Can you have both a Roth IRA and Traditional IRA?

Last updated 04/08/2026 by

Andrew Latham

Yes, it is possible to have both a Roth IRA and a traditional IRA. If you qualify, you should have one of each. Why? Two words: tax diversification.

If you do choose to open two IRA accounts, you will have to consider the IRS’s maximum annual contribution, which applies to both Roth IRAs and traditional IRAs. In 2014, the maximum contribution was $5,500 ($6,500 if you’re 50 or older) or your taxable compensation for that year, whichever was less. Notice that you need to have a job to qualify. If you – or your spouse, if filing jointly – don’t have any taxable income during a given tax year, you cannot contribute toward either a Roth or a traditional IRA.

To illustrate, if your taxable income is higher than $5,500 and you’re under 50, you could contribute to both a Roth IRA and a traditional IRA up to a combined maximum of $5,500 a year. You could contribute $2,250 in each, $4,000 in one and $1,500 in the other, or any combination you prefer, as long as the combined contribution does not exceed the annual maximum.

Another limitation to consider is that if you’re a higher-income worker (above $100,000 a year) or married filing separately. If you fall under either bracket, you may face restrictions on how much you can contribute toward a Roth IRA. More details on Roth IRA limitations at the end of the article.

That’s the skinny on whether you can or can’t have both a Roth IRA and a traditional IRA. Let’s flesh out that answer by dealing with some other questions you probably have in mind. Such as, what is the difference between a Roth IRA and a traditional IRA? And which one offers the best deal?

Get Competing Personal Loan Offers In Minutes

Compare rates from multiple vetted lenders. Discover your lowest eligible rate.

It's quick, free and won’t hurt your credit score

What’s the Difference between Roth IRA and Traditional IRA?

The main difference between Roth IRAs and Traditional IRAs is how they are taxed.

Roth contributions are after-tax, so you’ll never have to pay taxes on withdrawals of your contributions or the interest they generate. This is true so as long as you wait until you’ve reached age 59 ½ to cash in. The catch is you cannot deduct your contributions from your taxable income, so you don’t receive immediate tax savings.

Traditional IRAs are the exact opposite. Contributions to a traditional IRA can be pre-tax, which means they can reduce your taxable income. However, you will have to pay income tax on withdrawals of all your earnings and any contributions you deducted on your taxes. They give you a break at the front end and then hit you with a tax bill when you retire.

Valuable Tax Savings

Both types of IRA offer valuable tax savings. Which one is best for you will depend on your current tax rate and what you think your tax rate will be when you retire.

If you think your tax rate will be much lower when you retire, then a traditional IRA may offer the most savings. On the other hand, if you think your tax rate will be higher when you retire or that the growth of welfare spending is unsustainable and that income tax rates will be higher for everyone when you retire, you may prefer paying your taxes upfront and invest in a Roth IRA.

It’s impossible to know for sure what your tax rate will be at retirement, so choosing between a Roth and Traditional IRA is a bit of a gamble, which is why it’s a good idea to have money in both.

Roth IRA Advantages

If you’re young, a Roth IRA may offer the best deal because there’s a good chance the tax you pay on the interest generated by your contributions over several decades will outweigh the savings provided by pre-tax contributions.

One reason to prefer Roth IRAs is that your Roth contributions can be worth more in retirement. Roth contributions are already taxed, which allows you to contribute more on a tax-advantaged basis. Remember the $5,500 annual contribution limit. Over time, the extra savings add up.

Another benefit Roth IRAs offer is that withdrawals from Roth IRA don’t count as income. This benefit is important when you retire. Whether your Social Security benefits are taxed or not will depend on taxable income and your traditional IRA withdrawals. However, the same does not your Roth IRA withdrawals. If you have enough money in your Roth IRA, you may be able to stay in the lowest tax bracket but still have enough money to meet your retirement needs, and even some of your retirement “wants.”

Roth Limitations

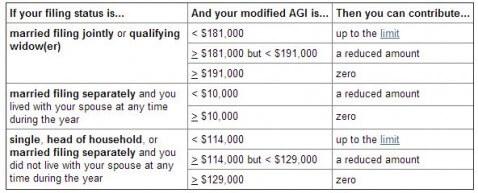

Anyone who has taxable compensation from a job can contribute toward a traditional IRA. However, the same doesn’t apply to Roth IRAs. High-income workers are limited, and even excluded, from contributing.

Taxpayers with a modified adjusted gross income above $114,000 if single, or $181,000 if married filing jointly. Married taxpayers filing separately who have lived together at any time during the tax year only qualify for a limited reduced contribution and are excluded altogether if their MAGI is above $10,000. The limits vary depending on your filing status.

In case you’re wondering, your modified adjusted gross income is your taxable income with certain nontaxable sources of income and deductions, such as foreign earned income, added back. Find a modified adjusted gross income calculator published by the IRS.

Do Roth IRA and Traditional IRA, If You Can

If you qualify, open both a Traditional IRA and a Roth IRA. This will add tax diversification to your portfolio and allow you to reap the benefits of both pre-tax and after-tax retirement accounts. However, you may want to invest more in your Roth IRA, particularly if you’re young.

FAQ on Roth IRA and Traditional IRA

What is the difference between Roth IRA and traditional IRA?

Both Roth and traditional IRAs are retirement savings and investment vehicles. Roth IRA contributions are made with post-tax dollars, while traditional IRA contributions are made with pre-tax dollars.

Can you contribute to a traditional IRA and a Roth IRA at the same time?

Yes, an individual can contribute to both a Roth IRA and a Traditional IRA in the same year. The total contribution into both cannot exceed $5,500 for individuals under 50, and $6,500 for those 50 and over.

What happens if I put more than a limit in my IRA?

If you contribute more than the IRA or Roth IRA contribution limit, the tax laws impose a 6% excise tax per year on the excess amount as long as it remains in the account.

Is there an income limit for traditional IRA?

There are no income limits for Traditional IRAs, however there are income limits for tax deductible contributions.

Can I withdraw money from my IRA?

Under certain conditions, you can withdraw money from your IRA without penalty. The rules vary depending on the type of IRA you have. Generally, for a Traditional IRA, distributions prior to age 59½ are subject to a 10% penalty in addition to federal and state taxes unless an exception applies.

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

Share this post:

Table of Contents