IRS Form 1099-C: How to Avoid Taxes on Forgiven or Canceled Debt

JW

Last updated 03/15/2024 by

Jessica WalrackDid you receive a 1099-C Cancellation of Debt Form from the IRS? If you have, you are probably a little confused. Not many people know that the IRS considers debt forgiveness compensation and as a source of income. You could call it a debt forgiveness tax. Yes, if you are lucky enough to get a creditor to forgive or cancel a debt, the IRS considers the “forgiven debt” compensation and taxable income.

When does this occur? A common example is a short sale of a home where the mortgage exceeds the fair market value, so the lender forgives the remaining balance. Even though you didn’t receive that money and the fair market value of your home left a balance, that change from the lender would be considered canceled/forgiven debt.

To understand the tax implications of this situation, you’ll need to get familiar with IRS form 1099-C and report the amount to the IRS.

Do you owe taxes if your debt was canceled? Just because you received a 1099-C form and had your debt forgiven doesn’t mean you have to claim that debt as income/compensation and pay forgiveness tax. The answer depends on the amount of debt canceled and on your circumstances. Read on to learn:

- What the 1099-C form is.

- When to file the 1099-C.

- The exclusions and exceptions might relieve you of your tax liability if you had your debt forgiven.

- What to do when you receive an IRS form 1099-C.

End Your IRS Tax Problems

Get a free consultation from a leading tax expert.

It's quick, easy and won’t cost you anything.

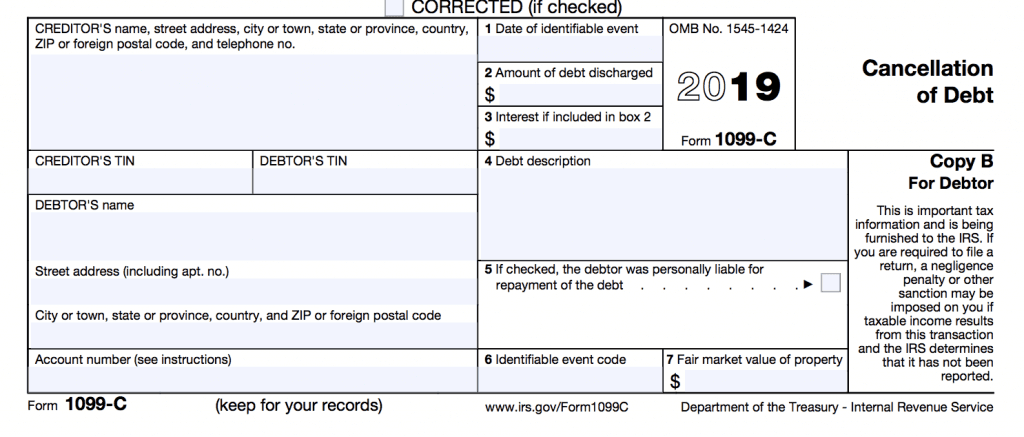

What is reported on tax form 1099-C cancellation of debt?

If your debt is forgiven or settled for less than the full amount of what you owe, the lender will report this to the IRS as lost income. According to the website, the IRS views this cancellation from the lender as earned income that should be taxed. If a lender forgives or settled a debt worth more than $600, the lender must send you and the IRS a Form 1099-C at the end of the year. This form is for reporting income when you file your taxes for the year your lender forgave your debt. The IRS will expect you to report that amount as income.

Even if you don’t receive a Form 1099-C from the lender, they likely sent one to the IRS. So whether you get one or not, you’re responsible for reporting the forgiven or settled amount in your tax return. Failure to comply could result in a tax bill or audit notice from the IRS. Incurring penalties and fees increase your tax owed and can push you deeper into debt. The IRS includes the debt in your income for the year on your taxes.

You’ll notice box 3 lists the debt as income. If the lender puts a checkmark in box 6, that’s another clue. A checkmark in box 6 means you’re liable and have to claim this as income on your tax return.

If this applies to you, you’ll get a 1099-C form in the mail. Each tax year, about 4 million 1099-C forms are filed and then reported as income on your tax return.

