Andrew Latham

Andrew is the Content Director for SuperMoney, a Certified Financial Planner®, and a Certified Personal Finance Counselor. He loves to geek out on financial data and translate it into actionable insights everyone can understand. His work is often cited by major publications and institutions, such as Forbes, U.S. News, Fox Business, SFGate, Realtor, Deloitte, and Business Insider.

articles from Andrew

287 posts

The Value of Financial Calculators

Published 06/10/2026 by Andrew Latham

Most people lose money not because they’re reckless, but because the human brain is genuinely bad at doing interest math in its head. We underestimate how fast debt grows and how much savings compound, and the research on this is brutal. Financial calculators fix the problem by swapping out your gut for the actual numbers. Run the math before you sign anything and you’ll catch the six-figure mistakes your intuition would have waved right through.

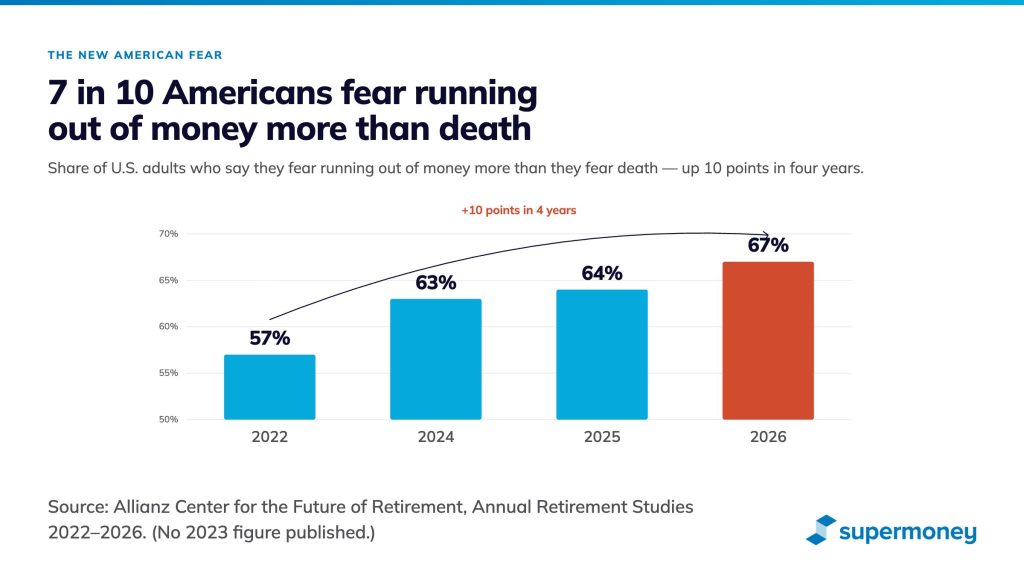

Americans Fear Running Out of Money More Than Death. The Real Problem Isn’t What You Think.

Published 05/06/2026 by Andrew Latham

A new Allianz survey finds that 67% of Americans now fear running out of money more than they fear death. The number keeps climbing every year. But here is the part that almost no one is reporting: half of Americans flat-out guessed at their retirement number, and only 23% have a written financial plan. The fear has two pieces. The math piece is real. The clarity piece is fixable in about three hours of work this week.

The $100K Question: Is College Still the Best Gift You Can Give Your Kid?

Published 03/17/2026 by Andrew Latham

There’s no single right answer to whether you should help your kid pay for college, buy property, or start a business. The right move depends on the kid, the degree, and how the money is structured. A nursing degree and a philosophy degree are not the same investment. Neither is buying your child a house to live in versus helping them acquire a rental duplex. And for parents who can’t write big checks, small moves like opening a custodial Roth IRA or a 529 plan can quietly build serious wealth over time.

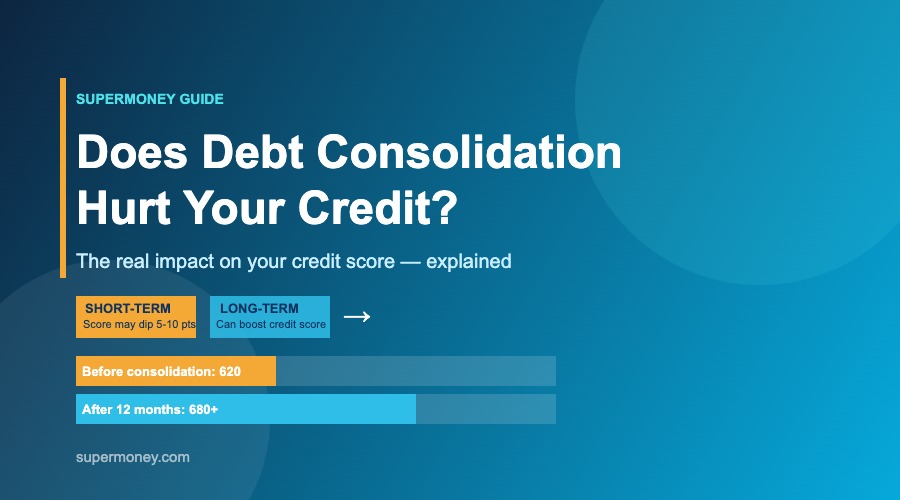

Does Debt Consolidation Hurt Your Credit?

Published 02/20/2026 by Andrew Latham

You’ve got a pile of credit card debt and you’re thinking about rolling it all into one loan to simplify your life. Smart thinking. But then you hear someone say “debt consolidation ruins your credit” and now you’re second-guessing everything.

