paid, and balance remaining.

- You can pay your mortgage payments monthly payment by phone, mail, online, in-person, or through automatic withdrawal from your bank account.

- Hang onto your monthly mortgage statements and annual mortgage statement for tax reasons.

Camilla has a background in journalism and business communications. She specializes in writing complex information in understandable ways. She has written on a variety of topics including money, science, personal finance, politics, and more. Her work has been published in the HuffPost, KSL.com, Deseret News, and more.

Table of Contents