Have you received a form or letter from the IRS that you don’t completely understand? Check our comprehensive guide to IRS letters and notices.

When do you have to pay for debt forgiveness?

Do you have to pay taxes on a discharged debt?

If you received a tax form 1099-C, your discharged debt is considered taxable income unless you qualify for an exclusion or exception. Note that exceptions apply before the exclusions.

Exceptions

If your debt was discharged under the following circumstances, you won’t have to pay taxes on it.

- The debt was canceled as a gift, bequest, devise, or inheritance.

- Payment of the debt would have been a deductible expense.

- Forgiveness/cancellation of certain student loan debt. However, not all student loan forgiveness programs are tax-exempt — make sure to read the fine print of your arrangement.

- Reductions of a home’s mortgage debt principal balance due to Pay-for-Performance Success Payments under the Home Affordable Modification Program.

- If you receive only social security income and can prove insolvency

Exclusions

After applying all of these, you may still be able to exclude canceled debt in the following situations:

- The debt was canceled as part of a title 11 bankruptcy.

- Insolvency occurred immediately before the cancellation of the debt (in other words, your debt was worth more than your assets).

- Qualified farm indebtedness, real property business indebtedness, or principal residence debt

If you end up excluding canceled debt from your income, you must include Form 982 to reduce certain tax attributes by the amount you’ll exclude. This is where a professional tax preparer benefits you. A tax professional can come in handy here.

Want to know more? Read IRS Publication 4681 on the IRS website.

How much debt has been canceled?

According to the IRS’s latest data, $89.6 billion in canceled debt has been claimed on federal tax returns since 2007 (source).

Who must file form 1099-C?

Generally, any “applicable financial entity” that processes a cancellation of $600 or more debt must file a form 1099-C when an “identifiable event” occurs.

What is an applicable financial entity?

‘Applicable financial entities’ include any institution that extends loans or lines of credit.

What is an identifiable event?

According to the federal tax professionals, the IRS, “identifiable events” include:

- Title 11 bankruptcy

- Other judicial debt relief.

- Relief from probate or a similar proceeding.

- Cancellation by agreement.

- Another type of discharge before an identifiable event.

To illustrate, here are some examples of situations that require the filing of a Form 1099-C:

- A debtor can’t repay a personal loan of $5,000 and agrees to pay a $2,000 lump sum to settle. The account is closed and discharged.

- A borrower can’t afford their car payments. Their vehicle is repossessed and sold at an auction for 65% of the remaining balance. The creditor discharges the difference between what is owed and what is recovered.

In these cases, the applicable financial institution must file the 1099-C for the amount of canceled debt.

What happens if you don’t file a 1099-C?

If a creditor accidentally fails to file Form 1099-C, they’ll face a penalty.

If a debtor receives a form 1099-C and fails to report the qualifying amount as income on their taxes, they’ll likely receive notices from the IRS about an income discrepancy regarding canceled debt. This can lead to IRS interest charges, penalties, and even an audit.

How does a form 1099-C affect your credit?

Form 1099-C has no direct impact on your credit report because credit bureaus don’t see it. Only the IRS and the debtor in question receive the form.

However, the creditor who files the 1099-C will usually report your default and discharged canceled debt directly to the credit bureaus. This negative mark can remain on your credit report for up to seven years.

Debt settlements and your credit

The average American has $38,000 in debt. Whether you’re overwhelmed with credit card debt or medical bills, there are debt relief firms that negotiate a debt cancellation settlement with lenders so that you can pay less than the original amount.

However, this practice can impact your credit because you’re not making consistent—if any—payments to lenders while the firm is gathering information and negotiating a settlement. According to the Federal Trade Commission (FTC), lenders can still charge you late penalties and fees during this process.

What to do if you receive a form 1099-C

If you receive a 1099-C form, here’s what to do.

First, make sure that all of the information is correct. Did you have a forgiven debt in the amount stated?

If so, it’s time to look for exclusions or exceptions. Figuring out if you qualify can get complicated, so enlist the aid of a competent tax professional and products. This can ensure that you don’t pay more than you have to.

A professional has the products and information to find out how much you can reduce your taxable income, which can affect your tax return and your tax refund, or if you can avoid having to pay taxes altogether.