Debt Snowball Calculator: Build Your Payoff Plan

Published 02/20/2026 by Andrew Latham

The debt snowball method is a debt payoff strategy where you pay off your smallest balances first, then roll those payments into your next-smallest debt. It’s not the mathematically cheapest method (that’s the avalanche), but it’s the one most people actually stick with — because early wins build real momentum. This guide explains how the snowball works, walks you through building your payoff plan step by step, and helps you decide if it’s the right strategy for your situation.

Debt Relief Attorney vs. Debt Settlement Company: Which Is Right for You?

Published 02/20/2026 by Andrew Latham

When you’re drowning in debt, the choice between a debt relief attorney and a debt settlement company isn’t just about cost — it’s about what kind of protection you need. Attorneys are licensed professionals who can represent you in court; settlement companies can negotiate but can’t defend you legally. This guide breaks down the key differences, costs, risks, and when to use each — so you can make the right call for your situation.

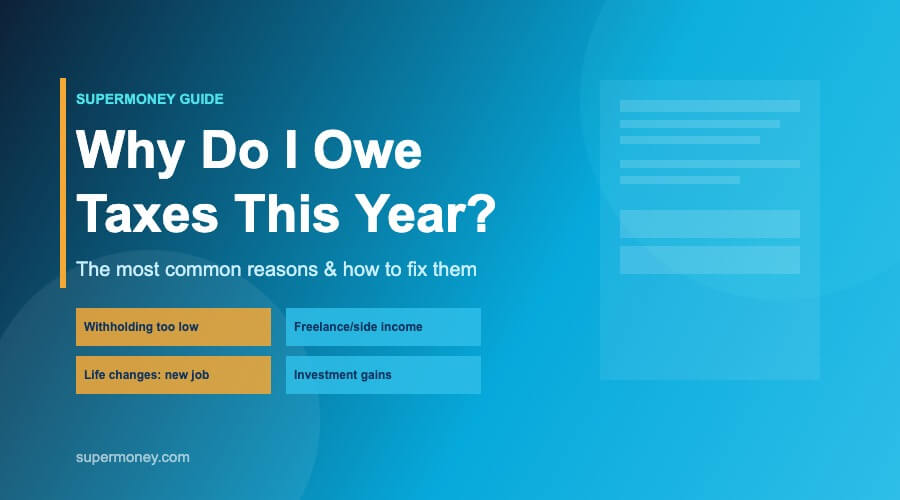

Why Do I Owe Taxes This Year?

Published 02/20/2026 by Andrew Latham

If you’re used to getting a tax refund and suddenly owe the IRS money, you’re not alone — and it doesn’t necessarily mean you did anything wrong. Owing taxes usually comes down to a gap between what was withheld from your paychecks (or paid in estimated taxes) and what you actually owe based on your total income and deductions. This guide walks through the most common reasons people owe taxes unexpectedly, how to fix the problem going forward, and what to do if you can’t pay what you owe right now.

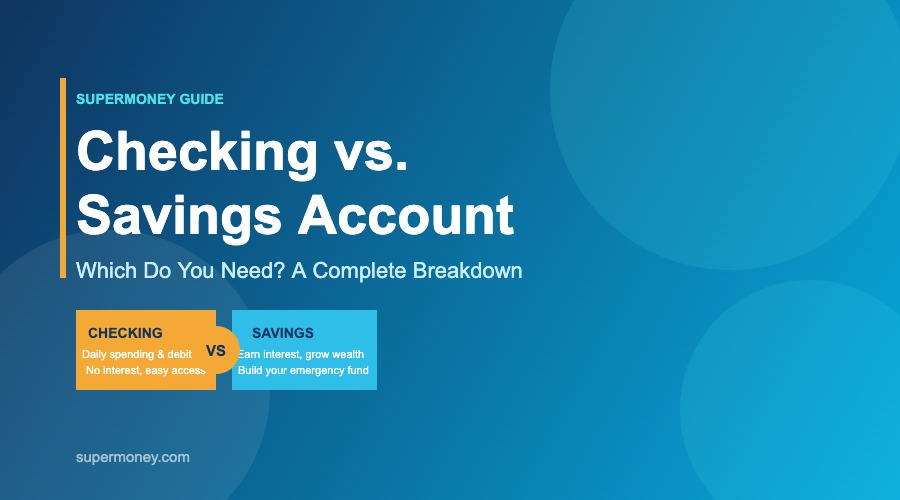

Checking vs. Savings Account: Which Do You Need?

Published 02/20/2026 by Andrew Latham

Checking accounts are your financial hub for daily life — unlimited transactions, debit cards, bill pay, but little to no interest. Savings accounts are where you park money you’re not touching, earning interest (often 4–5% APY at online banks) while staying separate from your spending. For most people, using both — linked but separate — is the smartest setup. Here’s exactly how each one works and which you need.

How to Deal With Financial Stress and Anxiety: Practical Ways to Feel More in Control

Published 02/02/2026 by Andrew Latham

Money worries don’t always show up as spreadsheets and bills. Sometimes they show up as sleepless nights, irritability, avoidance, or a constant low-level sense of panic.

What Happens When a Land Lease Ends? Renewal, Extension, and Exit Options Explained

Published 01/27/2026 by Andrew Latham

When a land lease ends, homeowners usually face one of several outcomes: renewal, renegotiation, sale, or relocation. The exact result depends on lease terms, state laws, and community policies. When you know what to expect at the end of a lease, it’s much easier to plan ahead and avoid any surprises down the road.