Is there anything I don’t have to declare as taxable income?

The IRS may consider this as income, but it’s not all taxable income. According to the IRS website, the following circumstances may exempt you from reporting income when you file your taxes (source).

- Amounts canceled as gifts, bequests, or inheritance.

- Certain qualified student loans if canceled as part of work forgiveness programs.

- Certain other education loan repayment or loan forgiveness programs

- A qualified purchase price reduction given by the seller of property to the buyer.

- Any Pay-for-Performance Success Payments that reduce the principal balance of your home mortgage under the Home Affordable Modification Program.

- Amounts from student loans discharged on account of death or total and permanent disability of the student.

If you meet these requirements, you don’t have to include them in your income.

Exclusions from gross income

Even if your canceled debt does not qualify for an IRS exception, you may still be able to reduce or remove your liability by claiming one of these exclusions. This may seem like one of those offers that appear too good to be true, but we bring the truth.

- Canceled in a Title 11 bankruptcy case.

- Canceled during insolvency.

- Qualified farm indebtedness.

- Cancellation of qualified real property business indebtedness.

- Qualified principal residence indebtedness that is discharged subject to an arrangement that is entered into and evidenced in writing before January 1, 2018.

If one or more of these apply to you, you’re required to reduce certain tax attributes by completing Form 982. Complete it and attach it to your tax return. For further assistance, consult a qualified tax professional.

Need help hunting for exclusions?

Once taxes begin to get complicated, it can be helpful to have an expert on your side. Tax firms have experience with 1099-C forms and other issues that may arise in this situation. They can ensure that you file everything properly regarding debt income. And if an issue comes up down the road, they can also represent you in dealings with the IRS. Not sure where to start? Review and compare leading tax firms here.

Related article: How to respond to IRS CP3219N

What if you already paid taxes on what you could have excluded in your tax return?

If you are just now realizing you could have claimed exclusions, there is still hope. You can amend previous tax returns and claim a refund for up to three years.

This is what you need to do. Although at this stage it is a good idea to hire a tax professional.

- First, collect all the documents you used to file the tax return you want to amend. You don’t want to trigger an audit by creating a discrepancy in your reported income.

- Second, download all the tax forms you need. These include IRS Form 1040X, Form 982 and Publication 4681, Canceled Debts, Foreclosures, Repossessions, and Abandonments. These are available on the IRS website.

- Complete the forms and amend your tax return with Form 1040X. Amended returns can’t be e-filed, so you will need to go old-school. Print and mail the documents and mail the paperwork to the address assigned to your state.

If you live in | Mail Form 1040X and attachments to: |

|---|---|

| Florida, Louisiana, Mississippi, Texas | Department of the Treasury Internal Revenue Service Austin, TX 73301-0052 |

| Alaska, Arizona, Arkansas, California, Colorado, Hawaii, Idaho, Illinois, Indiana, Iowa, Kansas, Michigan, Minnesota, Montana, Nebraska, Nevada, New Mexico, North Dakota, Ohio, Oklahoma, Oregon, South Dakota, Utah, Washington, Wisconsin, Wyoming | Department of the Treasury Internal Revenue Service Fresno, CA 93888-0422 |

| Alabama, Connecticut, Delaware, District of Columbia, Georgia, Kentucky, Maine, Maryland, Massachusetts, Missouri, New Hampshire, New Jersey, New York, North Carolina, Pennsylvania, Rhode Island, South Carolina, Tennessee, Vermont, Virginia, West Virginia | Department of the Treasury Internal Revenue Service Kansas City, MO 64999-0052 |

| A foreign country, U.S. possession or territory*; or use an APO or FPO address, or file Form 2555, 2555-EZ, or 4563; or are a dual-status alien | Department of the Treasury Internal Revenue Service Austin, TX 73301-0215 |

JW

Jessica Walrack is a personal finance writer at SuperMoney, The Simple Dollar, Interest.com, Commonbond, Bankrate, NextAdvisor, Guardian, Personalloans.org and many others. She specializes in taking personal finance topics like loans, credit cards, and budgeting, and making them accessible and fun.

Share this post: